Investment on the rise, but not in all sectors

The results of the semi-annual KOF Investment Survey point to a nominal increase in investment of 8.2 per cent in 2024, driven by technological progress and supported by the service sector. By contrast, industry and construction are reporting a slowdown or even a decline in their investment plans owing to funding shortages and a downturn in demand.

After investment growth slowed last year, the pace of gross fixed capital formation is likely to accelerate in the current year. This is shown by the findings of the latest KOF Investment Survey from autumn 2023, according to which the firms surveyed expect their spending on fixed assets to rise by 8.2 per cent in nominal terms in 2024. Last year they were expecting to see growth of 5.1 per cent.

However, these stable investment forecasts in the aggregate should not obscure the major differences between individual sectors. The expected increase in investment spending in 2024 will be driven primarily by firms in the services sector (up by 10 per cent). In contrast, industry and construction are slowing their pace of investment compared with last year. After manufacturing companies raised their capital spending by 5 per cent last year, they are planning a 4 per cent increase for the current year. Firms in the construction industry are actually intending to reduce their investment by 14 per cent after boosting it by 3 per cent last year.

This planned investment expenditure will primarily be channelled into the construction and conversion of industrial and commercial property. The companies surveyed intend to increase their construction spending by 12.7 per cent in nominal terms this year. Investment in research and development is set to rise by 8.2 per cent in 2024. In contrast, the expected growth in equipment spending is below the long-term average at 2.8 per cent. All figures are based on a method that has been modified since the latest survey to identify and adjust outliers in the investment totals from firms’ quantitative responses (see box).

Technological progress driving investment growth in the current year

The capital expenditure figures collected for 2024 are merely plans whose realisation was not certain at the time of the survey. In order to determine the uncertainty in the rates of change resulting from these plans, firms were asked about the certainty of realising their planned spending. In autumn 2023, 13 per cent of companies rated their investment plans for 2024 as uncertain. Compared with last year, this realisation certainty has increased slightly on balance but remains below its pre-pandemic average. Uncertainty in the manufacturing sector has grown significantly. This reflects the fact that the outlook for the economy and funding conditions is more uncertain than it has been for a long time.

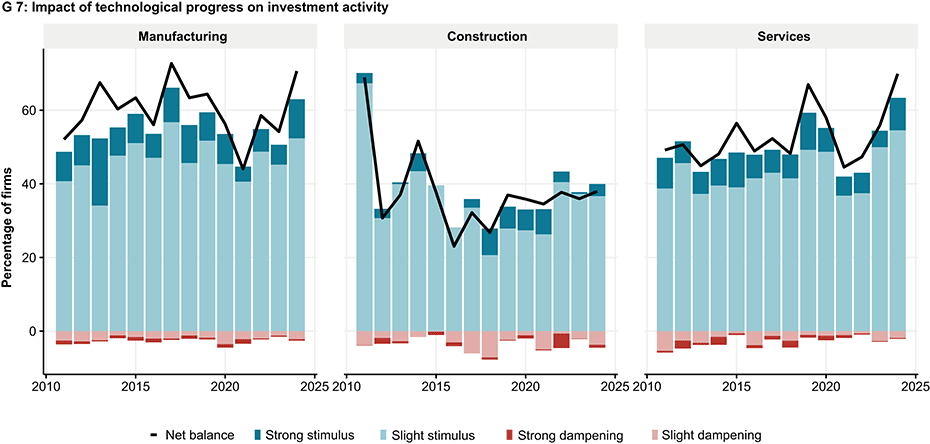

The driving force behind investment growth in the current year is technological progress. Its importance as an influencing factor has risen on balance from 53.1 points to 68.4 points compared with last year (see chart G7). This trend can be observed in all sectors but is strongest in manufacturing and services. Around 63 per cent of the firms surveyed in both sectors state that their investment plans are being positively affected by technology. In the construction industry this proportion is significantly lower at 40 per cent of companies.

Funding shortages and demand expectations weighing on investment prospects

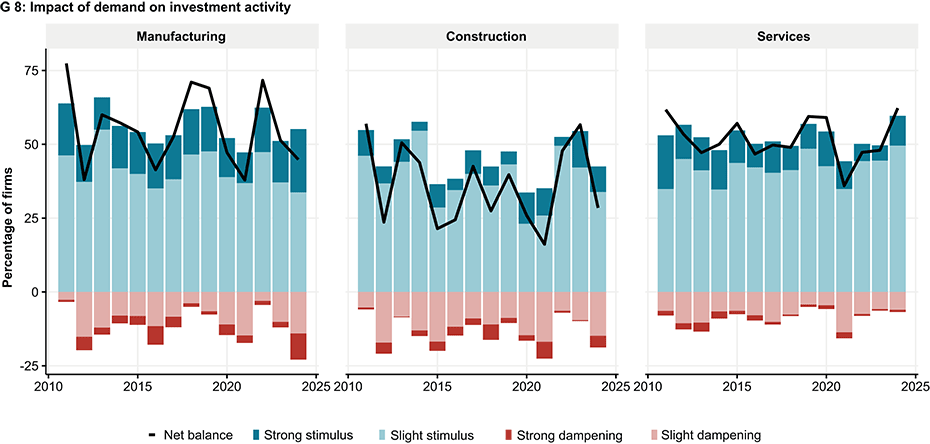

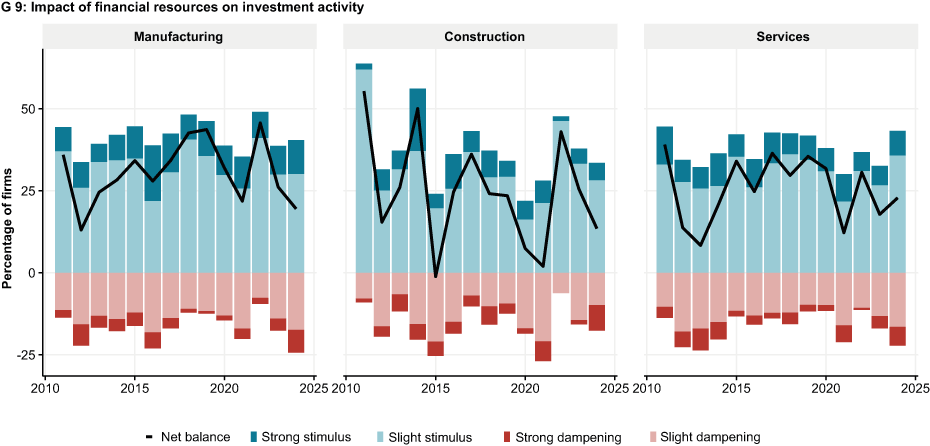

By contrast, expected demand and available financial resources are having an increasingly dampening effect on investment plans, particularly in sectors where companies expect investment growth to slow or even decline. In industry and construction, both of these influencing factors are having a significantly less positive impact on investment plans for 2024 than a year ago.

When asked about the expected level of demand, around a fifth of the firms surveyed stated that demand would slightly or significantly curb investment this year (see chart G8). This equates to a doubling compared with last year. When asked about their financial resources, almost a quarter of industrial companies reported a dampening effect on their earnings – more than at any time since the survey began in 2010 (see chart G9). In the construction industry the corresponding figure is 18 per cent of the firms surveyed. The background to these funding shortages is likely to be cost increases in areas such as energy, rents, interest rates, staff and materials.

Investment in environmental protection is gaining in importance

The most important investment objective continues to be the replacement of existing assets. At the same time, spending on environmental protection and on complying with trade law requirements has continued to gain in importance. More than half of the firms surveyed stated that they intended to make such investment this year. The corresponding figure in autumn 2022 was 47 per cent of companies.

In contrast, the importance of investment in expanding production and services has decreased slightly. Less than 60 per cent of companies intend to increase their operational capacity this year (compared with 64 per cent in autumn 2022). This trend is being accompanied by a contraction in the range of products and services, particularly in industry. This is incurring restructuring costs and reducing the funds available for investment.

Economic growth is strongly influenced by corporate investment activity. For this reason, the KOF Swiss Economic Institute at ETH Zurich conducts a survey of domestic firms every spring and autumn. The semi-annual survey carried out in autumn 2023 covers the period from 2 October to 24 December 2023. Of the 5,667 businesses contacted, 2,346 responded, which equates to a response rate of 41 per cent.

Methodological adjustments to the calculation of investment growth rates

Methodological adjustments were made to the calculation of investment growth rates when evaluating the KOF Investment Survey from autumn 2023. These growth rates are based on the quantitative responses from the firms surveyed regarding their existing and planned investment. However, these rates are susceptible to extreme values if, for example, companies state their investment in thousands of Swiss francs in one period and in millions of Swiss francs in the next. In addition, very high investment amounts can distort the overall outcome as they are included in the weighting process.

Previously, extreme investment amounts were identified and treated as outliers as part of an ad-hoc procedure. The latest survey has introduced a new, data-supported method of identifying and treating outliers. This procedure consists of two steps and is applied at sector aggregate level for each survey. The first step is to treat the growth rates by identifying and excluding rates outside the one-and-a-half interquartile range (‘box plot rule’) as outliers. The second step is to treat the investment totals by winsorising the amounts above the 95th percentile.

The new method has been retrospectively applied to all previous surveys. This completely revises the time series of investment growth rates. In addition, the new method may also have an impact on the other time series because the investment totals of the companies surveyed are included in the weightings of their responses.

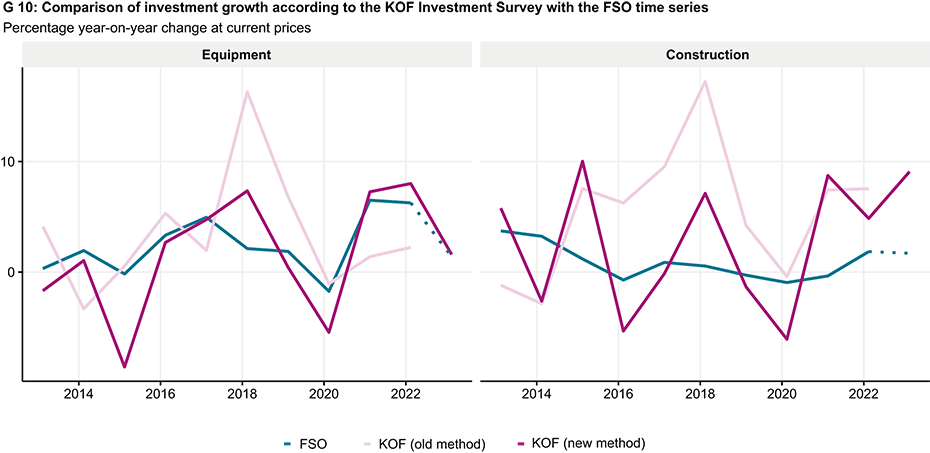

To validate the new method, we can compare the investment growth rates under the old and new methods with the corresponding figures from the Swiss Federal Statistical Office (FSO). Chart G10 shows the annual growth in equipment investment (left) and construction investment (right) under both methods for the results of the KOF Investment Surveys in the autumn of the current year and compares it with the corresponding components of gross domestic product by type of use according to the FSO, where the rate for 2023 corresponds to the latest KOF Economic Forecast from December 2023. The new method of identifying and treating outliers significantly increases their correlation with the corresponding FSO figures for both equipment investment and construction investment. The correlation for equipment investment under the new method is 0.85 (under the old method it was 0.05). The correlation for construction investment under the new method is 0.33 (under the old method it was minus 0.36). It should be noted in this comparison that the KOF Investment Survey only covers the corporate sector. The FSO data includes investment in the institutional sectors as well as agriculture and mining.

Contact

KOF FB Konjunkturumfragen

Leonhardstrasse 21

8092

Zürich

Switzerland