Global economic outlook remains weak

Although the much-feared energy crisis has failed to materialise, persistently high inflation, rising interest rates and geopolitical conflicts are weighing on the global economy.

As expected, global output picked up slightly at the beginning of the year compared with the final quarter of 2022. The Chinese government’s abandonment of its zero-COVID policy, which has recently boosted the country’s economy, has contributed significantly to this trend. Both industry and the service sector have staged a strong recovery supported by the revival of private consumption.

Higher exports in various European countries and the United States as well as a stronger-than-expected increase in private consumption – supported by declining energy prices – have also boosted the economy. Overall, however, business activity in Europe was rather weak – especially in Germany, where the economy slipped into a technical recession in the first quarter of 2023 owing to a slump in government consumption and weak consumer spending after a second consecutive negative quarter. This is due, among other things, to the discontinuation of government-funded measures to combat the COVID-19 pandemic – such as vaccinations and testing – as well as the high prices of food, services and energy.

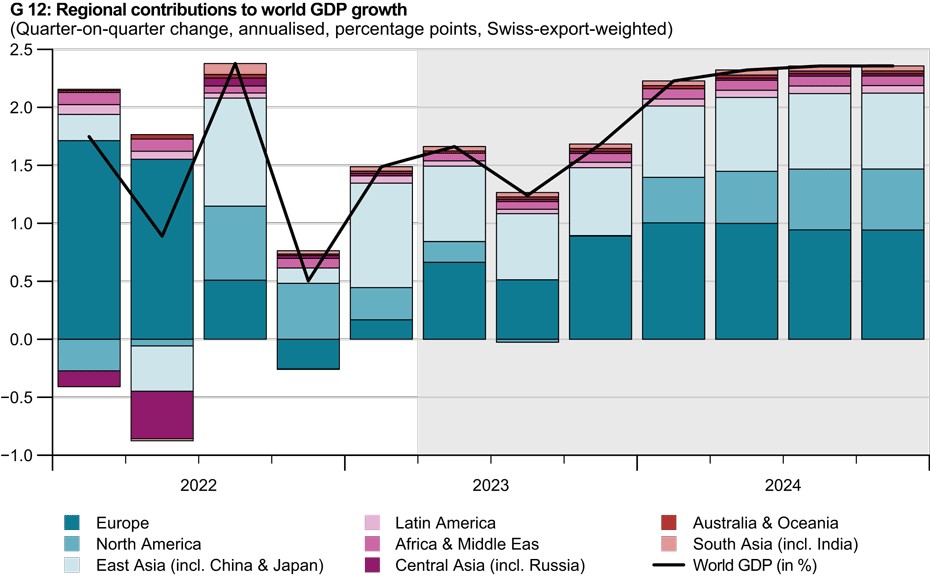

Global economic activity is likely to be weak in the second half of the year (see chart G 12). Declining but still high inflation and the more challenging financial environment are set to dampen private consumption, international trade and investment activity.

Easing energy prices causing further decline in inflation

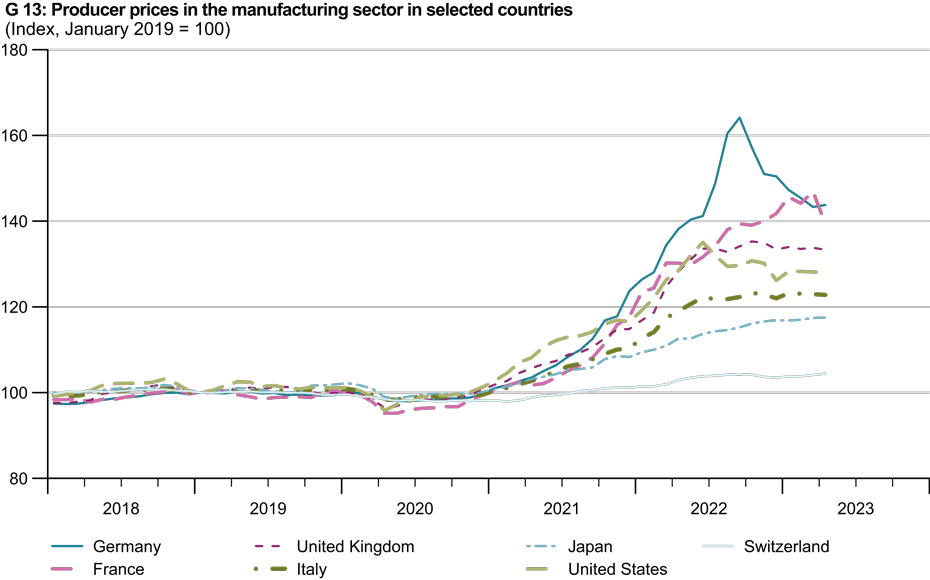

Producer prices in various countries have continued to fall or have stagnated in recent months (see chart G 13). This trend has been significantly influenced by the decline in energy prices since the beginning of the year as a result of last winter’s mild temperatures and the energy-saving measures taken by households and businesses. In addition, the lifting of COVID-related restrictions in China has had a positive impact on supply bottlenecks and reduced some prices of raw materials and intermediate products.

Consequently, consumer price inflation in the euro area fell significantly from 7 per cent in April to 6.1 per cent in May. This is its lowest rate since the outbreak of the war in Ukraine. Core inflation also fell slightly in the second quarter from 5.7 per cent in March to 5.3 per cent in May but remains well above the central bank’s target for price stability. This trend of falling inflation is not merely limited to the euro area and can also be seen in the United States and the United Kingdom, where consumer price inflation in April was 5 per cent and 8.7 per cent respectively.

Monetary policy tightening likely to slow further

As inflation remains high and is subsiding only gradually, the US Federal Reserve (Fed), the European Central Bank (ECB) and the Bank of England have continued to tighten monetary policy in recent months. Since March, the Fed has raised the target range for its federal funds rate in two stages of 25 basis points each to between 5 per cent and 5.25 per cent currently. However, there are signs of a slowdown in further restrictive monetary policy measures. For the first time following a series of ten interest-rate hikes in a row, the Federal Open Market Committee (FOMC) decided at its meeting on 14 June not to raise its key interest rate any further. This will enable the FOMC’s members to more precisely assess the effects of their monetary policy tightening so far. This could mean that interest rates have peaked for the time being, although further rate hikes in the second half of 2023 are not completely ruled out in the Fed’s statement on its latest interest-rate decision and are dependent on macroeconomic developments.

Given the recently heightened uncertainty in financial markets and the decline in the consumer prices of services excluding rents, food and energy, which the Fed recently used as its preferred inflation measure, KOF does not expect to see any further interest-rate hikes in the United States over the coming months. Because inflation remains well above the central bank’s targets, KOF does not expect key interest rates to be lowered during the further course of this year.

The ECB has raised its key interest rates in three stages of 25 basis points each since March. This means that its main refinancing rate is currently 4 per cent and has reached a level last seen prior to the outbreak of the financial crisis in 2007. The Bank of England has raised its key interest rate in several stages to 5 per cent. Despite the recent turmoil in financial markets, KOF expects to see further interest-rate hikes from the ECB and the Bank of England over the coming months. This is partly because uncertainty in the banking sector has recently decreased and central banks continue to fear that high inflation expectations will become entrenched.

Inflation likely to remain stubbornly persistent

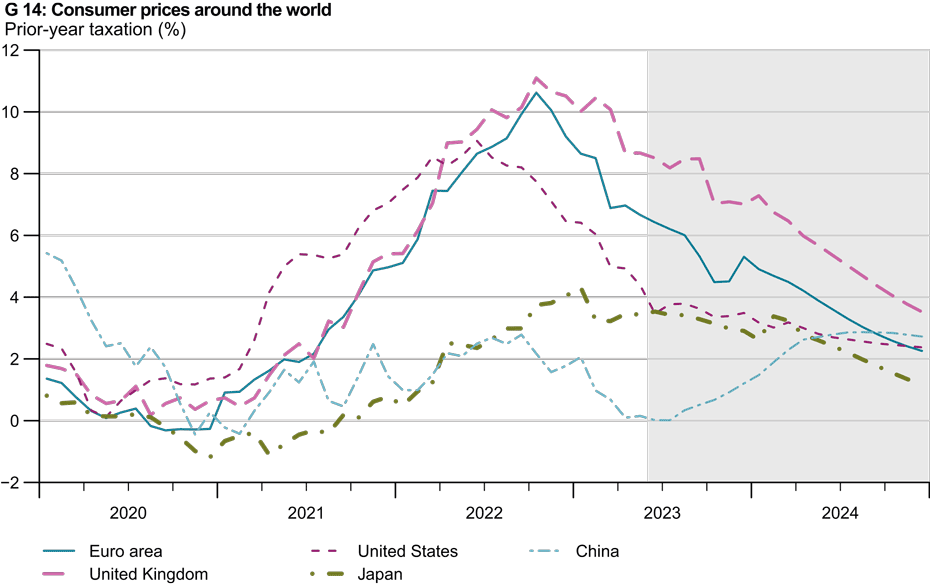

Given the fall in energy costs and the expiry of base effects from past price increases, inflation is likely to slow further in many countries over the coming months (see chart G 14). However, the extent of this decline in inflation could be less than central banks had hoped. This is due to the continued tight labour market, the shortage of skilled workers and strong wage increases in some countries, which keep the pressure on core inflation high.

Moreover, price rises in the services sector remain elevated owing to high demand in the wake of the post-pandemic recovery. Accordingly, inflation is likely to ease only slowly in many countries and should still remain above central banks’ targets over the forecasting period. KOF is forecasting annual inflation of 6.3 per cent for 2023 and 3.5 per cent for 2024 in the euro area, while annual inflation rates of 4.3 per cent for 2023 and 2.7 per cent for 2024 are expected in the United States.

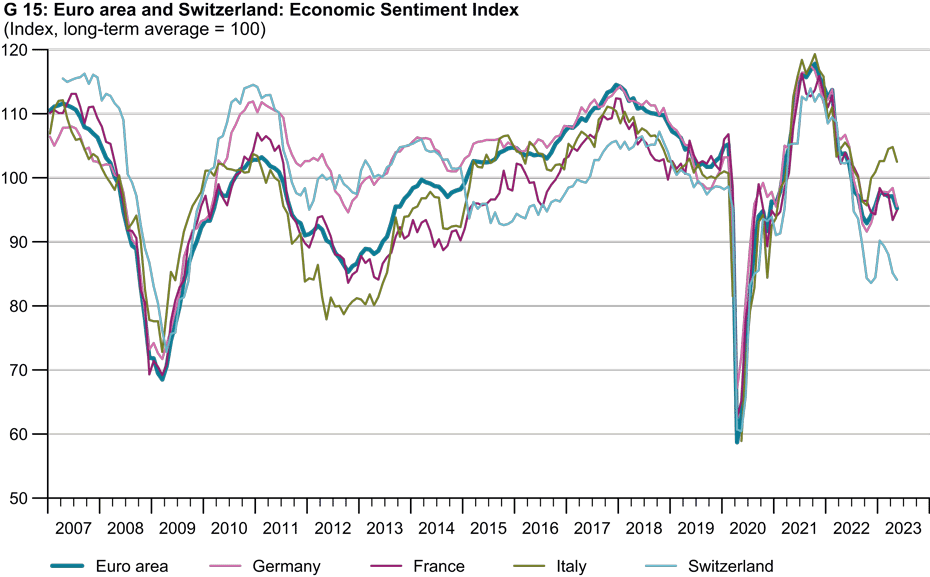

The encouraging trends in overall economic output at the beginning of the year are likely to continue in the current quarter before slowing significantly in the second half of the year. The strong growth in consumption in the United States in the first quarter is likely to be only temporary and will subside over the course of the year, as this was mainly due to one-off effects such as tax relief and the increase in social welfare benefits at the beginning of the year. Moreover, key leading indicators for all countries have recently deteriorated noticeably (see chart G 15).

In addition to the industrial and construction sectors, which have already seen weak investment over recent quarters and months owing to more challenging financing conditions, sentiment has also deteriorated in the retail and services sectors. Strong demand in the service sector in particular cannot be fully met as a result of persistent labour shortages, which are likely to lead to higher wage demands and rising prices.

Stubbornly high inflation in food and services is limiting consumers’ purchasing power and is likely to boost saving and thus dampen consumption. In addition, restrictive monetary policy will probably create tougher lending conditions for households and businesses and reduce investment activity.

On the other hand, countervailing positive stimulus should come from pent-up demand following the Chinese government’s abandonment of its zero-COVID policy, which should stimulate economic activity in China in 2023. Uncertainty about economic growth and the persistent crisis in the real-estate sector, which are likely to weigh on consumption, mean that pent-up demand in China is expected to be lower than in other countries. KOF is forecasting that Swiss-export-weighted world GDP will grow at a rate of 1.4 per cent this year and 2.0 per cent in 2024.

Various risks remain

KOF’s forecast assumes that the prices of oil and other energy sources will rise slightly over the forecasting horizon (by 1.5 per cent per year). The upside and downside risks to this forecast remain diverse owing to uncertainty around energy prices and the further course of the war in Ukraine. Downside risks include second-round effects from higher-than-expected wage demands, which would imply more persistent inflation than previously assumed. This would force central banks to adopt a more restrictive monetary policy, which would significantly increase the risk of an economic downturn.

In addition, a greater-than-expected negative effect of monetary tightening could exacerbate financing conditions for consumers and businesses and cause further distortions in financial markets. There is also the possibility of a further escalation of geopolitical tensions arising from the war in Ukraine. Moreover, global demand for natural gas could grow as a result of the economic recovery in China. This poses the risk that natural gas will only be available in Europe at considerable cost over the coming winter, which would have negative consequences for the economy.

Finally, it is unclear to what extent accumulated savings will be spent, especially in the United States. A highly uneven distribution of savings across the population could mean that individuals on lower incomes have already depleted their savings sooner than expected in KOF’s baseline forecast. Consequently, an earlier and more severe recession in the United States could increasingly drag down the economy in Europe as well.

Upside risks are that consumption grows more than expected on the back of a stronger reduction in savings and thus boosts the economy in the short term. In addition, it is possible that inflation will swiftly return to central banks’ target range. This would enable monetary policy to revert to a less restrictive stance at an earlier stage and therefore dampen investment activity to a lesser extent. It is also possible that current geopolitical conflicts could unexpectedly ease significantly, which would improve consumer and business sentiment.

Contacts

KOF FB Konjunktur

Leonhardstrasse 21

8092

Zürich

Switzerland

KOF FB Konjunktur

Leonhardstrasse 21

8092

Zürich

Switzerland

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland