Swiss labour market remains in good shape

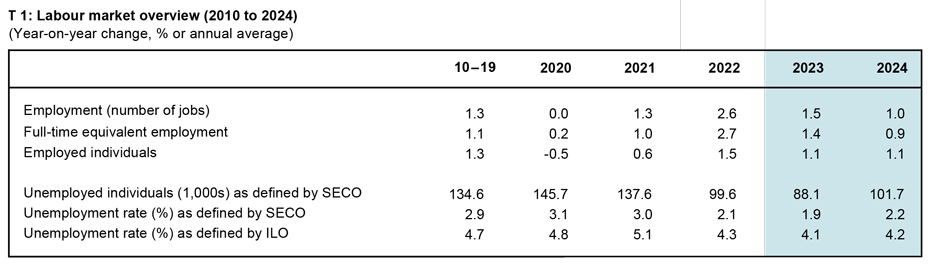

2022 will go down in history as an exceptional year for labour markets in Switzerland and many other European countries. KOF is forecasting that employment will increase by 1.5 per cent this year and 1 per cent next year.

Last year was one of the Swiss labour market’s best in recent decades. Almost all key labour market indicators reported values either close to or above their historical highs (such as the number of workers, the extent of firms’ recruitment problems and the number of vacancies) and lows (unemployment). The latest labour market figures indicate that the upward trend in the Swiss labour market continued in the fourth quarter of 2022. The number of registered unemployed fell by a seasonally adjusted total of 6,600 during the months between the end of September and the end of December, according to figures from Switzerland’s State Secretariat for Economic Affairs (SECO).

The high number of unemployment insurance (ALV) payments also played a role here. About 4,000 additional ALV claimants who had their ALV claim periods extended for a few months during the COVID-19 pandemic were taken off the payroll in November. Even if this one-off effect is excluded, however, the rate of registered unemployment decreased quite significantly in each of the last three months of 2022. According to the latest figures, this trend continued in January and February 2023, while employment statistics reveal that it strengthened between the end of September and the end of December 2022.

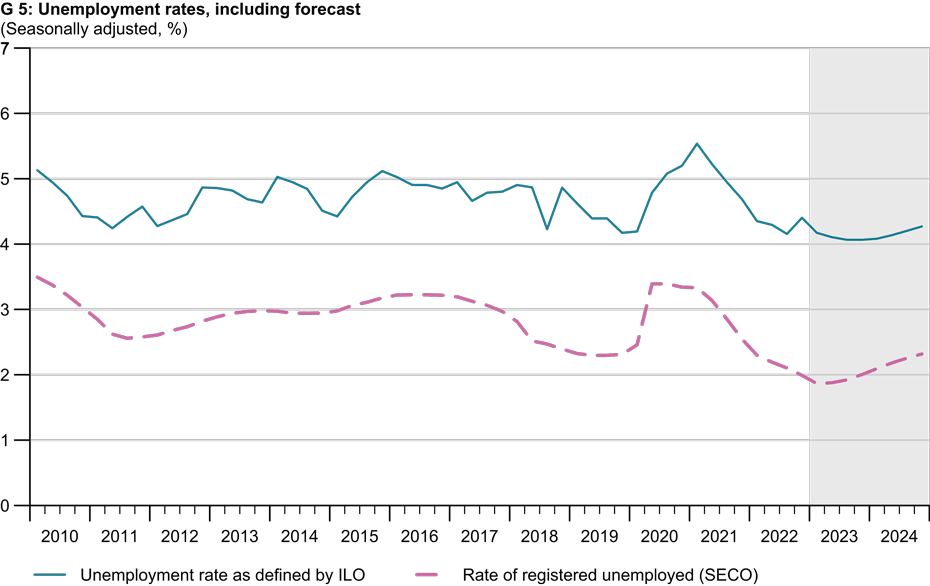

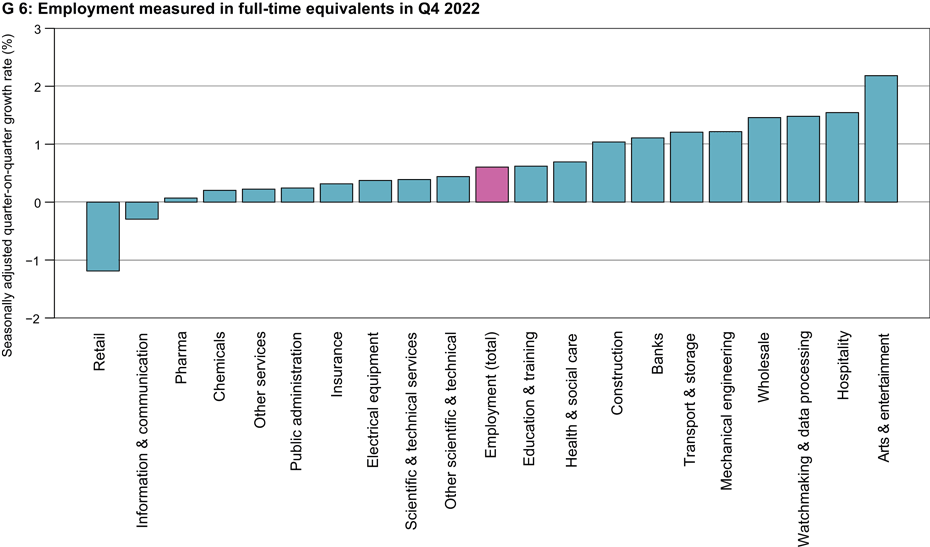

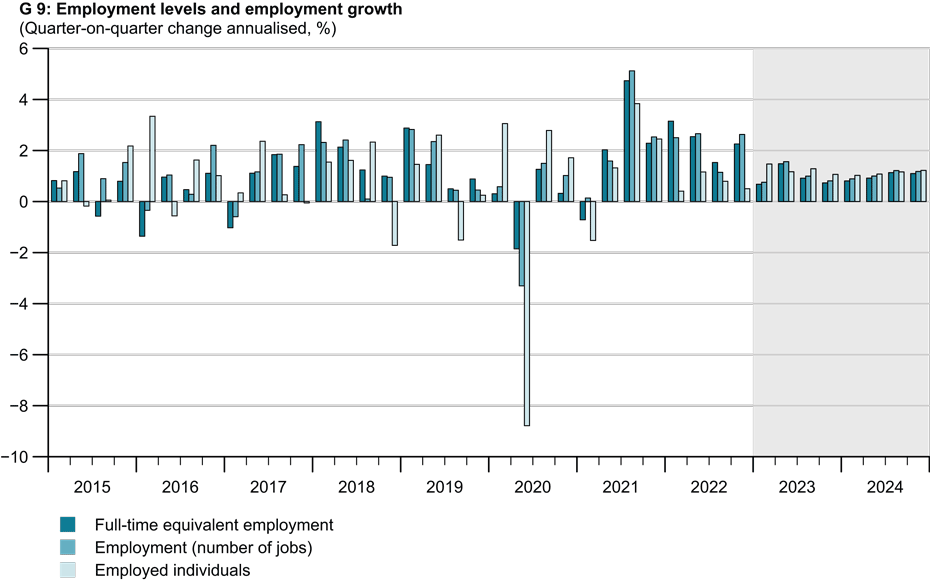

Measured in terms of full-time equivalents (FTEs), a seasonally adjusted increase of 0.6 per cent was reported. This growth was around 0.3 percentage points higher than expected by KOF in its December forecast. Only the unemployment rate as defined by the International Labour Organization (ILO) – unexpectedly and somewhat inconsistently with the other labour market data – showed a slight increase in its seasonally adjusted figures in the fourth quarter of 2022.

The data from the employment statistics show that employment growth was broadly based across sectors at the end of 2022. The strongest growth rates in FTEs in the fourth quarter were recorded in the hospitality industry (seasonally adjusted 1.5 per cent) and the arts and entertainment sector (2.2 per cent). These are the sectors that were most seriously affected by the COVID-19 pandemic. The watchmaking industry and data processing (1.5 per cent), the wholesale trade (1.5 per cent) and mechanical engineering (1.2 per cent) also grew strongly. Only two industries reported slightly declining employment figures. While the decrease in the information and communication sector was modest at 0.3 per cent, there was a significant fall of 1.2 per cent in the retail sector.

European labour markets booming

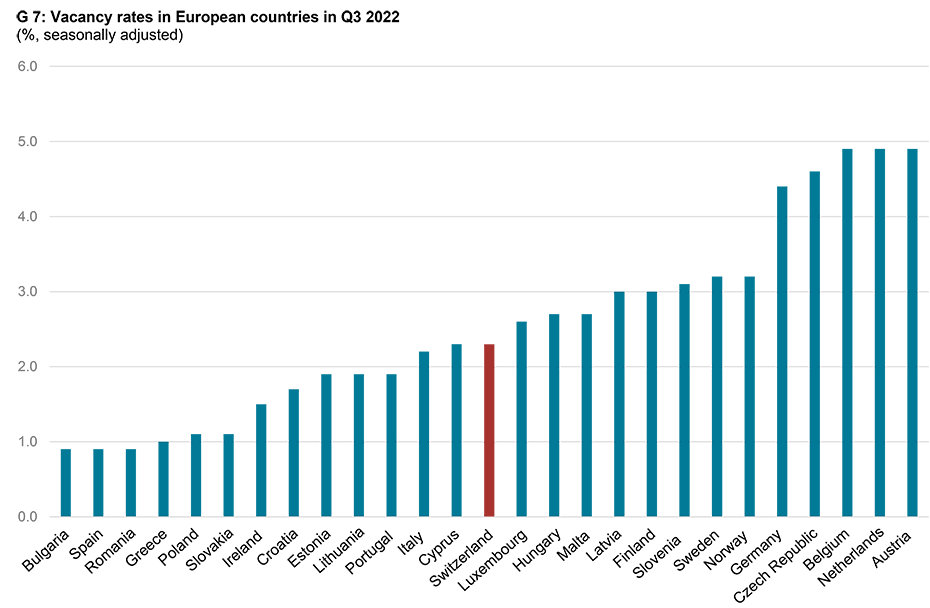

Switzerland was not the only European country whose labour market was in excellent shape in 2022. Despite fears of recession and high inflation rates, labour markets were booming in virtually all EU countries, as the figures on vacancy rates – the number of job vacancies in an economy as a percentage of the total number of jobs – show. Seasonally adjusted, 2.9 per cent of all jobs in the EU and 3.1 per cent of jobs in the euro area were unfilled in the third quarter of 2022. Even more impressively, vacancy rates rose to a new historic high in one of the last four data quarters in 17 of the 27 countries for which the European statistics portal Eurostat publishes this rate.

Looking at the situation in individual countries, seasonally adjusted vacancy rates were highest in the Netherlands, Belgium and Austria at 4.9 per cent each. Switzerland, with a seasonally adjusted rate of 2.3 per cent – also a new historic high – ‘only’ ranked 14th out of the 27 countries for which data are available (see the chart G7 entitled ‘Vacancy rates in European countries in Q3 2022’).

Given the high numbers of jobs that companies are looking to fill, unemployment in the EU and the euro area fell sharply. The unemployment rate as defined by the ILO, for example, adjusted for seasonal effects, was still 6.6 per cent in the euro area, which was 0.4 percentage points lower than in December 2021 and lower than at any time since the introduction of the euro. As a result of these developments, the Europe-wide Beveridge curve, which compares the unemployment rate with the vacancy rate, was at the upper-right edge at the end of 2022. This is a clear indication of a boom in the European labour market.

Shortage of skilled workers remains acute in 2023

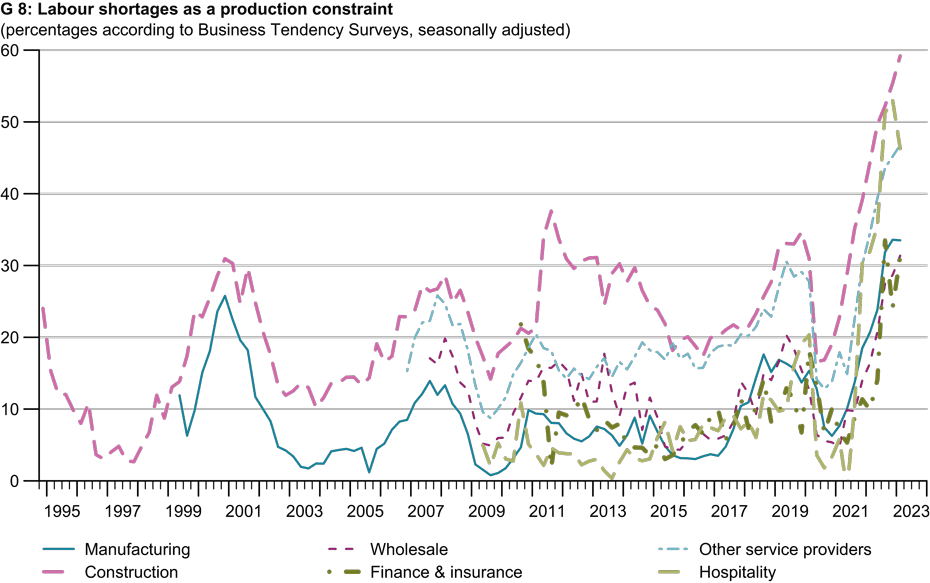

Given the sharp rise in employment in almost all sectors at home and abroad, it is not surprising that companies in Switzerland found it increasingly difficult to fill their large numbers of job vacancies with suitable staff last year. Accordingly, there were acute labour shortages in Switzerland and across large parts of Europe. Firms sometimes had trouble finding staff even for more basic jobs. Figures from the KOF Business Tendency Surveys for January 2023 suggest that the shortage of skilled labour continued to be a major stumbling block for companies at the beginning of 2023. The proportion of firms that reported being hampered by a lack of staff in their production and service provision functions remained at a historically high level.

These data reveal that the shortage of skilled workers in the construction industry actually increased. Almost 60 per cent of all firms here complained of staff shortages – the highest value of all sector aggregates shown. As the chart G8 entitled ‘Labour shortages as a production constraint’ shows, the construction industry had already been hit particularly hard by staff shortages in the past. This finding, which is surprising at first glance, is confirmed by a recently published study that KOF conducted together with a private-sector partner. Using extremely granular data obtained from all online job advertisements in Switzerland, the study commissioned by the Swiss Employers’ Association investigated which jobs in Switzerland are difficult to fill. The vacancy duration – the period of time between the posting and deletion of a job advertisement – was used as a measure of the difficulty of filling a vacancy.

This study’s evaluation according to detailed occupations shows, among other things, that the average vacancy duration is indeed relatively high in occupations that are generally said to have a great shortage of skilled workers such as doctors, nursing specialists, civil engineers and software developers. However, this duration is even higher in technical professions that require federal qualifications and are strongly represented in the construction industry. For example, it is extremely difficult to find female heating engineers, plumbers and carpenters in Switzerland.

Baby-boomer generation gradually leaving the labour market as demand for workers increases

In addition to the booming labour market, demographics have probably also contributed to the current shortage of skilled workers. The gradual retirement of the baby-boomer generation is increasing the need for replacements. The demographic effect on the demand for skilled workers is likely to intensify over the next five years compared with today before it becomes less important again. We can reach this conclusion by correlating the data on the age structure of the Swiss population with the labour force participation rate by detailed year of age, using realised and projected population figures.

If we assume, for the sake of simplicity, that the labour force participation rate in each age year will remain constant at the most recently observed level over the next few years, we find that, based on the age structure alone, at least 14,000 more people in the labour force will have to be replaced in 2023 than in 2015. In 2028, just as the retirement wave is calculated to peak, there will be at least 20,000 more people in the labour force than there were in 2015. The demographic pension peak is shifted slightly backwards in time if we assume, for example, that the increase in women’s retirement age will slightly raise the labour force participation rate in old age over the next few years. Based on these calculations, KOF has long assumed in its population scenarios, which are included in this forecast, that rising replacement demand over the coming years will also increase net immigration.

Better labour market outlook than in the previous forecast

Switzerland’s labour market continued to be in good shape at the beginning of 2023. Many leading labour market indicators – such as the Swiss Job Tracker, which tracks the fortunes of all jobs advertised online in Switzerland – showed signs of normalisation but remained at highly encouraging levels. The robust indicator situation is one reason why KOF assesses the outlook for the Swiss labour market more positively in its spring forecast than in its two previous forecasts. The second reason is that, according to its latest forecast, major neighbouring countries are likely to avoid the recession that had been expected until recently.

In concrete terms this means that KOF’s latest forecast predicts that employment will increase in the first half of 2023 rather than stagnating. However, even the latest forecast expects growth to slow compared with the very strong growth achieved in 2021 and 2022. KOF is now forecasting that employment will increase by an average of 1.5 per cent in 2023 (previous forecast: 1 per cent) – partly as a result of the considerable overhang. Annual growth is likely to be 1.4 per cent in FTE terms. KOF expects to see growth of around 1 per cent in both figures next year. The number of individuals in employment will rise in parallel (by 1.1 per cent in both 2023 and 2024).

According to the forecast, the decline in unemployment will continue in the first quarter of 2023 but will come to a halt thereafter. Overall, KOF is forecasting an average registered unemployment rate of 1.9 per cent for 2023 (as defined by SECO) compared with 2.2 per cent in its previous forecast. This rate will rise slightly to 2.2 per cent in 2024. The unemployment rate as defined by the ILO will rise in parallel at a higher level, averaging at least 4.1 per cent in 2023 according to the forecast. It is presumed that the aforementioned seasonally adjusted increase in the unemployment rate in the fourth quarter of 2022 was due not only to cyclical factors but partly also to the statistical imprecision of this indicator. KOF therefore assumes a certain counter-correction in the ILO figures in the forecast for the first quarter of 2023.

Contact

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland