“The battle against inflation has not yet been won”

Alexis Perakis, monetary policy expert at KOF, talks in this interview about his predictions for inflation, interest rates and the Swiss franc exchange rate this year. He considers the current debate about interest-rate cuts to be premature.

Inflation has recently fallen in almost all currency areas. In addition, central banks in the United States, the eurozone, the United Kingdom and Switzerland once again decided not to raise interest rates further at their meetings before Christmas, meaning that the current cycle of rate hikes is probably over. Has inflation now been defeated?

Of course, it is good news for the population and the central banks that inflation is falling. But it is still too early to declare victory in the fight against inflation. Starting a debate on interest rate cuts is not a problem in itself as long as you continue to monitor the important figures very closely. Even if many price indicators are moving in the desired direction, we should not rejoice too soon, but rather wait a few more months or quarters and observe the evolution of prices. In fact, core inflation is still high in many countries and this means that the battle against inflation has not yet been won. Only when the current trends prove to be stable can we talk about realistic interest rate cuts.

Central banks have been heavily criticised in the past because, according to their critics, they reacted too late to rising inflation. In hindsight, did central banks perhaps do a good job after all? Inflation has started to fall, and it seems realistic that the economy will achieve a soft landing without triggering a major economic slump.

Looking back, we have to acknowledge that inflation in many currency areas has far exceeded the level of price stability in the last two years. This is not encouraging. The current outlook for the US is certainly more positive than for Europe, where not all countries are likely to emerge from the inflation crisis unscathed. Switzerland has definitely come through the crisis well. This is mainly due to the fact that inflation was never as high as in the eurozone because of the nominal appreciation of the Swiss franc.

“Looking back, we have to acknowledge that inflation in many currency areas has far exceeded the level of price stability in the last two years. This is not encouraging.”Alexis Perakis, KOF monetary policy expert

When does KOF expect to see the first interest-rate cuts in the major currency areas, and when could the Swiss National Bank (SNB) lower interest rates again?

We do not expect interest rates to be cut either in the US or in the eurozone before the middle of this year. If interest rates are cut, it will probably only be by small increments of 25 basis points. The SNB could then follow suit with a slight delay at the end of 2024 or the beginning of 2025.

Will interest rates fall first in the US or the eurozone?

Given its weak growth, the eurozone would actually benefit more from an interest-rate cut than the United States, where the economy is doing much better. Nevertheless, I believe that the first interest-rate cut will occur in the US. Christine Lagarde, the President of the European Central Bank (ECB), explicitly stated in her press conference before Christmas that the ECB Governing Council had not yet discussed interest-rate cuts. Jerome Powell, the Chairman of the US Federal Reserve (Fed), on the other hand, has – at least according to the interpretation of many market participants – shown himself to be more open to interest-rate cuts this year.

“We expect prices in Switzerland to rise by 1.7 per cent this year and by 1 per cent next year.”Alexis Perakis, KOF monetary policy expert

KOF’s Monetary Policy Communicator (MPC), which is an instrument for measuring the ECB’s communication, is currently at exactly 0.00. How should this result be interpreted?

The MPC translates the statements made by the ECB President at her regular press conferences into an index. A value of zero means that the ECB’s forward guidance on rising and falling prices is balanced. This can be interpreted as follows: the ECB does not expect any major price fluctuations on average and interest rates in the eurozone will therefore flatline for some time. This supports my thesis that any interest-rate cuts in the eurozone before the middle of the year are unlikely.

How much pressure will Switzerland be under if the Fed and the ECB cut interest rates?

Fairly little in the current situation. The SNB sets its interest rates based on domestic inflation figures. Interest-rate differentials that arise with major trading partners, such as the EU and the US, can of course also play a role. Differences in key interest rates, for example, can have an impact on exchange rates. However, the SNB does not have to react immediately, or at least not to the same extent. The current size of the interest-rate spread provides a buffer for the SNB’s monetary policy, given that the inflation differential with the eurozone has narrowed in recent months.

What is KOF’s latest inflation forecast?

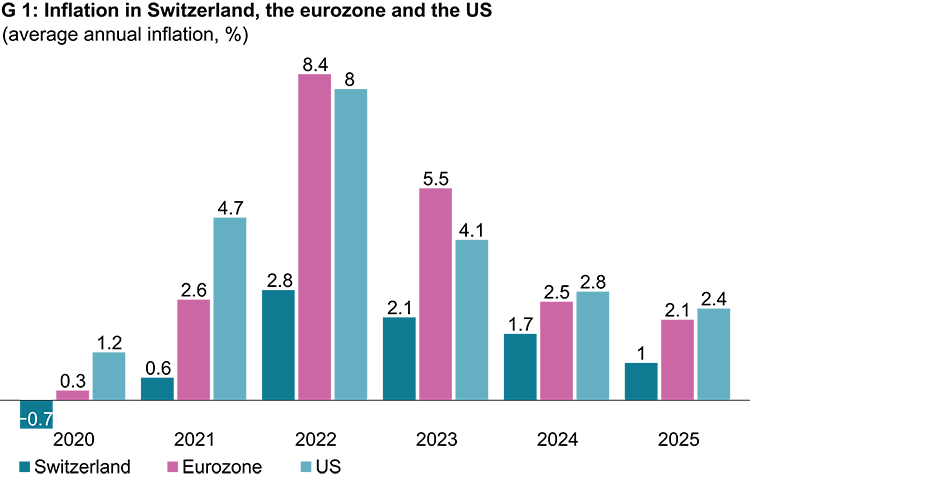

We expect prices in Switzerland to rise by 1.7 per cent this year and by 1 per cent next year. This would bring inflation back within the SNB’s target range. We are forecasting that inflation in the eurozone and the US will fall but – at an annual average of 2.1 per cent and 2.4 per cent respectively – will still be slightly above the ECB and Fed targets next year (see chart G1).

What are the main drivers of inflation in Switzerland?

Rent increases are the most important driver of inflation and at the same time the greatest uncertainty factor in the inflation forecast. This is because it is not yet possible to estimate exactly how the rise in the mortgage reference interest rate will affect rents in Switzerland. In our latest forecast, for example, we adjusted the extent of rent increases downwards based on the available data for November. For the first time, this data includes the effects of rent increases in recent months, which were lower than expected. It is important to note that rents are only collected on a quarterly basis and the next figures will therefore only be available at the beginning of March. The question now is whether the increase in rents was truly more restrained or whether it will be included in the CPI, the national consumer price index, with a time lag and thus observed with a delay.

How does KOF expect the Swiss franc/euro exchange rate to evolve over time?

We are assuming that the real exchange rate between the Swiss franc and the euro will remain stable. As there is still an inflation differential between Switzerland and the eurozone, the franc will continue to appreciate in nominal terms.

Contacts

KOF FB Data Science und Makroök.

Leonhardstrasse 21

8092

Zürich

Switzerland

KOF Bereich Zentrale Dienste

Leonhardstrasse 21

8092

Zürich

Switzerland