KOF Business Tendency Surveys: Situation Is Picking Up

- KOF Business Situation Indicator

- KOF Bulletin

In October, the KOF Business Situation Indicator for the Swiss private economy rose for the fourth consecutive time. It looks as if the recovery of the recent summer months will continue. Companies are also more confident with respect to their future development. Business expectations for the coming six months are more positive than they were in the middle of the year. The Swiss economy is carried along by a modest but steady tailwind.

Development by economic sector

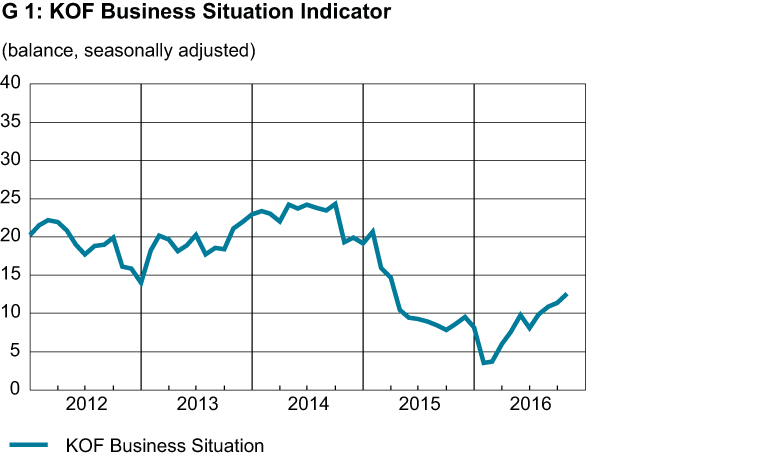

In October, the business situation improved in the majority of the industries under review (see G 1). The Business Situation Indicator rose in the manufacturing, construction, retail and wholesale industries as well as the banking and insurance sector and the hotel and catering industry. All in all, the increase of the Business Situation Indicator has a relatively broad basis. While project engineering offices experienced little change in their business situation compared to the previous month, and other services are slowing down their upward tendency, their situation remains nevertheless predominantly positive.

Business situation by region

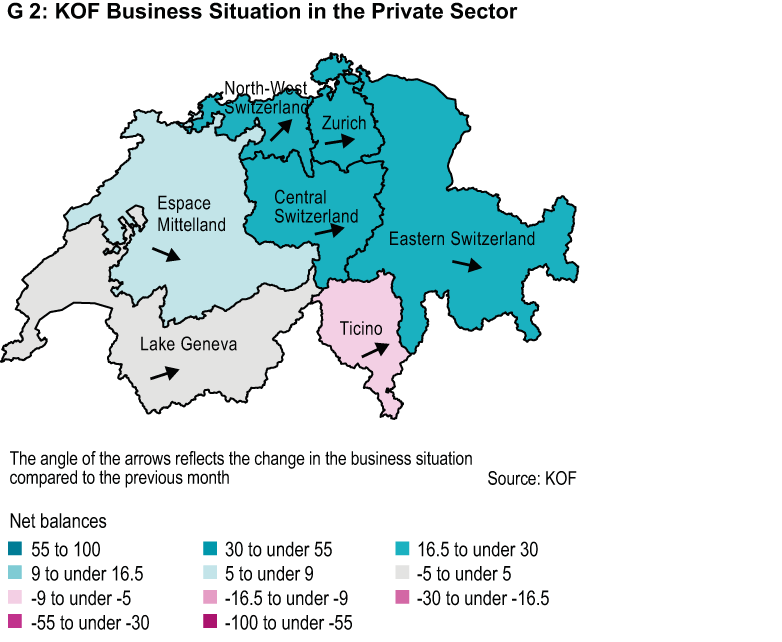

From a regional perspective, October presents a heterogeneous picture (see G 2). In North-West Switzerland, the situation improved considerably. On top of this, the business situation has also picked up in the Lake Geneva region, Central Switzerland, the Zurich region and Ticino, which still remains at the bottom of the league. In contrast, the situation in Eastern Switzerland did not quite reach the previous month’s level and Espace Mittelland reported a slight downturn. In the year-on-year comparison, Espace Mittelland is also the only region that reported a noticeable deterioration of its business situation in the last 12 months.

Recovery in the manufacturing industry and the construction sector

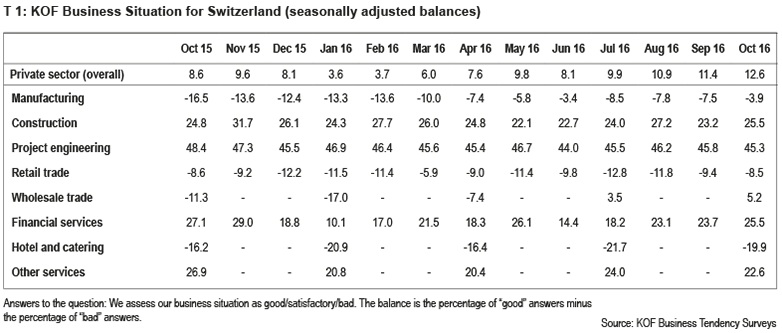

The business situation in the manufacturing industry continued to improve. All in all, the companies now consider the situation just about satisfactory, which is substantially better than last October. The latest progress in the business situation is predominantly due to the reports of the export-oriented companies. Complaints about the situation have declined considerably. Although the assessment has improved, order books and production are still seen as weaker than a year ago. Nevertheless, pressure to discount prices has diminished compared to the previous year and the erosion of margins is slowing down. Even so, the companies are not yet in a position to regain pricing power and raise prices. This is also reflected by the degree of capacity utilisation: At 81%, utilised capacity is still below average. On top of this, many companies still report insufficient demand. Other potential impediments, such as financial restrictions or labour shortages, are not playing a major role at the moment. In regard to further development, the companies are still moderately optimistic. They expect a slight increase in incoming orders and plan for a cautious increase of production.

The construction-related building trades and project engineering sector reported no change in their business situation, which they still consider predominantly favourable. In the building trades, the situation even improved to some extent in October. Both construction-related sectors are confident in regard to the business trend in the coming six months. Reports of insufficient order books have diminished among building companies. Machine utilisation has increased and companies plan to generally maintain their present staff numbers in the coming three months. Construction prices, however, are still in a downward spiral. Accordingly, the profit situation has suffered considerably. Although this trend should level off to some degree, construction companies are somewhat sceptical when it comes to their future earnings trend. Project engineering offices recorded a further rise in demand in the past three months and are hoping that this trend will continue in the coming quarter. Their fees are, however, still under pressure. Even so, the profit situation among project engineering offices in general is almost stable.

Retail more hopeful, situation in hotel and catering sector picking up

The business situation in the retail trade improved for the third consecutive time. Nonetheless, the situation is still predominantly unsatisfactory. Sales volumes have declined further and retailers once again report fewer customers than in the previous year. Accordingly, the profit situation is under pressure. Nevertheless, there is new hope among retail businesses who expect a significant increase in turnover and a deceleration of the price decline. In the wholesale trade, the business situation improved further and the profit situation remained stable. Although wholesale businesses are once again expecting price cuts, they also hope that demand for their services will pick up. Nonetheless, they plan to reduce staff numbers.

Following a slight downturn in the previous quarter, the situation in the hotel and catering industry has once again improved. In some way, the hotel and catering sector is treading water. At present, the business situation is nearly as unfavourable as at the beginning of the year. The current deterioration is predominantly due to the assessments of businesses in the big cities. In the mountain regions, the situation is improving and in the lake regions, it is at least stable. Although both the downward trend in demand and the erosion of the profit situation have slowed down recently, pressure to cut prices has increased once more. The companies hope that this will put a halt to the decline in demand. A breakdown into catering and hotel businesses shows that the situation in the hotel sector is no longer as unfavourable as it was a few months ago. The occupancy rate has risen substantially and declining turnover is now a rare occurrence. The situation in the catering sector is unsatisfactory. To some degree, this dissatisfaction reflects the unfavourable weather in early summer. Restaurateurs hope that demand will recover to some degree in the near future and that sales of food and drinks will not decline any further.

Banks and insurance companies report improved situation, other service providers less satisfied

In October, banks and insurance companies reported a slightly better business situation than in the previous month. Three months ago, the situation in this sector was not as favourable as it is now. The profit situation remained almost stable with institutes expecting a negative earnings trend in the near future due to rising operating expenses. Banks assess their business with domestic customers as good and their business with foreign customers as just about satisfactory. This indicates a noticeable improvement of their foreign customer business. In regard to domestic customers, the respondents reported more lively private customer demand while demand among institutional clients increased only marginally. Banks are still sceptical when it comes to the interest margin trend, while commission rates are unlikely to change much. Insurance companies hope for a rise in operating income in the next few months, not least because they expect a slowdown in the decline of net income from capital investments.

The other service providers reported a slight downturn of their business situation. However, all in all the situation remains predominantly favourable and slightly better than in the first half of 2016. Demand has picked up further and skills shortages are on the rise. The transport, information and communication segments, in particular, are slowly working their way out of the slump. The situation in the business support service sector is almost stable. Even so, rising demand could not prevent a rather negative profit situation trend in these two service segments.

Contact

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland