The Swiss construction sector since COVID-19: an interim assessment

There is currently much discussion about developments in the local real-estate and rental housing markets. This article adds to the debate by classifying the Swiss construction sector during the current period of upheaval.

Although the COVID-19 pandemic initially caused disruption in the Swiss construction sector in spring 2020, the industry quickly found its feet again and held up very well compared with other sectors of the economy. Because there were only a few large-scale construction site closures at the beginning of the pandemic, work in the construction sector only ground to a halt in certain areas across Switzerland. On the other hand, the crisis also had fairly stimulating side-effects on the sector – for example, on demand in the real-estate and mortgage markets. The adjustments to lifestyles during the COVID-19 pandemic boosted demand for home improvements, more living space and, especially, spending more time at home. The latter factor is now driving up property prices in Switzerland owing to the shortage of residential property available.

Indicators of a dynamic construction industry

Brisk momentum has been noticeable on many fronts in the construction industry over the past three years. Several indicators of construction activity from the KOF Business Tendency Surveys have been performing encouragingly well since the short-lived, crisis-related slump in spring 2020. Regular reports issued by the construction companies show that the majority rate their business situation and order backlogs as being satisfactory or good – and this assessment is much more unanimous than it was before the crisis.

As many economic indicators have been on a continuous upward trajectory since spring 2020, they are now already well above their pre-crisis levels. This trend can also be observed in construction sector employment. At the same time, reports from survey respondents and other voices within the industry are increasingly agreed that they are reaching their capacity limits in certain places. Following a surge in global demand, worldwide supply delays and shortages of inputs and building materials pushed firms to their production limits in 2021. Meanwhile, worsening staff shortages are one of the main factors constraining construction companies’ performance.

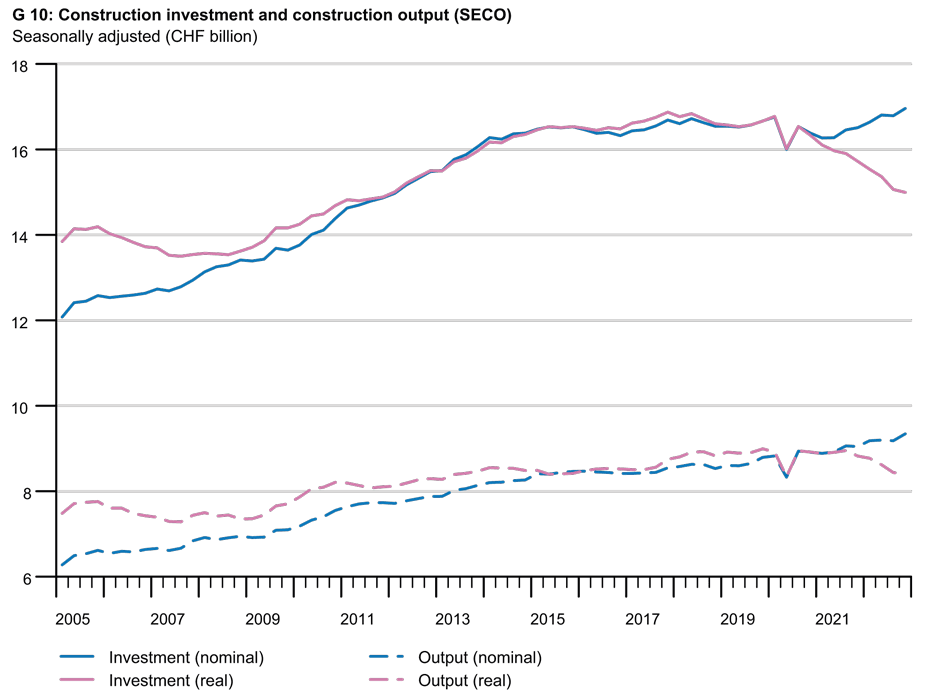

Construction investment and construction output since the COVID-19 shock

These observations are contrasted with data showing the amount produced (output side) and investment (GDP calculation) in the Swiss construction sector. They are collected by the Swiss Federal Statistical Office (FSO) and published annually for the previous year in each case. The State Secretariat for Economic Affairs (SECO) publishes the levels of construction output and construction investment over the four quarters of a year (chart G 10) based on the FSO’s annual figures.

Since it bounced back from the initial COVID-19 shock in the second quarter of 2020, the construction sector has performed much worse than the previously mentioned indicators imply (according to the latest figures). The nominal data show a modest but, at least, slightly positive trend in construction investment and construction output over the past three years. However, if we look at the real values – i.e. investment activity and output minus the additional effect that construction services have become significantly more expensive during this period – there has effectively been less investment and output for several quarters.

Current inflation presents a mixed picture

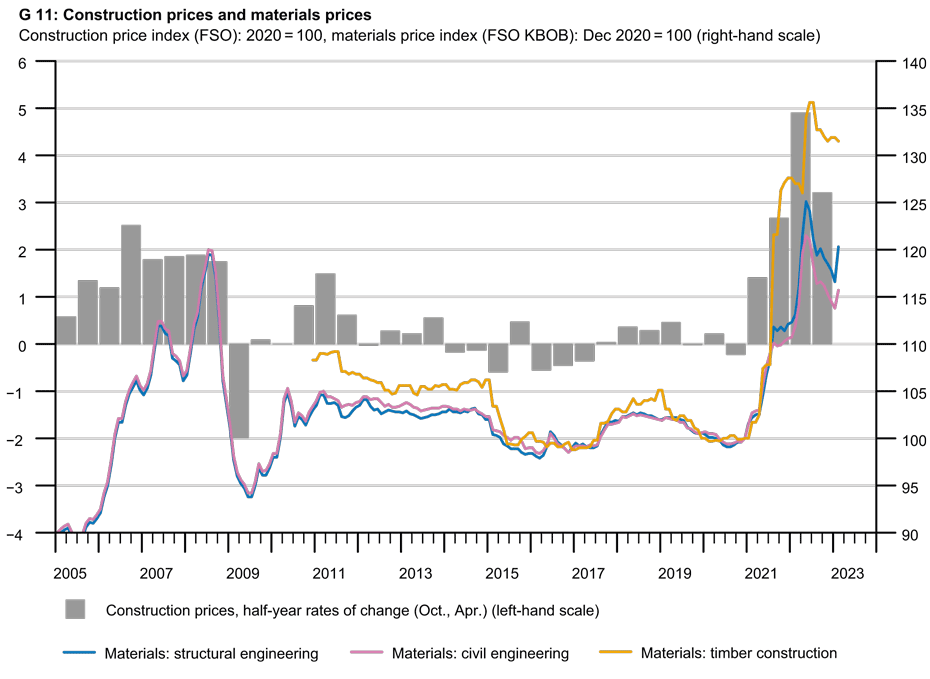

The emerging discrepancy between nominal and real trends thus conceals the fact that, in the midst of the pandemic-related turbulence, Swiss construction prices were subject to a level of disruption that is now turning out to be more drastic than was initially suspected. The surging global prices of preliminary products, raw materials and building materials such as steel, plastics and wood that emerged during the crisis led to a significant increase in the price of construction services in Switzerland from mid-2021 onwards (chart G 11).

By October 2022 the construction prices recorded by the FSO Construction Price Index had risen by 3.2 per cent within six months and by as much as 8.3 per cent compared with prices in October 2021. This is the highest inflation rate recorded by this index since the time series began back in 1998. The long period of enormous pressure on margins and, consequently, low or even declining prices in the Swiss construction sector (2009 to 2020) has therefore ended for the time being.

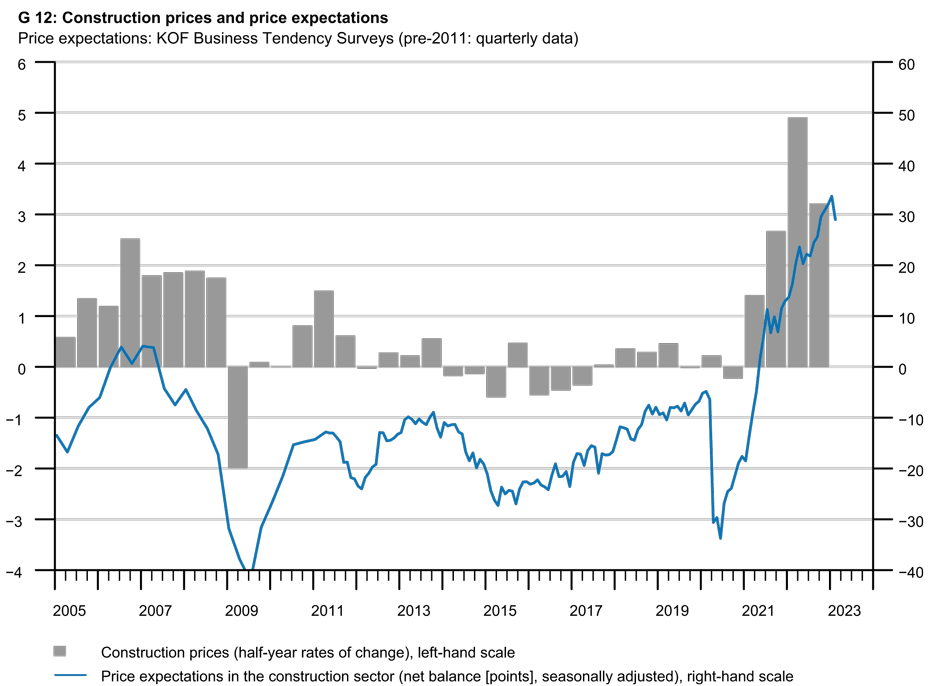

Although price inflation in raw materials and construction materials has been gradually returning to normal since mid-2022, construction prices will continue to rise for the time being. This is because the greater demand for construction services coupled with labour shortages is likely to widen the scope for construction companies to raise their prices owing to their high capacity utilisation. A good indicator of expected price levels over time is the price projections of construction firms revealed by the results of the KOF Business Tendency Surveys. This indicator has been rising so steeply and continuously since spring 2020 that it hits a new all-time high almost every reporting month (chart G 12). In February of this year, 32 per cent of construction companies expected to raise their prices over the coming three months while 64 per cent expected prices to remain at their current levels for the time being.

A long build-up

The fact that nominal and real rates of change in the construction sector are no longer aligned is thus a phenomenon that has been somewhat forgotten but is not new. As the global economy boomed between 2000 and 2008, high global demand led, among other things, to sharp price increases in raw materials such as metals and chemical substances. This also caused construction prices in Switzerland to rise continuously between 2005 and 2008 (see chart G 11). At that time, too, the real output and investment data were declining while the nominal data suggested a positive trend. Following this weak phase, the world recession of 2007/2008 surprisingly hardly impaired the Swiss construction sector. On the contrary, driven by fundamental factors such as strong immigration and fuelled by low interest rates, a long-lasting construction boom began in Switzerland in 2008 and peaked between 2018 and 2019.

Construction investment has declined again since then, although this should rather be seen as a normalisation from a very high level. KOF reckons that the cooling of activity in the construction sector, which had already become apparent previously, has not been exacerbated by the pandemic and that no construction recession is imminent either. Factors such as high population growth, the prevailing housing shortage, benign labour market conditions and the resilient Swiss economy support this view. KOF’s assessment is that we are likely to see a “soft market landing”1 at the bottom followed by a revival of momentum in construction activity.

----------

1 In a study entitled 20 Jahre Wohneigentumsboom: Wie weiter? (Raiffeisen, 2016) Raiffeisen Bank describes its forecast as a “soft market landing”, referring to the Swiss real-estate and construction markets.

References

Raiffeisen (2016): 20 Jahre Wohneigentumsboom: Wie weiter?

external pagehttps://www.raiffeisen.ch/content/dam/www/rch/ueber-uns/news/de/Immobilienstudie-de.pdf

German Commodity Agency (DERA) (2013). Causes of Price Peaks, Slumps and Trends in Mineral Commodities.

external pagehttps://www.deutsche-rohstoffagentur.de/DE/Gemeinsames/Produkte/Downloads/DERA_Rohstoffinformationen/rohstoffinformationen-17.pdf?__blob=publicationFile

Contact

KOF FB Konjunkturumfragen

Leonhardstrasse 21

8092

Zürich

Switzerland