Financial bottlenecks slowing investment growth

Although Swiss companies intend to curb their pace of investment in 2023, this slowdown does not point to a recession. According to the results of the semi-annual KOF Investment Survey, investment growth is likely to slow from a nominal 5.3 per cent last year to 3.9 per cent in the current year. Financial bottlenecks in particular are having a dampening effect on investment expectations.

Although gross fixed capital formation is expected to increase again this year, its growth is likely to be lower than it was last year. This is shown by the results of the latest KOF Investment Survey from autumn 2022, according to which survey respondents expect their fixed capital investment to rise by a nominal 3.9 per cent in 2023. The survey’s results indicate that growth of 5.3 per cent is expected for last year. The fact that investment growth is likely to weaken in the current year is not surprising in view of the energy crisis and rising interest rates. What is surprising is the resilience of investment to the gloomy economic situation. Investment expectations for the current year do not reveal any recessionary tendencies, which is consistent with KOF’s economic forecast from December 2022.

Industry and the construction sector in particular are slowing their pace of investment compared with last year. Having increased their investment by 8 per cent in 2022, companies from the manufacturing sector plan to raise it by only 2 per cent in the current year. Firms in the construction sector even plan to reduce their investment by 3 per cent in 2023 after having raised it by 3 per cent last year. Only in the services sector is investment growth expected to prove robust. Investment here is predicted to rise by around 5 per cent, similar to last year.

The planned capital expenditures will primarily go towards new buildings and the conversion of commercial and business premises. 44 per cent of survey respondents intend to increase their construction investment this year (compared with 31 per cent last year, according to the previous survey in autumn 2021). The proportion of companies that plan to invest in research and development this year has also grown significantly on balance. The number of firms intending to increase their investment in equipment and machinery is roughly the same as it was last year (38 per cent).

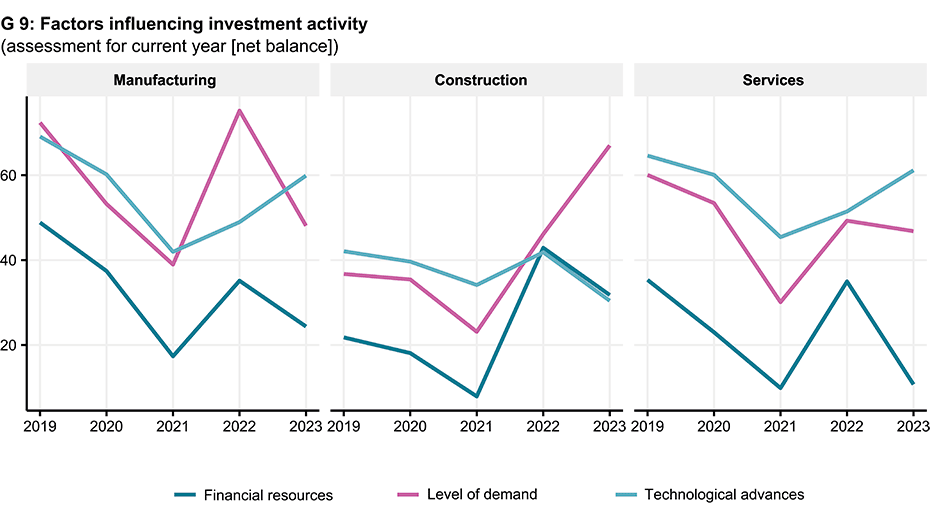

Uncertainty and financial bottlenecks weighing on investment prospects

The investment figures collected for the year 2023 are merely plans whose realisation was not yet certain at the time of the survey. In order to establish the precision of the rates of change resulting from these plans, companies were asked about the certainty of realising their planned investment. In autumn 2022, just under 12 per cent of firms rated their investment plans for 2023 as uncertain. This is around a third more than in the previous year and reflects an investment environment that is proving challenging in view of heightened geopolitical tensions and a gloomy global economic outlook.

The survey’s results show that the financial resources available and the expected earnings situation in particular are having a much less positive impact on investment plans for 2023 than they did a year ago (see chart G 9). Just under one-fifth of the companies surveyed say that the financial resources available will either slightly or significantly dampen their investment this year. In autumn 2021 this was the case for only 9.6 per cent of firms. While this trend can be observed in all sectors, it is most pronounced in services.

Technological progress stimulating investment in environmental protection

In contrast, survey respondents believe that technological advances will have a stimulating effect on investment during the current year. Their importance as an influencing factor has risen on balance from 49.7 points to 57.5 points compared with last year. This increase is primarily due to the manufacturing sector (see chart G 9). Around 46 per cent of the industrial firms questioned in the previous survey said that their investment plans would be positively influenced by technology. 58 per cent of survey respondents from the manufacturing sector expect this to be the case for 2023. Technological progress is thus replacing the demand outlook as the most important driver of investment expectations in industry. This trend is being accompanied by a sharp increase in the proportion of companies that plan to adapt their existing product ranges to the state of the art and add fewer new products to their ranges.

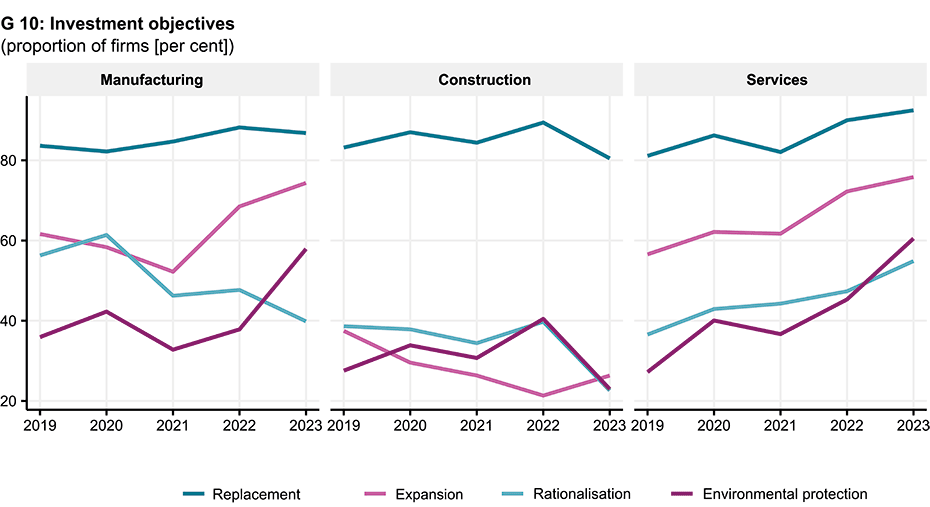

The main investment objective is still to replace existing fixed assets. At the same time, investing in environmental protection and in compliance with trade law requirements has become much more important (see chart G 10). 57 per cent of the companies surveyed say they intend to invest for this purpose this year. In autumn 2021 this was the case for 45 per cent of firms. Similarly, the importance of investment in expanding production and service provision has increased slightly. 72 per cent of companies plan to expand their operational capacity this year (compared with 69 per cent in autumn 2021).

The investment survey

Economic growth is strongly influenced by companies’ investment activity. For this reason, the KOF Swiss Economic Institute at ETH Zurich conducts a survey of domestic firms every spring and autumn. The semi-annual survey in autumn 2022 was conducted from 26 September to 24 December. Of the 5,826 companies contacted, 2,398 responded, which equates to a response rate of 41 per cent.

Contact

KOF FB Konjunkturumfragen

Leonhardstrasse 21

8092

Zürich

Switzerland