Gloomy outlook for the global economy

The international economy has slowed. Above all, the effects of China’s weakness and of restrictive monetary policy are weighing on the global economy.

While the pressures of high inflation are easing, the global economy is still feeling the effects of China’s weakness and of restrictive monetary policy. Inflation rates have retreated from their double-digit highs, and monetary tightening is also likely to have peaked. KOF expects that this dampening effect will hit economies with a time lag and weigh on the economic outlook going forward. International trade is predicted to continue to slow, reflecting weak global demand, the shift from goods to services, the appreciation of the US dollar and the imposition of further trade restrictions.

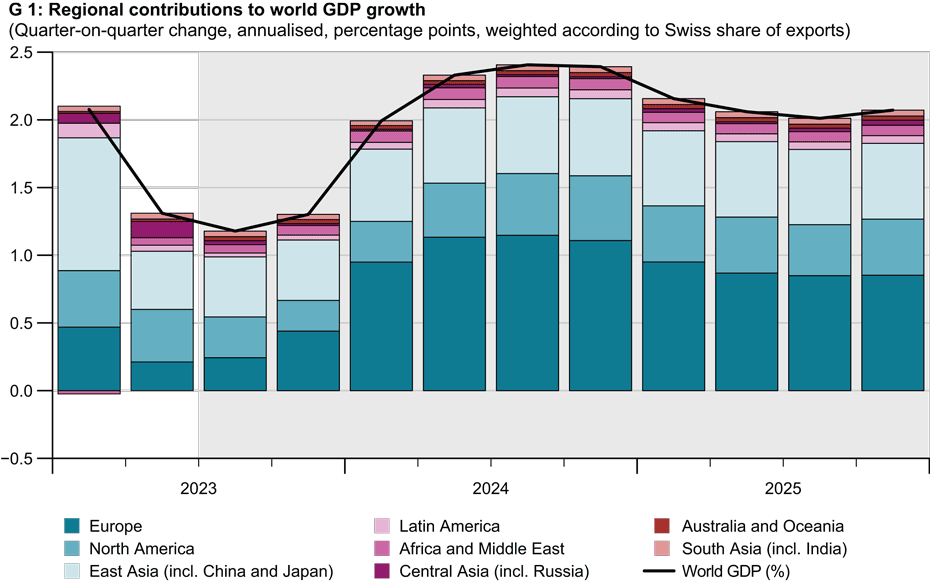

The global economy continued to slow at the beginning of the second half of 2023 owing to weakening growth in the services sector and a worsening downturn in manufacturing. Consequently, KOF is forecasting that global economic growth will be fairly low for the rest of the year (see chart entitled ‘Regional contributions to world GDP growth’). Falling but still high inflation and the more challenging financial environment are likely to dampen private consumption, international trade and investment activity.

Inflation continues to ease but remains elevated

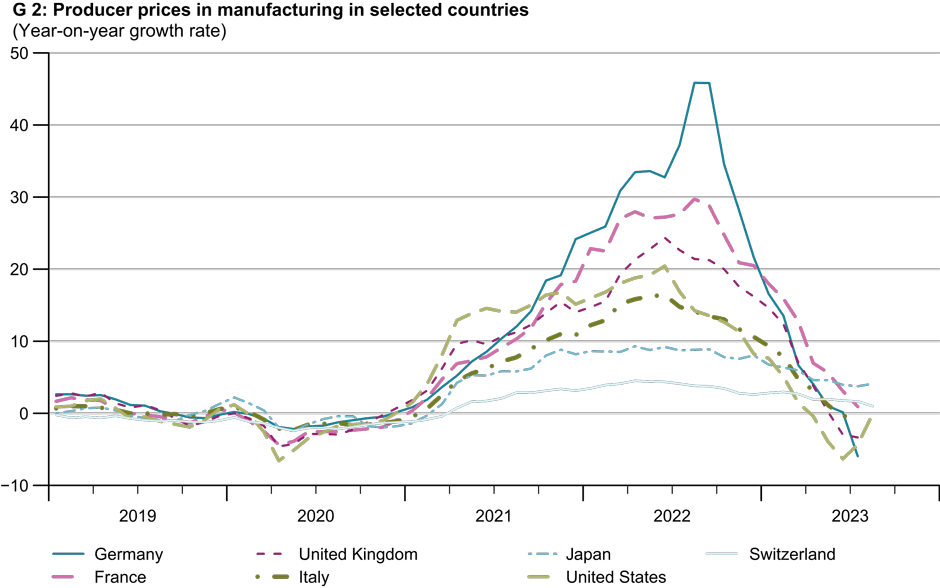

Producer prices have continued to normalise in recent months and in most countries have largely approached pre-pandemic growth rates or have even declined (see chart G 2). In addition to the expiry of base effects, the normalisation of price rises is largely due to the falling prices of energy, raw materials and intermediate goods as a result of the further easing of supply chain problems and materials shortages.

