KOF Business Tendency Surveys: threat of recession this winter is fading

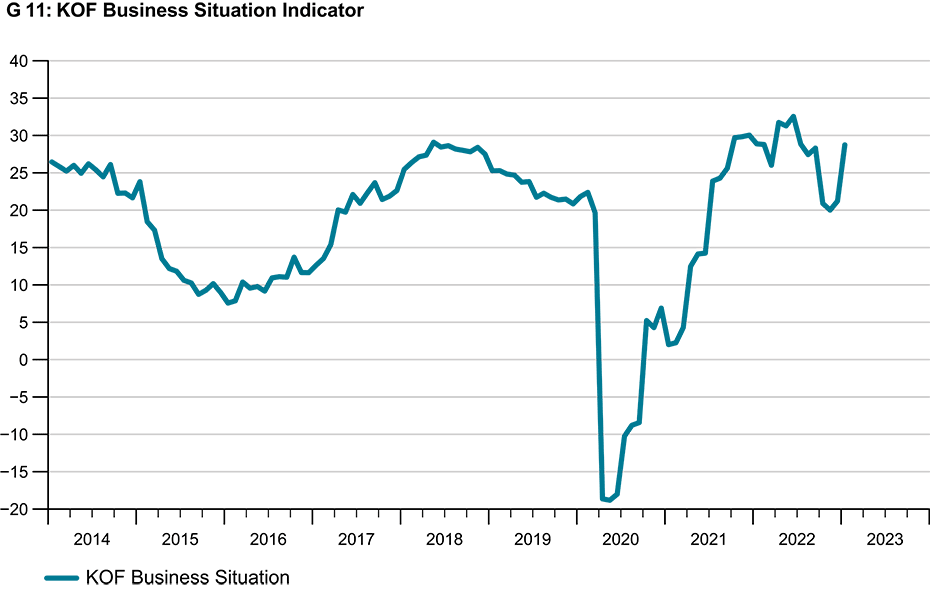

The KOF Business Situation Indicator for the Swiss private sector, which is calculated from the KOF Business Tendency Surveys, rose significantly in January (see chart G11). While firms’ business had deteriorated in the autumn, a clearly positive trend was visible in January. The operating outlook for the coming months is more encouraging than it was before.

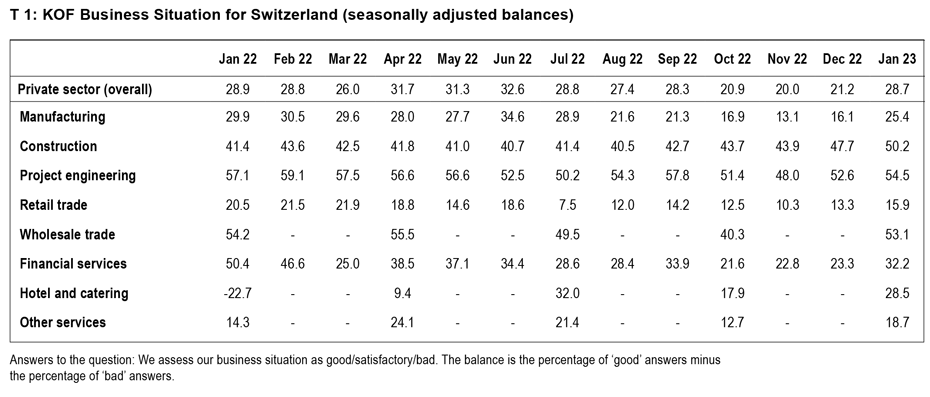

The business situation improved across the board – in some cases substantially – in January. Compared with the previous survey this improvement was particularly pronounced in the wholesale trade, hospitality, manufacturing and financial and insurance services. This positive trend is not quite as strong – albeit still clearly evident – in other services, the retail trade, construction and project engineering. The business outlook for the near future is similarly widespread. Only the construction industry is not following suit. Otherwise, confidence is growing in all sectors (see table T 1).

Price buoyancy declining slightly

Swiss companies’ plans to raise their prices are still strong, even though their intentions are no longer pointing to price rises being quite as steep as those in the autumn. However, this trend varies significantly from sector to sector. Firms in the wholesale and manufacturing sectors, for example, are planning to raise their prices less frequently than they did before. In contrast, the construction industry and other service providers are planning more price increases. Pricing intentions have changed little in the retail and hospitality sectors.

Since the summer of last year, KOF has also been asking companies on a quarterly basis about their expectations for future Swiss consumer price inflation. Here, too, the results suggest that the situation is easing. Whereas, back in the autumn, firms had expected to see an inflation rate of 3.7 per cent over the next twelve months, they now expect prices to rise by 2.9 per cent over this period. When asked about a time horizon of five years, companies last autumn gave a forecast of 3 per cent. Survey respondents now reckon that the inflation rate in five years’ time will be around 2.6 per cent.

Business in the manufacturing sector is picking up again

The business situation in the manufacturing sector recovered strongly in January. The problem of shortages of materials and intermediate products is clearly becoming less acute. Complaints about these shortages are decreasing in all manufacturing sub-sectors. Although firms expect the prices of their purchases to continue to rise sharply, they believe that prices have already peaked for the time being. Their assessment of their sales prices is the same. The pressure on earnings is no longer increasing. Companies are now not as sceptical as they were in the autumn of last year about the level of demand in the near future.

Construction activity is buoyant despite rising prices

The business situation in the two sectors associated with building activity – project engineering and construction – improved in January. Business activity in the construction industry is also very strong on a longer-term comparison. The earnings of construction companies are increasingly stabilising. In addition, firms are less sceptical about the future performance of their earnings than they were before. Construction companies intend to raise the prices of their services even more frequently than they did previously. The shortage of materials is no longer as serious as it was in the autumn or summer of last year. Overall capacity utilisation in the construction industry has risen sharply. Order books are still fairly full, and the shortage of workers is becoming an increasingly urgent problem.

Business situation improving in both the wholesale and retail sectors

Business in the retail sector improved for the second month in a row. Although it is also strong on a medium-term comparison, it remains below the level of activity observed at the beginning of 2022. Overall, retailers’ sales of goods have picked up recently and their earnings are performing much better than they did before. Although retailers plan to raise their sales prices in the next three months at a similar rate as they did previously, they expect to see stronger growth in their sales. Retailers in the food sector in particular are optimistic about the volume of sales going forward. The Business Situation Indicator for the wholesale sector is rising for the first time in six months. Although the demand outlook for companies in the wholesale sector has hardly changed, the problem of supply availability is becoming less acute. However, the issue of supply capacity has become much less critical.

Hospitality industry starting the new year on a positive note despite rising prices

Having dipped in the autumn, the Business Situation Indicator for the hospitality sector rose in January. Business is particularly good in the accommodation sector. Hotels in the mountain and lake regions were able to close the gap with those located in towns and cities. Room occupancy rates at hotels – even after seasonal adjustments – continued to rise. Foreign guests are responsible for much of this growth. Reservations for the current quarter are more numerous than they were at the same time last year. These businesses intend to raise their prices more or less as frequently as they did previously. Nevertheless, survey respondents are confident that demand for their services will continue to rise.

Financial and insurance service providers hoping for a turnaround in earnings performance

In January, the business situation of financial and insurance service providers noticeably improved from its year-end low in December. Survey respondents are also much more confident than before about the outlook for business growth over the next six months. Their earnings could be stabilised, and these institutions see an opportunity to increase their earnings in the near future. Banks expect to see growing demand for their services, especially from corporate clients. Although lending and deposit-taking should continue to guarantee success for the banks, survey respondents believe that fees and commissions could also perform fairly well again. Insurance companies report a modest increase in the number of their new policies. However, they hope that the downward trend in their net investment returns will slow significantly.

Business situation in other services improving

Following a gradual slowdown in business activity in the second half of last year, business in the other services sector is growing in early 2023. The business situation is improving considerably, especially in the transport and logistics sub-sector. In contrast, capacity utilisation has fallen at information and communications firms and in business-related services. General uncertainty about the future course of business is decreasing slightly among service providers. The labour shortage continues to be a major concern for service providers, and complaints about the lack of skilled workers have risen further.

The results of the KOF Business Tendency Surveys for January 2023 include the responses of around 4,500 firms from manufacturing, construction and the major service sectors. This equates to a response rate of around 59 per cent.

The detailed results of the KOF business surveys (including tables and graphs) can be found Downloadhere (PDF, 526 KB).

Contact

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland