Exports proving robust

Swiss foreign trade is holding up well despite global turbulence and the current weakness of major trading partners such as China and Germany.

Although Switzerland’s international trade weakened in the second quarter, it remains robust by global standards. Its strong focus on industries such as pharmaceuticals and watches – especially in trade with the United States – is providing stability. Given the existing inflationary pressures and the deteriorating global economic situation, however, the outlook for Swiss industry is worsening. After trade boomed in the first quarter of 2023 owing to the elimination of supply shortages, the annual growth rate is likely to slow throughout the rest of the year. The annual growth rate for exports of goods and services (excluding valuables) is thus 2.5 per cent. The growth forecast for imports has been adjusted to 4.6 per cent.

Downturn in world trade

The dynamics of the global economy have meant that the initial pandemic-driven surge in demand for goods as opposed to services has subsided, affecting Chinese exports in particular. This shift has implications for international trade and forms the basis of the challenges facing Switzerland’s industrial trade.

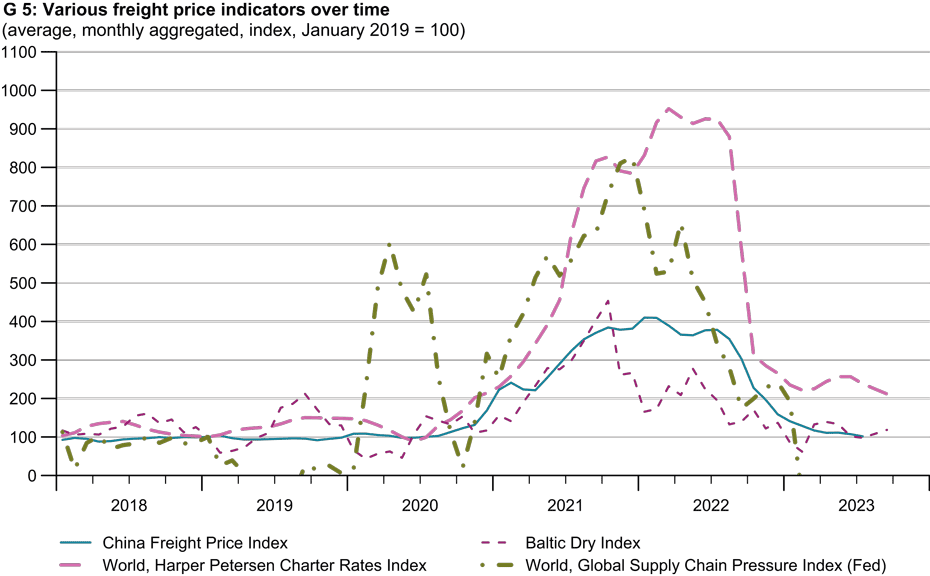

Supply chain shortages normalised and freight prices fell in the first quarter of 2023 (see chart G 5), which triggered a brief increase in exports and output. The rapid easing of trade barriers caused inventories to build up and trade figures to subsequently flatline in the second quarter of 2023 – a pattern that can also be observed in Switzerland’s industrial sector.

China’s economy has been in trouble since the pandemic. The slowdown of this economy is not an isolated event and is an international problem affecting global trade. This slowdown in China has caused a decline in global demand that has hit Switzerland’s main trading partners hard. Germany, a linchpin of Swiss industrial exports, is particularly vulnerable to these fluctuations in global demand. In addition, the European automotive industry faces another challenge: the rise of Chinese electric vehicles. This emerging industry poses a new competitive threat to Europe’s automotive sector, which is a major buyer of Swiss machinery and equipment.

Trade in goods: industry ailing while pharma holds up well

Facing a backdrop of global economic headwinds, Switzerland’s trade in goods is preparing for a subdued outlook, influenced primarily by the economic slowdown in key trading partners such as China and Germany. Following an encouraging first quarter of 2023, the goods trade suffered a decline across the board in the second quarter.

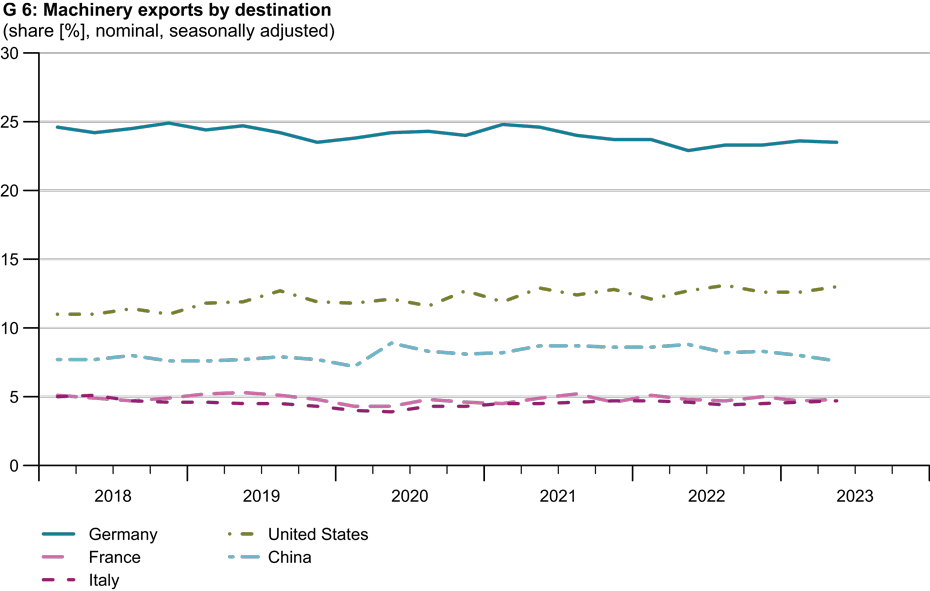

The machinery and equipment sector, which is highly dependent on Germany and China, saw exports fall by 6.2 per cent and imports dip by 7.8 per cent in the second quarter of 2023. Taking into account Germany’s substantial 24 per cent share of the demand for Swiss machinery and equipment, this sector faces a medium-term downturn, exacerbated by the weakening German economy (see chart G 6).

After reporting strong export growth of 5.2 per cent in the first quarter, the pharmaceutical sector saw a slight decline of 1.8 per cent in the second quarter. There are two reasons for this sector’s resilience. Firstly, pharmaceuticals are more cyclically resistant. And, secondly, a large share of Swiss pharmaceutical exports is accounted for by the US, which is currently performing better than expected, providing additional support for the sector. The watch sector also seems to be holding up well thanks to continued demand for high-end products.

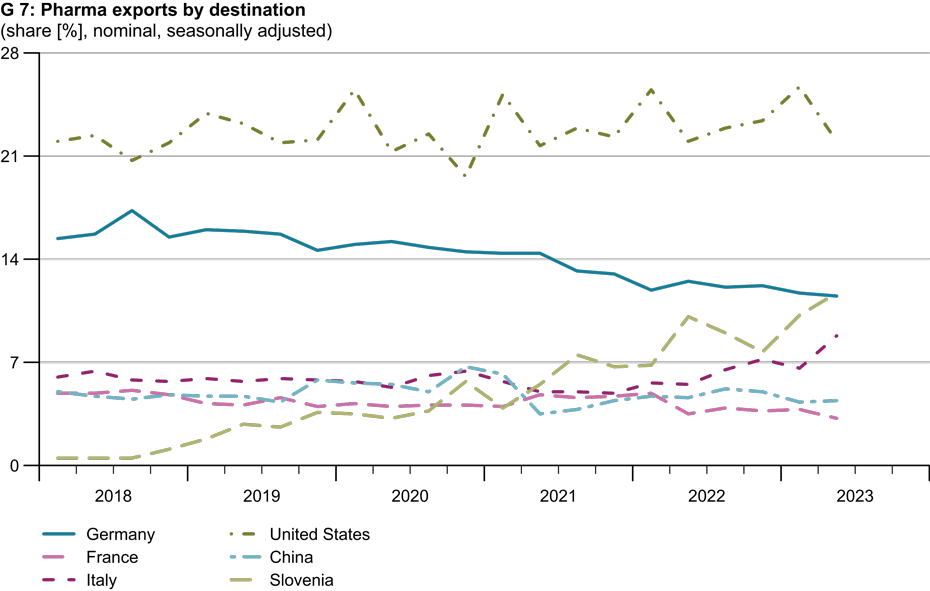

KOF expects to see subdued growth next year. Excluding valuables and transit trade, goods exports should increase by a moderate 1.6 per cent. In 2025, as the international economic situation becomes more stable, growth should gather pace and reach 3.9 per cent. This upswing will benefit the machinery and equipment sector in particular. Imports are expected to grow at the slightly faster rate of 2.3 per cent in 2024, after which the pace of growth will remain relatively constant. The higher growth rate expected for goods exports compared with imports indicates an increase in the trade balance. This trend underlines the structural robustness of the export-led Swiss economy and shows its resilience despite short-term challenges (see chart G7).

Services: a buffer against global economic volatility

While the goods trade faces a subdued outlook owing to the adverse global economic conditions, the performance of the Swiss services sector is more varied. According to KOF’s forecasts, service exports are expected to grow by 2.4 per cent and service imports by a significant 10.1 per cent this year.

Tourism remains a key driver of the services sector. The easing of international travel restrictions has meant that the influx of tourists, especially those from the US, has exceeded KOF’s previous forecasts and significantly strengthened service exports. European tourism figures have remained stable, while domestic tourism has exceeded initial expectations. However, there is a significant increase in tourism-related imports for 2023. This is attributed to the fact that the Swiss are increasingly opting for holidays abroad, and pent-up demand is being unleashed from the number of days’ vacation accumulated as a result of the pandemic.

There has been a decline in financial services, while the consulting sector is showing modest growth in both imports and exports. In the medium term, tourism will boost import growth at a rate that exceeds initial forecasts. Services exports are expected to increase significantly in 2024 and are predicted to grow by 6.6 per cent, mainly due to the European Football Championships. However, this upswing is expected to slow in 2025 and to level off at around 1.8 per cent. On the other hand, service imports are forecast to grow steadily and robustly in both 2024 (4.1 per cent) and 2025 (3.8 per cent), with tourism making a significant contribution.

Current account: stability in a world of volatility

The current account surplus for 2022 amounts to CHF 56 billion, which is a moderate increase of 7.1 per cent compared with the previous year. This rise is mainly due to the trade in goods. Following a crisis-ridden year with a negative balance, the surplus has regained its former strength and stabilised at the 2021 level.

As far as primary income is concerned, stagnation in real wages coupled with rising inflation has had a negative impact on the trade balance. This has been exacerbated by an increase in marginal departures – the strongest in more than a decade – probably fuelled by improved opportunities for remote working. On the other hand, investment income has experienced a moderate upswing.

In terms of the trade in goods, the current account remains at a solid level, thanks in large part to the increase in pharmaceutical exports in the aftermath of the pandemic. However, the economic slowdown in key trading partners such as China and Germany poses a challenge and suggests a rather subdued trade balance in 2023. Looking ahead to 2024 and 2025, KOF expects the balance of trade in goods to continue its upward trend. In the services sector, however, a proportionate adjustment of growth in imports suggests a more moderate expansion. While the overall outlook remains stable, the current account surplus is therefore expected to see subdued growth.

The entire KOF economic forecast can be found here (in German):

Downloadhttps://ethz.ch/content/dam/ethz/special-interest/dual/kof-dam/documents/Medienmitteilungen/Prognosen/2023/VJA_2023_3_Herbst_Gesamtbericht.pdf (PDF, 2.1 MB)

Contact

KOF FB Konjunktur

Leonhardstrasse 21

8092

Zürich

Switzerland