KOF Business Tendency Surveys: Swiss economy faltering

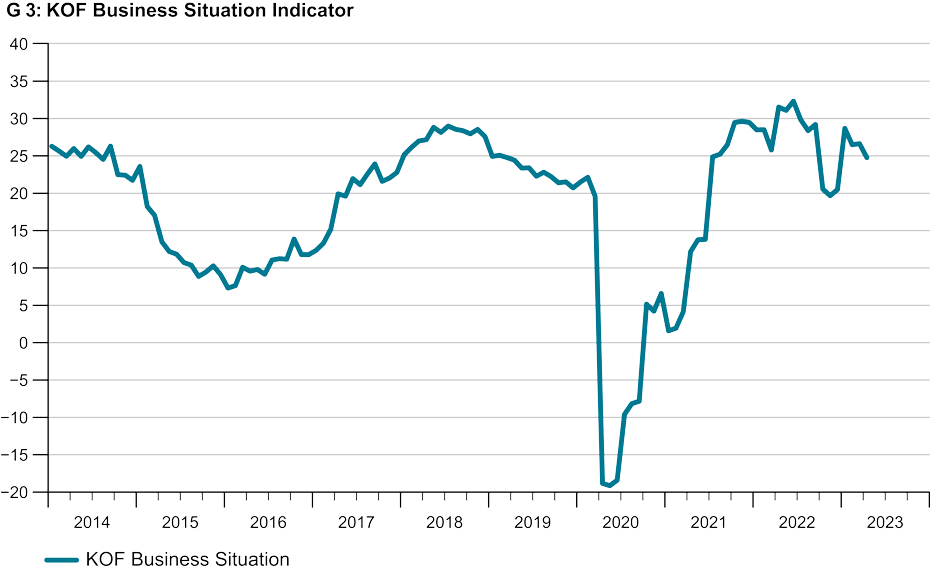

The KOF Business Situation Indicator for the Swiss private sector, which is calculated from the KOF Business Tendency Surveys, fell in April after barely moving in the previous month (see G 3). Business is thus still performing better than it did in the autumn of last year but is no longer as buoyant as it was in January.

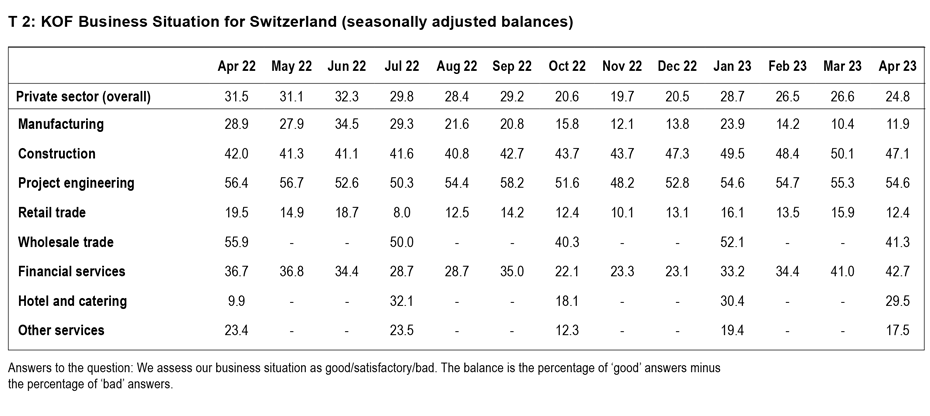

The performance of individual sectors varied in April. Manufacturing industry managed to stop its downward trend of recent months for the time being. The construction, retail and other services sectors suffered setbacks. The downturn in the wholesale trade was somewhat more pronounced (see table T 2).

Supply chains are working again

There are indications that the problem of shortages of materials and inputs is becoming much less acute across several sectors. Complaints about a lack of materials and intermediate products in the construction industry and the manufacturing sector are declining sharply. Wholesalers expect delivery times to decrease. Companies in the manufacturing sector are reporting that, in their view, the stocks of intermediate products in their warehouses are clearly too high. After a phase in which inventories were deliberately built up, a period could now follow in which target inventories of primary products are adjusted downwards again.

Price buoyancy declining sharply

Price increases are clearly declining in line with firms’ projections. Price rises have peaked in all surveyed sectors for the time being. Although price increases are still being planned most frequently in the hospitality industry, even here the upward trend is no longer as strong as it was in previous quarters. The main reason for the declining upward trend in sales prices is probably that the purchase prices of companies’ intermediate products are no longer rising as sharply. Supply chains are functioning again and energy prices – for example for gas – are easing. Firms’ expectations about general consumer price inflation match these projections regarding their own sales prices. In April they expected inflation to reach 2.6 per cent over the next twelve months. In January they were still forecasting 2.9 per cent inflation and in October 2022 3.7 per cent inflation in each of the following twelve months.

Labour shortages continue to be a concern for companies

The shortage of workers continues to affect firms considerably. Although complaints about staff shortages no longer increased in all sectors of the economy in April, none of these industries is out of the woods yet. Reports of labour market shortages are currently relatively widespread in all sectors over the medium term.

Not enough new orders being received in the manufacturing sector

The Business Situation Indicator for manufacturing managed to avoid a third consecutive decline, rising slightly in April. Nevertheless, business in manufacturing is currently less buoyant than it was throughout 2022. Companies’ orders on hand decreased, although production was not expanded on balance. Capacity utilisation remained unchanged compared with the previous quarter. Consequently, stocks of finished goods were replenished more slowly than in the previous month, but inventories are still reckoned to be much too high. Assessments of input-product inventories are even more striking. After these inventories were considered to be far too low at the turn of 2021/22 and companies had frequently complained about shortages of intermediate products, they now think that their inventories of inputs are much too large. Firms now even see their business activities being constrained more often by a lack of demand than by a shortage of intermediate products.

Capacity utilisation is high in the construction-related sectors of the economy

Business in the sectors associated with building activity – project engineering and construction – was slightly restrained in April. However, the situation remains buoyant. Earnings have improved more frequently than before and companies in both sectors are more confident about their earnings going forward than they were previously. In the construction sector, however, demand has recently not risen as sharply as it did before and satisfaction with order books has declined. Although capacity utilisation in the construction sector remains very high, it is no longer peaking as it did in the previous quarter. Firms are evidently feeling a marked reduction in cost pressures because, on balance, they are no longer looking to raise their prices.

Business activity in the wholesale and retail sectors has been restrained

Business in the retail trade deteriorated slightly in April after having improved in the previous month. Sales of goods remain under slight downward pressure, as in previous months, although customer footfall in shops is higher than it was a year ago. Retailers are now looking to raise their prices less frequently than they were at the beginning of the year. Nevertheless, they expect demand to perform better and sales to increase in the near future. After improving in January, the Business Situation Indicator for wholesalers in April fell back almost to where it had been last autumn.

The hospitality industry continues to perform well

Business in the hospitality industry was almost consistently good in April. Forecasts for the coming six months are still very positive despite a slight slowdown. Uncertainty about business going forward has also decreased. Revenue was increased sharply compared with the corresponding quarter of last year. Room occupancy in hotels rose again. Plenty of room reservations were received for the current quarter, primarily in the major towns and cities. Overall, earnings in the hospitality industry again performed rather well. Nevertheless, further price rises are planned, although not quite as widespread as they were in the autumn.

Other service providers report high levels of capacity utilisation

The recovery in other services did not continue, and the Business Situation Indicator fell slightly in April. The fact that survey respondents’ expectations about the level of business going forward are slightly more optimistic than before suggests that there will be no general downward trend reversal. Companies’ capacity utilisation is now significantly higher than it was before the pandemic. The transport sector, which recovered only very slowly from the pandemic, is now reporting a capacity utilisation rate slightly above the average for 2018 and 2019. As firms are still planning to increase their staffing levels almost as before, labour shortages continue to be a major issue in this sector of the economy. However, complaints about these have declined slightly compared with the previous quarter.

Contact

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland