KOF Tourism Forecast: solid visitor numbers in winter

KOF is forecasting an increase of 270,000 overnight stays for the coming winter. This growth will be driven by both domestic and overseas guests. KOF expects to see a slight decline in overnight stays in the summer of 2024.

Following a summer season that exceeded expectations, the Swiss tourism industry is entering the winter months with a cautious but positive outlook. KOF’s winter forecast is based on a summer with 1.28 million overnight stays and a significant increase of 6 per cent on the back of a recovery in overseas guests, positive growth stimulus from China and the United States, and continued strong domestic demand. This upturn has resulted in growth of 10.6 per cent for the 2023 tourism year, which corresponds to 3.94 million additional overnight stays and thus exceeds the pre-pandemic level.

As we move into the winter months, this positive momentum is expected to continue, albeit at a slower pace. KOF is forecasting an increase of 270,000 overnight stays for the winter of 2023/24, bolstered by the solid figures from last winter. This expected growth stems from the hope that March 2024 will not be as snow-poor as last year (the least snowy since 1990, as documented by the WSL Institute for Snow and Avalanche Research SLF).

Review of the 2023 summer season and macroeconomic impact on tourism

A comparison shows that the Swiss tourism sector has performed remarkably well post-pandemic since the summer of 2023, especially when compared with other European countries (see chart entitled ‘Development of overnight stays’). Despite facing macroeconomic headwinds, Switzerland has had a good summer over this period.

The decisive factor here was that the success of Swiss tourism is determined by the domestic market. Despite experiencing a slight slowdown this summer, the volume of Swiss visitors remained impressively high and fell less sharply than expected. The figures for domestic visitors point to a long-term positive trend during the early and late summer months, when Swiss visitors increasingly opted for domestic trips to regions such as Ticino.

This resilience of Switzerland’s tourism figures contrasts with a global economic slowdown characterised by the economic downturn in China and the tightening of monetary policy, which is impacting on international travel. The macroeconomic challenges facing China – in particular its property crisis and the dwindling level of confidence in the government owing to the country’s strict and suddenly lifted COVID restrictions – are having an impact on Chinese consumers’ willingness to spend on foreign travel. Given the tougher visa requirements for Chinese tourists, KOF has therefore revised the growth rates in our most recent forecast downwards. However, growth stimulus remains very positive owing to the low level of these rates.

Trends and risks:

- Boost from Southeast Asia: This year’s summer was characterised by a surge in visitors from Southeast Asia. Guests from countries such as Indonesia and the Philippines increasingly opted for Switzerland, causing overnight stays to rise by almost 50 per cent compared with the pre-pandemic period. Overnight stays by visitors from India remain well below their pre-crisis levels.

- Caution in East Asia: In contrast to the strong figures seen in Southeast Asia, traditionally strong markets such as Japan and China remained cautious. It is still uncertain when and how tourism from these regions will recover.

- Low numbers of visitors from Russia: The sanctions imposed have caused a continuing decline in Russian tourism in Switzerland. This tourism during the summer months was around 30 per cent of its level in 2019. These sanctions are now having a particularly serious impact on the total number of overnight stays – especially during the winter months and, above all, in January, which were highly popular with Russian guests in the past. Given the current situation and the low probability of sanctions being lifted, this trend is expected to continue throughout the coming winter.

- Sustained US enthusiasm: North American visitors have boosted Swiss tourism this summer, achieving strong growth of 22 per cent in overnight stays compared with last summer.

- Upturn in French guests: Overnight stays by French visitors over the last two years have stabilised at a higher level than those from the rest of Europe. KOF reckons that this higher level will consolidate to some extent. Despite all the macroeconomic uncertainty, the 2022 and 2023 summer seasons comfortably exceeded their pre-crisis levels (up by 8 per cent in 2022 and 13 per cent in 2023). This trend contrasts with the numbers of overnight stays by guests from Germany and Italy.

- Numbers of Britons peak during the summer months: Overnight stays by UK visitors in August were at their highest since 2010. In contrast to other European countries, the British did not recover until summer 2023. This could be due to the prolonged economic slowdown caused by Brexit. It is uncertain whether this trend will continue next year or whether it was a catch-up effect. KOF expects to see these visitor numbers stagnate.

- KOF surveys and sentiment in demand for accommodation: A moderate upward trend in demand for accommodation is evident compared with last year. This suggests that the outlook for the tourism industry is generally positive, albeit with regional differences. The picture was similarly positive last year.

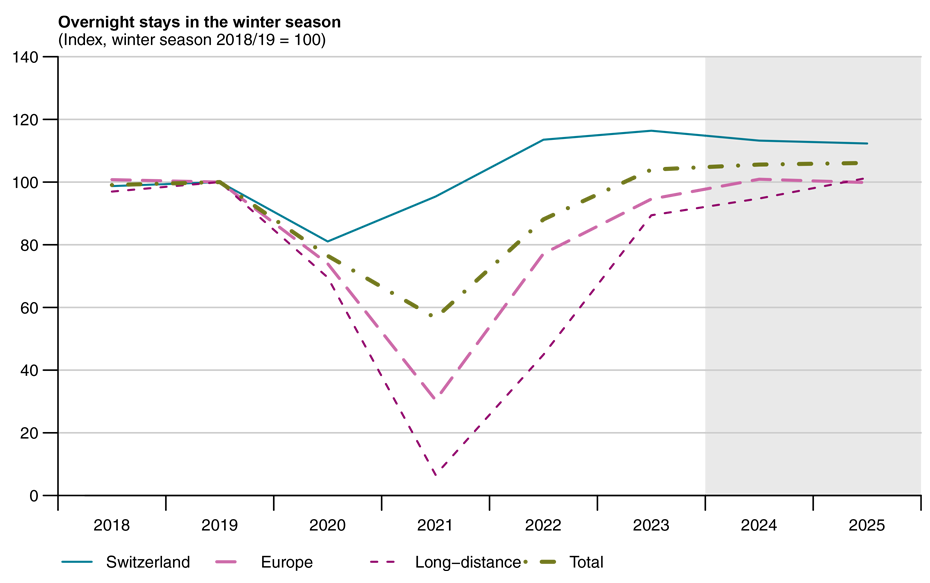

Winter forecast

KOF is forecasting an increase in overnight stays to 270,000 for winter 2023/24, which corresponds to an increase of 1.6 per cent compared with the previous season. The rise expected this season is due to one-off effects. Firstly, the unusually warm temperatures seen in March 2023 had a highly negative impact on last year’s winter business (almost 170,000 fewer overnight stays than in March 2019).

Secondly, European guests – particularly those from Germany – were reluctant to travel last year owing to the feared shortage of energy supplies, which led to heating restrictions in public buildings and dampened consumer sentiment. This situation creates a lower basis for comparison, so the return to normality is perceived as growth.

The situation is similar with Chinese visitors, who will remain below their usual level for some time but will provide seasonal and year-on-year growth stimulus. If Chinese guests remain roughly at the level last seen in the summer months of 2023, this will constitute growth of 133 per cent compared with the previous season, which corresponds to an increase of 120,000 overnight stays. These effects will generate year-on-year growth.

Switzerland: A slight decline is forecast for domestic tourism following a particularly strong previous season. However, overnight stays by Swiss guests are still forecast to be buoyant at 112 per cent of the level of the 2018/2019 winter season.

Europe: Switzerland is expected to see an 8 per cent increase in overnight stays by European guests, suggesting robust demand and a return to pre-pandemic levels (101 per cent of winter 2018/2019). Last winter was characterised by supply shortages, particularly in Germany. Even if the economic environment continues to stagnate, demand for travel is likely to be less affected than it was last winter.

Long-haul travel: The Asian markets are on the road to recovery with the focus on China, where an increase in overnight stays is expected, albeit starting from a very low level. Visitors from the US were already achieving enormous growth rates in the summer. This is likely to continue during the winter, albeit at a slightly lower level.

KOF expects the situation to stagnate during the following winter of 2024/25. European trends, such as the positive impact of tourists from France, will be dampened by the long-term flatlining of visitor numbers from Germany. Visitors from Switzerland are also likely to start travelling abroad again.

Summer forecast

The outlook for Swiss tourism in the summer of 2024 is mixed. KOF is forecasting a flatlining trend, with a decline of around 0.7 per cent (approx. 160,000 fewer overnight stays). The long-term stagnation in European visitors and the decrease in Swiss guests, who are unable to maintain their high numbers, are driving the outcome towards a slight decline. The growth forecast is cautiously optimistic if visa problems are swiftly resolved and macroeconomic factors do not prevent wealthier sections of the Chinese population from travelling. Chinese tourists could then return to almost pre-pandemic levels and help generate positive growth in the summer of 2024.

Switzerland: Following an exceptionally strong prior year, domestic tourism is showing signs of a slight slowdown. This demonstrates that the numbers of Swiss visitors travelling abroad have not yet returned to their pre-pandemic levels (see chart entitled ‘Swiss Tourism Abroad – Number of Arrivals at Tourist Destination’). Although expected to decline by 4 per cent, the number of overnight stays by Swiss guests in 2024 remains very high at 111 per cent of the level in the 2019 summer season.

Europe: Overnight stays in Europe are forecast to fall slightly by 4 per cent year on year in 2024. These figures will remain stable at 100 per cent of the 2019 level, which indicates Switzerland’s continued appeal. Positive trends (France, United Kingdom and Netherlands) are offsetting a gradual flatlining (Germany and Italy). The decline is partly more significant as KOF does not expect overnight stays by the French to maintain the high levels seen in summer 2023.

Long-haul travel: The positive trend is continuing in long-haul travel – particularly from Asia – where there is a 36 per cent year-on-year increase in overnight stays, representing a full recovery to 105 per cent of the 2019 level. Significant growth of 50 per cent is expected for China, with overnight stays reaching 84 per cent of the comparable year 2019.

The tourism figures for many regions are likely to have returned to normal by the summer of 2025. The number of Swiss visitors will also have flatlined by then. Visits from America will remain at a high level, while the number of European guests will stagnate. Growth potential will probably come from Asia. However, it remains unclear to what level guest numbers will return.

Contact

KOF FB Konjunktur

Leonhardstrasse 21

8092

Zürich

Switzerland