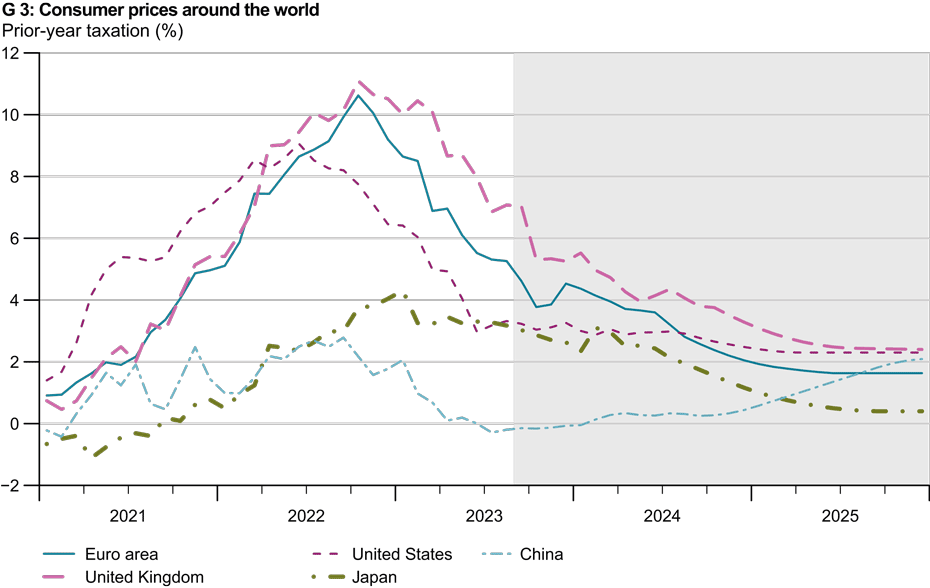

Although consumer price inflation remains elevated worldwide, it has been further reduced thanks to falling petrol, gas and electricity prices, the build-up of gas reserves, the electricity price cap in Europe, the normalisation of supply chains, weak demand in China and the expiry of base effects (see chart G 3). However, food price inflation remains elevated. Furthermore, a tight labour market with strong wage growth and high corporate profits is leading to second-round effects that are fuelling core inflation.

This can be observed especially in the case of services, where inflation continues to rise. Inflation in the euro area remained at 5.3 per cent in August, with the core rate declining from 5.5 per cent to 5.3 per cent. Inflation in the US has actually picked up in the last two months, rising from 3.3 per cent to 3.7 per cent in August, with core inflation at 4.3 per cent. UK inflation declined from 7.9 per cent to 6.8 per cent in July, while core inflation remained at 6.9 per cent. Meanwhile, consumer price deflation has been taking place in China since August.

Monetary tightening may have peaked

Inflation has fallen sharply in the developed economies and is likely to continue to decline owing to the recent increasingly restrictive monetary policy and weakening demand. However, any further decline in inflation will be somewhat slower, as base effects have already largely run their course and the oil price has recently started to rise again. The European Central Bank (ECB) has raised key interest rates in three stages of 25 basis points each since May, which means that the main refinancing rate currently stands at 4.5 per cent. Given the worsening economic outlook in the euro area, any further interest-rate hike seems rather unlikely. At the same time, it is fair to assume that the 2 per cent target will not be reached any time soon.

At its meeting in July the US Federal Reserve raised the target range of the federal funds rate by 25 basis points to 5.25-5.5 per cent in one go and then did not make any further interest-rate moves in September. Given the recent price data and the easing in the labour market, KOF does not expect to see any further interest-rate adjustments. In contrast to many other countries, the recently higher wage costs, commodity prices and petrol prices in the US have pushed up producer prices, which will probably be partially passed on to consumers, which means that inflation is likely to remain at around 3 per cent for a while.

The Bank of England (BoE) has also had to follow up with further interest-rate hikes and has raised its key interest rate from 4.5 per cent to 5.25 per cent since June. Even though inflation in the UK remains very high, the BoE decided against any further interest-rate hikes in September owing to the surprisingly sharp declines in inflation in recent months. KOF does not expect the BoE to raise interest rates any further.

There is still considerable uncertainty about the impact of monetary tightening, the time lag of its effect and the appropriate path to normalisation. However, KOF does not expect the ECB, the Fed and the BoE to cut their key interest rates for some time yet. The latest sentiment indicators point to a further slowdown in global output. Purchasing managers’ indices show a decline in both output and new orders in the manufacturing sector for the fourth time in a row in August, while a certain stagnation is becoming increasingly apparent in the services sector. This decrease is particularly pronounced in the euro area and the UK and also suggests a slowdown in the US.

