KOF’s Business Tendency Surveys: Swiss economy lacking stimulus

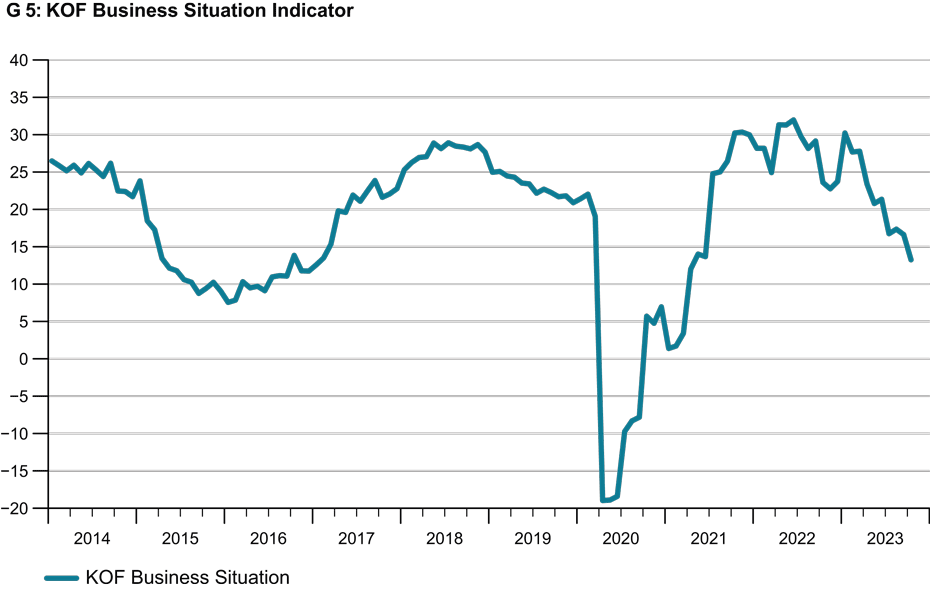

The KOF Business Situation Indicator for the Swiss private sector, which is calculated from KOF’s Business Tendency Surveys, fell in October for the second month in a row (see chart G5). Following a modest decline in the previous month, business activity cooled significantly in October. By contrast, companies’ business expectations for the coming six months are almost unchanged and more or less average on a medium-term comparison.

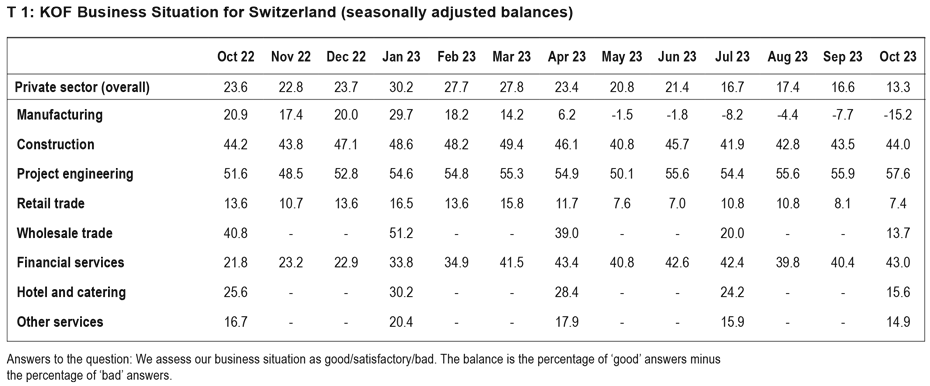

The business situation in October deteriorated in the majority of sectors surveyed. The adverse trend in the manufacturing sector in particular is weighing on the Swiss economy. However, the hospitality industry and the wholesale trade also suffered setbacks in October. Although the trend is slightly negative in other services and in the retail trade, it is very slightly positive in construction. There is a clearly visible improvement in the project engineering sector and in financial and insurance services (see table T1).

Business outlook offers a glimmer of hope

The majority view of business activity over the coming six months has reversed. While the manufacturing sector was still predominantly sceptical in the summer, confidence is now on the rise. The outlook has also brightened in financial and insurance services, the retail trade, project engineering, construction and other services. On the other hand, optimism in the hospitality industry is declining slightly and wholesalers are becoming much more sceptical. Overall, these business expectations reflect the budding hopes for the performance of the Swiss economy going forward.

Price buoyancy continues to decline

Companies’ pricing intentions are now less focused on increases than before, and the upward pressure on prices caused by Swiss firms is weakening. The manufacturing sector, the retail trade and other services are planning to raise prices less sharply than before. In the construction sector, on the other hand, price increases are being considered slightly more frequently than in the previous month.

Companies expecting smaller wage rises than in autumn of last year

KOF also asks firms about their expectations regarding wage levels over the next twelve months. As of October 2023, companies were expecting nominal wage increases to average 1.9 per cent over the year as a whole. This is a smaller rise than in the autumn of last year. At that time they had factored in an increase of 2.5 per cent.

Firms in manufacturing, the retail trade and wholesalers currently expect to see a slightly below-average wage round compared with the rest of the sector. Wage adjustments in the hospitality industry, construction and the project engineering sector could be above average. Overall, however, wage negotiations are likely to be intense as companies continue to complain about widespread labour shortages, although the problem has become less acute in all sectors except construction in the autumn and concerns about weak demand are increasing.

The manufacturing sector remains in a downward spiral

The Business Situation Indicator for the manufacturing sector is declining again. Dissatisfaction is increasing not only among export-led companies but, in October especially, among domestically focused ones as well.

Utilisation of technical capacity is declining noticeably. Capacity utilisation has been falling all year, especially in the chemical and pharmaceutical sectors. Companies’ earnings are increasingly coming under pressure. However, survey respondents hope that the bottom of the market will soon be reached and that demand will tend to pick up in the near future.

The situation in the building-related sectors of the economy is encouraging

Business in the project engineering and construction sectors, which are both associated with building activity, is improving. In both sectors, however, demand is no longer as buoyant as it was a year ago. As a result, the provision of services is being expanded more cautiously than before. Capacity utilisation in the construction sector has fallen slightly further. It is thus still above average on a medium-term comparison but significantly lower than at the beginning of the year.

Business activity is cooling in the two trading sectors

Although the Business Situation Indicator for the retail trade is again slightly down, the business outlook for the coming half year is more confident than before. Sales of goods have weakened in the past three months, however, so retailers increasingly consider their warehouses to be too full.

Companies hope to see sales growth in the near future and are particularly optimistic about the food sector. The Business Situation Indicator for the wholesale sector fell for the third quarter in a row. The wholesale trade in producer goods is responsible for the latest downturn. The Business Situation Indicator for consumer-goods wholesaling – primarily in the food and beverages sector – is not falling any further.

Business activity in the hospitality industry has peaked for the time being

Business in the hospitality industry deteriorated significantly in October. The situation is less encouraging than in the summer in both the food-service and accommodation sectors. Accommodation providers in the major towns and cities as well as food-service businesses in all tourism areas – mountains, lake regions, major towns and cities – have suffered setbacks. The number of overnight stays by domestic guests is performing sluggishly, while those by overseas guests continue to rise significantly.

Food-service providers are registering hardly any growth in sales of beverages and food. However, they are hoping to see sales increase again in the current quarter. Complaints about staff shortages are still widespread among food-service providers but are no longer as serious as in the autumn of last year. A similar pattern can be seen in pricing intentions, with both food-service businesses and accommodation providers frequently planning price increases, although they are not quite as widespread as in the autumn of last year.

The situation of financial and insurance service providers is improving again

Business activity in the financial and insurance services sector continues to improve. These institutions’ expectations about their levels of business over the coming six months are also more confident than before. Their earnings situation has seen an improvement in the past three months, although this is not quite as pronounced as before.

Other service providers report good capacity utilisation

Business activity in other services changed little in October. Capacity utilisation at service companies remains high, although their earnings situation is hardly improving. Service firms are still planning to increase their staffing levels, but not as significantly as in recent quarters.

Contact

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland