Swiss tourism shown to be crisis-proof

The tourism industry in Switzerland has managed to overcome the pandemic-related disruption and will continue to grow during the 2023 tourism year, according to KOF’s forecast. The domestic tourism sector is proving robust in the face of the slowdown in the global economy.

KOF expects to see an increase of 1.2 million overnight stays (up 5 per cent) during Switzerland’s 2023 summer season. This recovery is primarily due to the returning influx of foreign tourists, especially from China, and robust domestic demand. This will result in strong growth of 3.9 million overnight stays (up 10.5 per cent) in the 2023 tourism year, following the years of restrictions imposed by the pandemic. Overnight stays for both the tourism year and the summer season will exceed pre-pandemic levels for the first time and set new records, even if they fall short of pre-pandemic growth forecasts. This positive trend indicates that the tourism industry is managing to shake off the pandemic-related disruption. Despite all of this, it is important to note that the pre-pandemic growth path has still not been reached.

Trends: Looking ahead to the 2023 summer season, Swiss tourism is experiencing a mix of positive waves and challenging undercurrents. Here is an overview of the key trends shaping the landscape:

Positive trends:

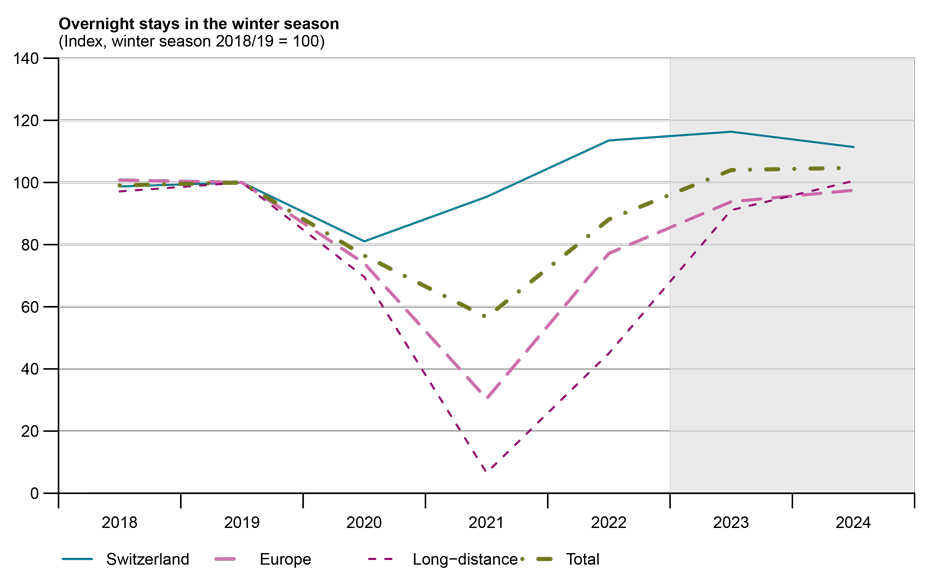

• Home advantage: Domestic tourism continues to boom. 9.2 million domestic overnight stays were recorded this winter, an increase of 200,000 overnight stays compared with the record winter of the previous year. This trend indicates that ‘staycations’ remain popular.

• The Chinese comeback: Chinese tourists are gradually returning to Switzerland. This is a positive trend that points to an expected normalisation over the course of the year.

• Stable outlook: According to KOF surveys, the tourism sector is set to perform steadily in the coming months. Even if Swiss tourists do not maintain their high share, they are expected to remain a significant force in the industry. The prospect of an increase in foreign travellers is also a good sign for the sector.

• Southeast Asia on the rise: The Southeast Asian countries – Malaysia, Thailand, the Philippines and Singapore – have posted record figures in recent months and are growing in importance. Their share of overnight stays in March was 2 per cent, which corresponds to the number of Italian guests. Overnight stays by guests from the Philippines doubled (210 per cent) in the same month compared with the pre-pandemic period. Similarly, Malaysia (208 per cent), Thailand (122 per cent) and Singapore (147 per cent) achieved a strong recovery and growth in the long-haul markets.

Future challenges: Swiss tourism faces a number of challenges between now and summer 2023 that need to be addressed:

• Freak weather: The events in March show that the success of the winter season depends heavily on the whims of the weather. This month had the least snow since 1990, as documented by the WSL Institute for Snow and Avalanche Research (SLF). This unexpected change in the weather mainly affected the numbers of guests from countries in which spontaneous bookings are normally possible, including Switzerland, Germany, France and Italy. Overnight stays therefore fell short of forecasts by almost ten percentage points, which illustrates the weather’s great influence on winter tourism.