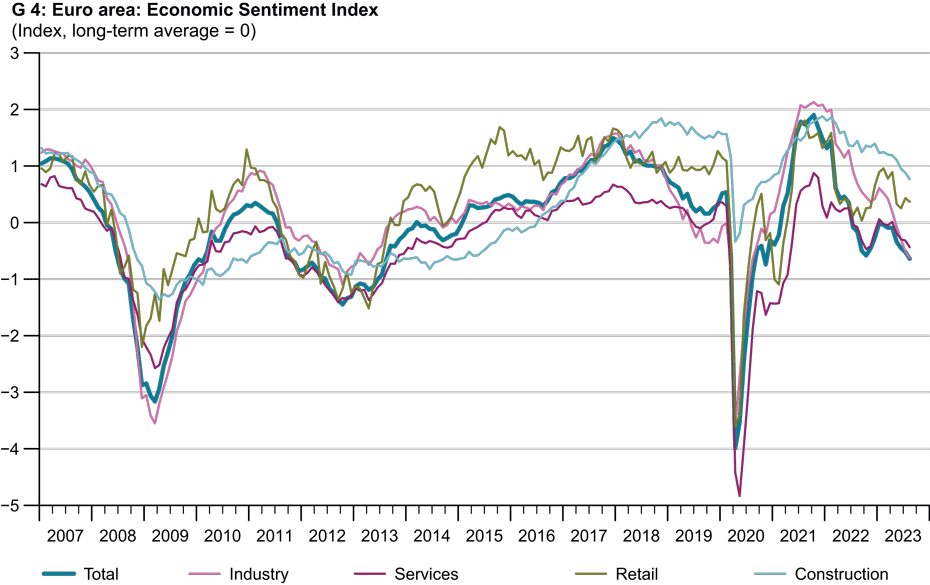

A slowdown is evident in the labour market as well. Employment growth has slowed sharply in recent months and, given the current excess capacity, the labour force is likely to be reduced over the coming months. Sentiment indicators in the euro area have recently fallen across all sectors, and the overall index recorded its seventh consecutive decline in August. This points to weak momentum over the coming months (see chart G 4).

Little growth in global output over the further course of the year

Given continued high inflation, the restrictive interest-rate environment and low foreign demand, KOF expects to see only weak economic activity in the euro area. However, the disbursement of the NextGenerationEU programme and real wage rises should support activity somewhat. The economy in the United Kingdom was surprisingly strong in the last quarter owing to wage increases in the public sector as well as robust private consumption. The UK should grow this year thanks to strong population growth, a robust labour market and fiscal measures. However, the broader outlook remains weak as a result of pressures from Brexit, persistently high inflation, and monetary tightening.

Economic activity in the US has risen surprisingly sharply recently. Investment momentum is picking up again and strong income growth is boosting consumption. However, the currently low savings ratio points to a depletion of savings and thus to lower consumption levels throughout the remainder of the forecasting period.

In China, the second quarter was more disappointing than expected. The country is currently suffering from a phase of weak economic activity, which is characterised by a real-estate crisis and resulting low consumer demand. Although the Chinese central bank has cut its key interest rate, it is still hesitant as it does not want to devalue the yuan too much. In addition, the government is reluctant to provide strong fiscal stimulus so as to avoid incurring any further debt. These factors are likely to weaken China’s economic activity over the entire forecasting period.

KOF is forecasting a 1.4 per cent increase in world GDP weighted by Swiss exports for 2023 as a whole. Rates of 1.9 per cent and 2.2 per cent are expected for 2024 and 2025 respectively. This is a minimal revision compared with the summer forecast (1.4 per cent for 2023 and 2.0 per cent for 2024).

Risks mostly on the downside

This forecast has been prepared based on the technical assumption that the oil price and other energy prices will increase only slightly (1.5 per cent per year) over the forecasting period. Given the continually uncertain environment, the majority of the forecasting risks are on the downside and mainly relate to the monetary policy outlook, the geopolitical environment and the state of the Chinese economy.

Consequently, there is a risk of inflation in the core rate becoming more entrenched owing to second-round effects, forcing central banks to take further action on interest rates. The high interest-rate environment could fuel renewed instability in financial markets and bank insolvencies. There is a possibility that these high rates in conjunction with high levels of government debt could cause turbulence in financial markets and force governments to implement austerity measures.

Moreover, any further destabilisation of the Chinese real-estate sector poses a major risk. It would cause the country’s economy to falter even more and have a negative impact on global demand. Finally, geopolitical tensions such as any renewed escalation of the war in Ukraine and the China-Taiwan conflict could trigger further commodity price shocks, exacerbate the East-West confrontation and further weaken globalisation.

Upside risks are that monetary tightening takes effect faster and more effectively, while inflation falls faster than expected, which could cause central banks to lower their policy rates to neutral levels sooner. There is also the possibility that savings will be reduced more than previously expected and boost private consumption. A surprising conflict resolution of the war in Ukraine and of the trade dispute between the US and China would have a positive impact on global trade. And, finally, the Chinese government could unexpectedly decide to provide fiscal stimulus packages to support the domestic economy, which would have a positive effect on the global economy.

KOF’s entire economic forecast is available here (in German):

Downloadhttps://ethz.ch/content/dam/ethz/special-interest/dual/kof-dam/documents/Medienmitteilungen/Prognosen/2023/VJA_2023_3_Herbst_Gesamtbericht.pdf (PDF, 2.1 MB)

Contacts

KOF FB Konjunktur

Leonhardstrasse 21

8092

Zürich

Switzerland

KOF FB Konjunktur

Leonhardstrasse 21

8092

Zürich

Switzerland

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland