Climate risks and investment: how Swiss companies are dealing with climate change

Although many Swiss firms see their business activities as being exposed to physical climate risks, they nevertheless view ecological change predominantly as an opportunity rather than a risk. Investment aimed at combatting climate change is accelerating and, in comparison with the EU, Switzerland is one of its pioneers. Having added a new block of questions to its investment survey, KOF can shed light on the economic impact of climate change from the perspective of Swiss companies.

Climate change poses epochal challenges to society as a whole and to businesses as part of it. Firstly, climate change confronts companies with uncontrollable events that can have a negative impact on their assets and productivity in both the short and long term. For example, extreme weather events such as floods can destroy entire production facilities and, in the longer term, higher temperatures can impair labour productivity. And, secondly, measures to mitigate climate change are subject to considerable uncertainty, while the transition to a post-fossil-fuel economy requires a high degree of flexibility and adaptability from companies.

Consequently, businesses face two types of climate-related risks: physical risks, which arise directly from climate change and the consequences of potentially related weather events, and transition risks, which arise from society’s response to climate change and the transition to a more sustainable economy.

New questions on climate-related and weather events included in the KOF Investment Survey

In order to grasp the economic impact of climate change and thus gain insights into its mitigation, a better understanding of these risks from a business perspective is necessary. To this end, KOF has supplemented the spring edition of its semi-annual investment survey with questions on how companies perceive climate risk and what measures they are taking to mitigate this risk.

These questions are based on the EIB1 Group’s investment survey , which polls around 12,000 firms from the 27 EU countries every year. Since 2020 this survey has included a block of questions on climate issues. Analysis of these questions makes it possible to compare the findings for Switzerland with international survey results. Thus, in the section below, the findings for Switzerland can be compared with the latest results of the EIB Investment Survey dating from 2022.

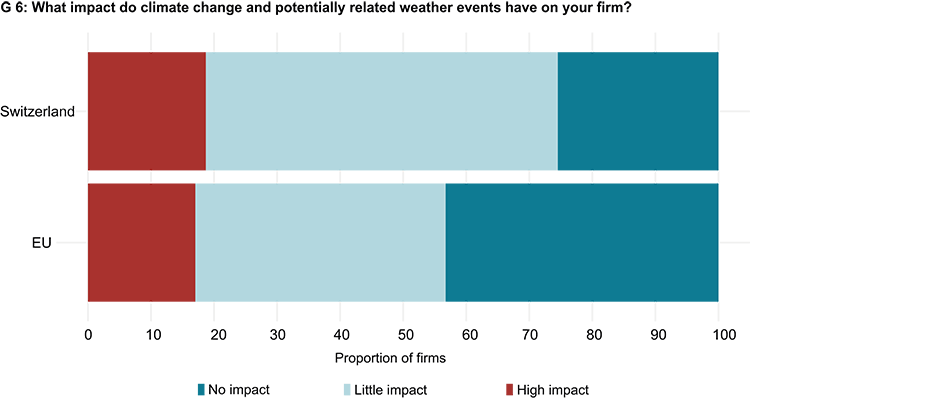

Physical climate risk represents a reality for many companies

Almost three-quarters of Swiss firms see themselves as being exposed to physical climate risk (see chart G 6). As part of the investment survey, companies were asked what impact climate-change-related weather events could potentially have on their business. Just under a fifth of respondents report a major impact and 54 per cent report a minor impact.

While more large companies see their business activities as being affected by physical risks than small and medium-sized firms do, there are hardly any differences in the perception of physical risks between individual sectors. When compared internationally, more companies from Switzerland regard themselves as being exposed to physical climate risk than firms from EU countries do. Overall, only 57 per cent of companies from EU member states consider their business activities to be affected by physical risks. 17 per cent report a major impact and two-fifths report a minor impact.

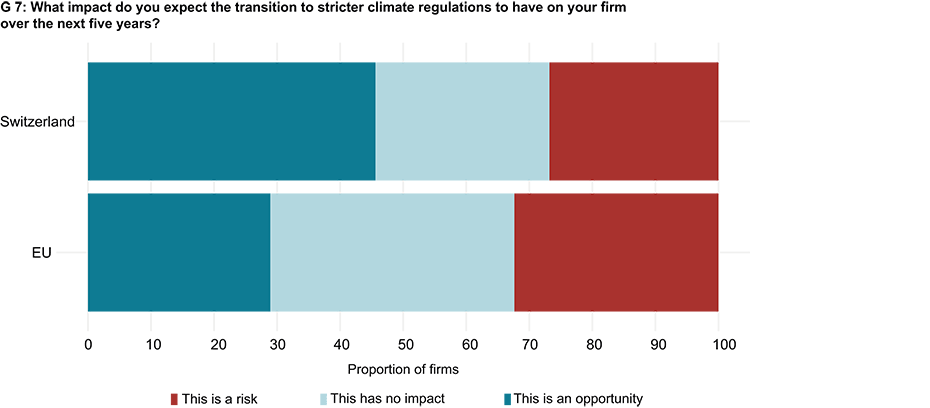

Companies view ecological change predominantly as an opportunity rather than a risk

The majority of Swiss firms seem to be aware of the risks associated with environmental change. When asked how the transition to stricter climate standards and regulations will affect their company over the next five years, almost half of these firms regard it as an opportunity and 27 per cent consider it to be a risk (see chart G 7). Around 28 per cent see no impact on their company. This means that more firms in Switzerland expect the ecological transition to have an impact than those in the EU do, while the change is viewed more optimistically here overall.

39 per cent of companies from the EU member states do not perceive any transition risk, 32 per cent consider the transition to be a risk and 29 per cent see it as an opportunity. Large companies and firms from the construction industry in particular regard ecological change as an opportunity. In contrast, the proportion of companies that see ecological change as a risk is highest in industry (one-third).

As transition risks can have various impacts on different business areas, firms were also asked to indicate the impact that the transition to low carbon will have on their market demand, supply chain and reputation over the next five years. This revealed that companies associate the environmental transition with positive rather than negative effects on their demand and reputation. However, this is not the case for supply chains, where firms tend to expect negative impacts.

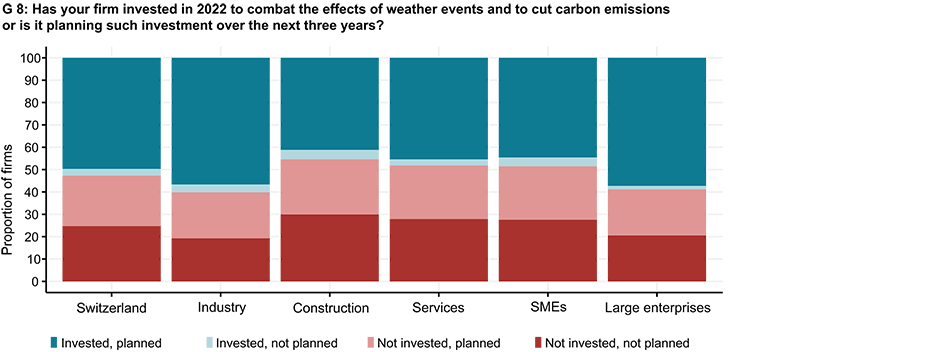

Swiss corporate investment to combat climate change is accelerating

More than half of Swiss companies invested to combat the effects of weather events and cut carbon emissions last year (see chart G 8). And investment aimed at combatting climate change is likely to gain further momentum in the near future. This is because almost three-quarters (72 per cent) of all firms are planning such investment in the next three years.

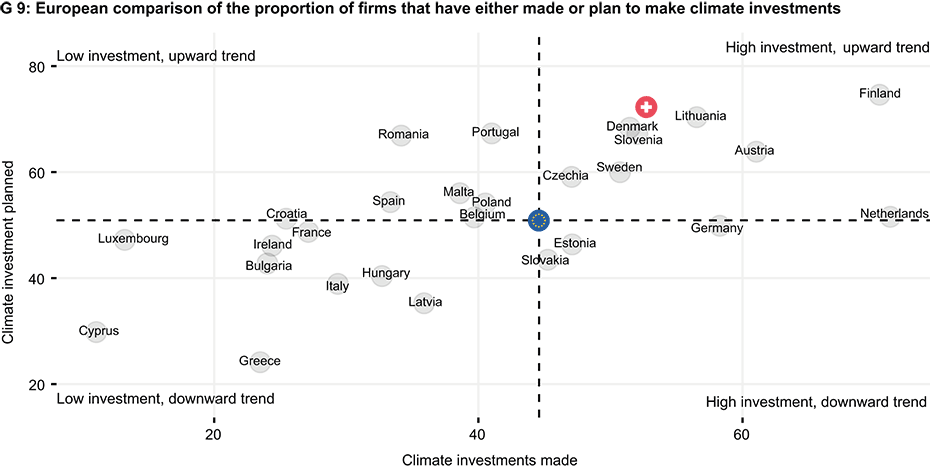

This gives Switzerland a pioneering role compared with EU countries. Fewer companies from the EU (an average of 45 per cent) have invested in cutting carbon emissions in the past than Swiss companies have. And fewer firms from the EU (51 per cent) are planning similar investment in the near future than companies from Switzerland are. This means that Switzerland is most comparable with countries such as Denmark, Slovenia and Lithuania in terms of its firms’ climate investment (see chart G 9).

One caveat to this comparison is that the latest available data from the EIB survey dates from 2022 and thus refers to marginally different time periods than the KOF Investment Survey data2 does (see the appendix on data and methodology for more details).

Climate investment in Switzerland is primarily made by large companies with more than 250 full-time-equivalent employees. 59 per cent of them have invested accordingly during the past year, while 78 per cent are planning further investment over the next three years. In contrast, only 49 per cent of SMEs have already made climate investments, while two-thirds of them plan to do so in the near future. Viewed across various sectors, 60 per cent of manufacturing companies are investing in cutting their carbon emissions, while the corresponding proportion among construction firms and service providers is less than half.

------------------------

1The EIB Group consists of the European Investment Bank and the European Investment Fund.

2The KOF Investment Survey data is from spring 2023; previous investment by companies in Switzerland refers to the year 2022, while investment planned for the near future relates to the next three years (2024 to 2026). EIB Group Investment Survey data is from 2022; previous investment by companies from EU member states refers to 2021, while investment planned for the near future relates to the next three years (2023 to 2025).

Data and methodology

KOF Investment Survey

The Investment Survey conducted by the KOF Swiss Economic Institute at ETH Zurich serves as a timely record of Swiss companies’ investment activity. It has been carried out since 1967 and contains questions on investment plans and objectives, investment purposes and factors influencing investment.

The participants are private Swiss firms with more than two full-time-equivalent employees covering all sectors of the Swiss economy except agriculture. The panel of respondents is a stratified random sample, which ensures that it constitutes a representative sample of the Swiss economy for each enterprise size class (measured by the number of employees) at the industry level (NACE ‘division’ level).

The investment survey is conducted semi-annually in the spring and autumn of each year. Firms may complete the survey in either German, French, Italian or English, and the questionnaire may be completed either on paper or online.

The spring 2023 survey was conducted between 21 February and 15 May 2023. A total of 5,858 firms were contacted, of which 2,488 responded. The corresponding response rate is 43 per cent.

EIB Group Investment Survey

The EIB Group Investment Survey is designed to capture European firms’ investment activity and financing. Since 2020 it has included a block of questions on climate.

Participants are drawn from Bureau van Dijk’s Orbis database. The sample includes non-financial enterprises (NACE level of sections C to J) with at least five employees from the 27 EU member states. Since 2019 the survey has also been conducted in the United States. The panel of respondents is a stratified random sample and representative at the EU, country, sector and enterprise size class levels.

The survey has been conducted annually by telephone since 2016. Additional modules are partly completed online. The 2022 survey was conducted during the period from April to July 2022. Around 12,000 firms from Europe and 800 firms from the United States were surveyed.

Comparability of KOF and EIB data

The KOF Investment Survey data was collected in spring 2023. The EIB Group Investment Survey data is from 2022 and is publicly available: external pagehttps://data.eib.org/eibis/.

The questions in both surveys are comparable in terms of wording. The reference times and reference full stops used in the questions are identical in that the realisations refer to the past year, while expectations relate to the next three or five years.

The samples used in the two surveys essentially differ in their sectoral coverage (KOF surveys firms from NACE sections C to S, while the EIB Group surveys them from NACE sections C to J), in their inclusion of small firms (the EIB Group surveys firms with more than five employees, while KOF also surveys micro-enterprises with between two and five employees) and in the granularity of their stratification (KOF stratifies its sample per three enterprise size classes and 75 NACE sections, while the EIB Group stratifies its sample for each country per four enterprise size classes and four sectors).

The EIB Group weights its survey results using data on value added at factor cost (gross income from operating activities after adjusting for operating subsidies and indirect taxes) as the population. Each enterprise is given the same weighting within a size class-sector stratum. The KOF Investment Survey’s results are weighted according to employment.

Contact

KOF FB Konjunkturumfragen

Leonhardstrasse 21

8092

Zürich

Switzerland