• Inflation concerns: Strong inflationary pressures are casting a particularly long shadow abroad and could dampen demand for holidays. This possible change in consumer behaviour should be carefully considered in future forecasts.

• Economic conditions: Despite the less-than-ideal macroeconomic conditions prevailing in Europe, there has been a slight improvement here. The mild winter has helped to avert energy shortages and even higher inflation, providing some relief in these difficult times.

Comparative winter performance: The Swiss showed consistency. Winter tourism in Switzerland remained stable on a global comparison and reached a new record level, while neighbouring countries experienced a rollercoaster ride owing to various factors:

• Record winter in Switzerland: Switzerland experienced a record winter characterised by strong domestic demand (16 per cent above pre-pandemic levels). This growth was accelerated by the arrival of guests from overseas markets: North American guests increased by a massive 87 per cent, while Asia (excluding China) reported a 97 per cent rise.

• Holidaying at home: The number of overnight stays by Swiss guests has been 12 to 28 per cent higher each month in the past year than it was before the pandemic. In contrast, countries such as Italy, Austria and Germany are seeing significantly fewer domestic guest nights than they did before the pandemic, while the figures for France are stagnating.

• The energy crisis is reverberating across central Europe: Germany, Austria and Italy – the countries most affected by the energy crisis – had to cope with a challenging winter season and heavier losses. Switzerland achieved better results in winter owing to its less price-sensitive guest structure.

• France is thriving: France – like Switzerland – has seen a steady increase in tourist numbers. It is the only country where both local and foreign visitors are above pre-pandemic levels.

Summer 2023: a resilient Swiss tourism sector

KOF is forecasting an increase of 1.2 million overnight stays (up 5 per cent). This summer is expected to be the first to surpass the pre-pandemic number of overnight stays and hit a new all-time high. Despite all of this, it is important to note that the pre-pandemic growth path has still not been reached.

• KOF surveys: From the major towns and cities to the mountain and lake regions, sentiment in the accommodation industry remains positive. However, a slight gloominess was evident in the first quarter of 2023.

• Guest-related forecasts – a tale of two trends: KOF’s surveys show a divergence in the predicted numbers of domestic and foreign guests. While no further increase in domestic guests is expected for the summer, the number of foreign guests is likely to rise.

• The American wave continues: The trend towards more visitors from the United States is expected to maintain its strong momentum. Numbers in March were already 64 per cent up on last year and 20 per cent up on the pre-pandemic period.

• Chinese tourists – a recovery is in sight: Chinese tourists will significantly increase the numbers of overseas visitors. However, a full return to normality for Chinese tourists is not expected until the end of 2023.

• European visitors subdued: Overnight stays by European visitors are expected to flatline. While the outlook for the external economy remains relatively subdued, there is a slight upward revision for this summer owing to the mild winter across Europe that mitigated severe energy shortages.

Winter 2023/2024: modest growth at a high level

KOF expects to see modest growth at a high level of about 1 per cent (0.1 million) for the coming winter season.

• Swiss guests will ensure a good winter: Overnight stays by Swiss guests will be encouraging, with the relevant figures expected to be about 10 per cent above pre-pandemic levels. However, the exceptional figures reported for the 2022/23 winter season will not be surpassed. Consequently, a decline of 4 per cent in Swiss guests is expected for the coming winter.

• Regional differences: There could be a few shifts in the coming season caused by weakening catch-up effects. Regions that saw increases in winter 2022/2023 could suffer negative growth rates. American guests in particular, who exceeded the norm by 10 per cent last winter, are unlikely to repeat this growth in the coming season. Their numbers have recovered and could level off or even show slightly negative growth after their sharp rise this year.

• Europe: On the other hand, KOF expects to see an increase in European visitors – especially those from Germany – as the economic environment improves.

• Climate change risk: Climate trends will increasingly impact winter tourism and constitute a growing forecasting risk. As seen in March 2023, significant changes can affect short-term bookings. For example, the lack of snow in March caused a sharp decline in overnight stays.

Contact

KOF FB Konjunktur

Leonhardstrasse 21

8092

Zürich

Switzerland