Global economic growth remains weak for the time being

According to the KOF Economic Forecast, the global economy will not pick up speed again until the second half of the year. The loss of household purchasing power caused by the high inflation rates of the past two years will dampen private consumption in the short term. In addition, the more challenging funding conditions and the high level of political uncertainty are weighing on investment momentum in many countries.

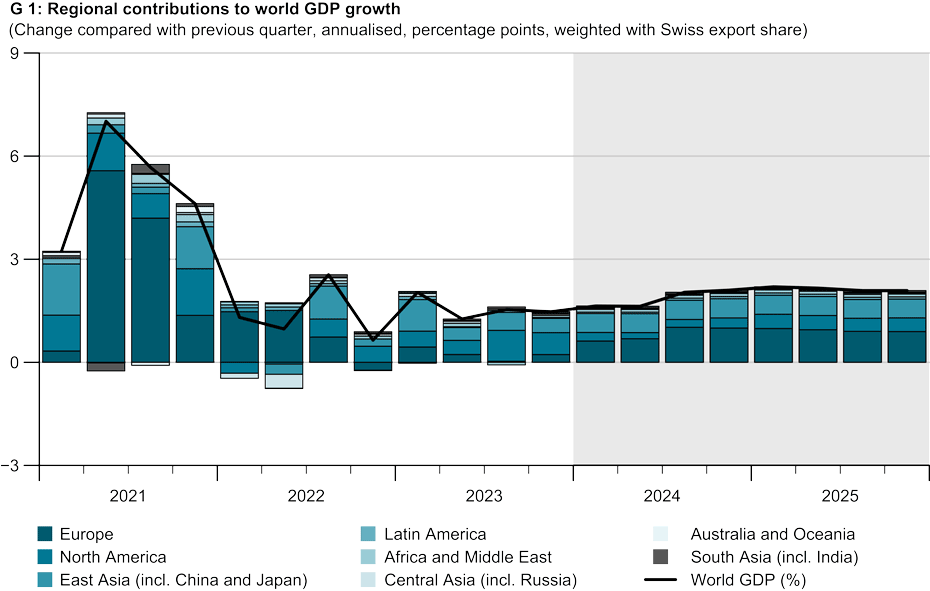

Global output was below average in the final quarter of 2023, with significant variations in economic growth across individual regions (see chart G 1). While US production has recently been stronger than generally expected due to continued robust private and public consumer spending, economic activity in Europe has remained weak.

Germany reported a decline in the fourth quarter of 2023 owing to negative net exports and a sharp drop in investment in the residential construction and manufacturing sectors, which is attributable to more challenging financial conditions, subdued earnings forecasts and heightened political uncertainty. The United Kingdom slipped into a technical recession in the second half of 2023 after a second consecutive quarter of negative growth. This is partly due to lower private consumer spending as a result of the loss of purchasing power caused by high inflation.

Global economic growth is likely to remain weak in the first half of this year before a modest recovery is expected in the second half of the year and, especially, next year on the back of a further decline in inflation, rising wages and improved financial conditions.

Decrease in inflation has slowed recently

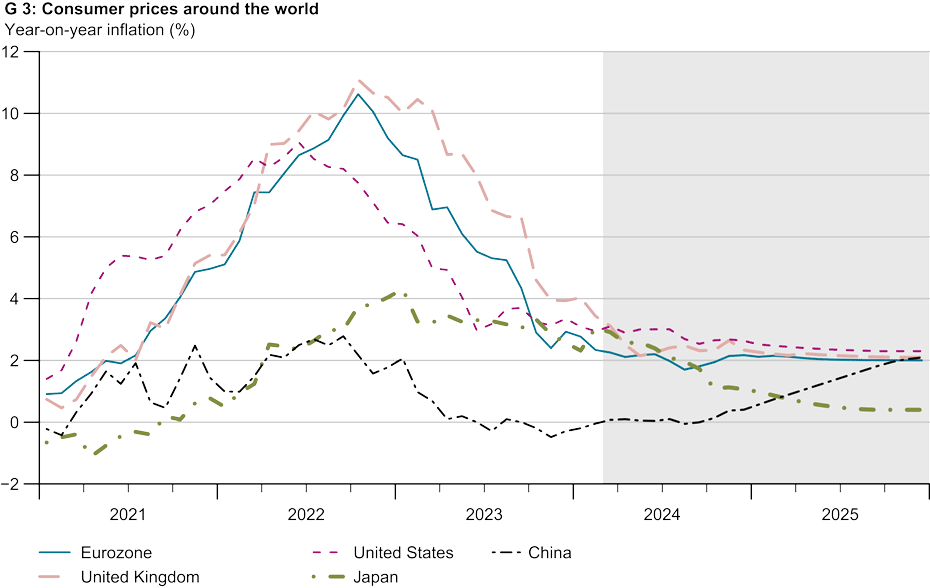

While consumer price inflation fell significantly last year owing to the decline in energy, commodity and intermediate goods prices worldwide, this downward trend has recently lost momentum. Over the past few months, inflation has fallen only slightly in the eurozone from 2.9 per cent in December 2023 to 2.8 per cent in January 2024 and in the United States from 3.4 per cent in December to 3.1 per cent in January. In the United Kingdom, on the other hand, consumer inflation recently edged up slightly from 3.9 per cent in December to 4 per cent in January.

One of the main reasons for this trend is that the weakening energy price component is gradually losing influence as energy prices fall below last year’s levels to a lesser extent. Although core inflation has also fallen recently in all countries, it is still well above central banks’ inflation targets.

Interest-rate cuts not expected before the middle of the year

The European Central Bank (ECB), the US Federal Reserve (Fed) and the Bank of England (BoE) completed their cycle of interest-rate hikes at the beginning of the second half of last year and have since left their key interest rates unchanged at their elevated levels. Given the recent cautious statements made at central banks’ press conferences, an immediate reduction in rates seems unlikely. This is due to ongoing upside risks to the medium-term inflation outlook, which partly depend on the level of wages going forward. By implementing a historic interest-rate hike, the Japanese central bank has abandoned its eight-year negative-rate monetary policy and raised the target range for its key interest rate to between 0 per cent and 0.1 per cent.

Given the weak economy and falling core inflation in the eurozone, KOF expects the ECB to make its first interest-rate cut in June of this year. The Fed is likely to follow suit in July by lowering the federal funds rate band, while the BoE is also likely to decide on its first rate cut at the end of June in view of below-average economic growth.

Economic recovery starting in the second half of the year

Global economic growth is likely to remain weak in the first half of 2024 and only pick up slightly in the second half of the year and, especially, next year. The loss of household purchasing power owing to the high inflation rates of the past two years will dampen private consumption in the short term. In addition, the more challenging funding conditions and the high level of uncertainty as well as the cyclical slowdown in global demand are weighing on investment momentum in many countries.

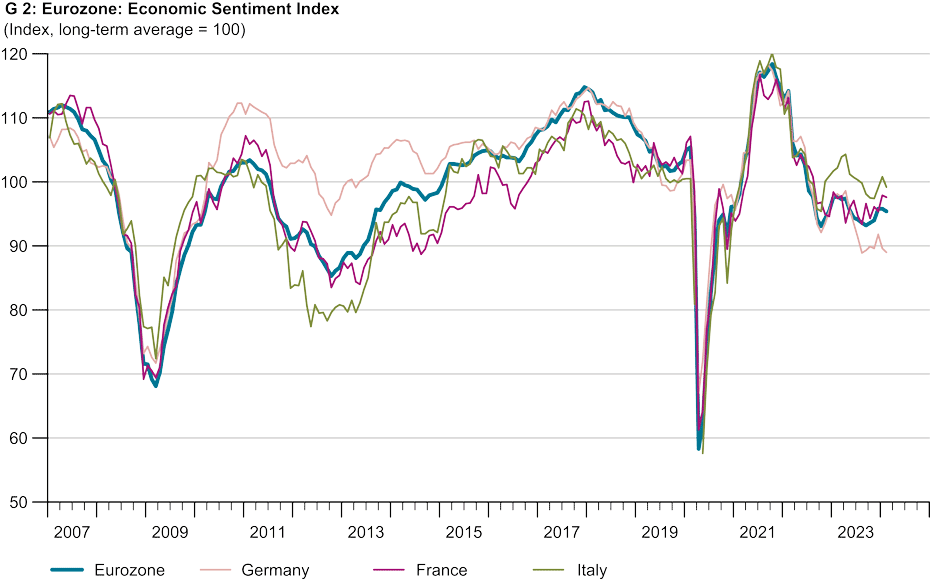

This economic trend is also illustrated by key leading indicators, which have deteriorated noticeably for many countries in recent months (see chart G 2). A combination of rising wages and continually declining inflation as well as the prospect of lower interest rates should boost private consumption and investment during the second half of the year. KOF expects global GDP weighted with Swiss exports to increase by 1.6 per cent for 2024 as a whole (winter forecast: 1.6 per cent). The corresponding forecast for 2025 is 2.1 per cent, which represents a slight upward revision compared with the winter forecast (2.0 per cent).

Sharp decline in inflation over the course of the year

Consumer price inflation is likely to fall further owing to the continued easing of energy price pressures and the current weakness of the global economy (see chart G 3). In addition, commodity and intermediate product prices are expected to weaken, with higher wage increases preventing inflation from levelling off faster.

Inflation in the eurozone is likely to be only slightly above the central bank’s target by the end of the year, while inflation rates in the United States and the United Kingdom should remain elevated until mid-2025 as a result of stubborn price increases in housing costs and in the services sector. By contrast, the decline in core inflation is likely to be less rapid as the lower cost of intermediate products will have only a gradual impact on end prices.

Various risks remain

This forecast was prepared on the technical assumption that the oil price and other energy prices would rise only slightly (1.5 per cent per year) up to the forecast horizon. Given the persistently uncertain environment, forecasting risks remain diverse and predominantly on the downside.

Core inflation could stabilise on the back of unexpectedly strong second-round effects, which would prompt central banks to delay interest-rate cuts. Restrictive funding conditions could cause instability in financial markets and trigger property-related and banking crises. In addition, intensifying geopolitical conflicts could again fuel higher energy prices and uncertainty and put further pressure on the real economy. One upside risk is that private consumption could be stimulated by unexpectedly strong real wage growth.

Contacts

KOF FB Konjunktur

Leonhardstrasse 21

8092

Zürich

Switzerland

KOF FB Konjunktur

Leonhardstrasse 21

8092

Zürich

Switzerland

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland