Energy crisis and rising cost of living slowing down global economy

In Europe, persistently high inflation and high energy costs are likely to continue to weigh on demand. In the United States, inflation is leading to a loss of purchasing power, while rising interest rates are dampening investment. The outlook for the Chinese economy has also darkened.

International supply chains, which remained strained by the sudden recovery in demand following the easing of government restrictions during the pandemic, were hit hard by the outbreak of the war in Ukraine. War-related production losses, raw-material supply shortages as a result of the sanctions imposed on Russia, and Russia’s halting of supplies to the EU have further exacerbated the situation. European – especially German – industry, which is heavily dependent on Russian oil and gas, has suffered particularly. The gradual boycott of Russian oil by the European Union and its allies, which ended with a partial embargo on Russian oil, has forced the EU to find new oil suppliers. At the same time, Russia has imposed counter-sanctions in the form of gradual gas supply freezes. Faced with the threat of gas shortages, gas storage facilities in Europe have been stocked up and large quantities of gas have been hedged by means of forward contracts, causing European gas prices to skyrocket while supply has remained unchanged. European electricity prices have risen sharply in response. In addition, the ongoing production restrictions in place at French nuclear power plants continue to constrain European electricity supplies.

Further escalation in the energy market halted for the time being

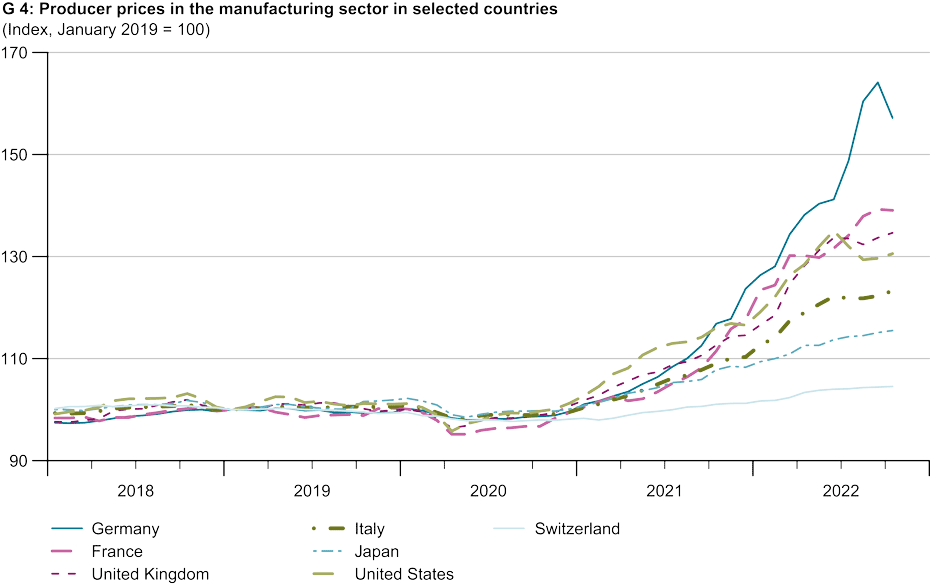

Rising electricity and commodity prices have fuelled enormous increases in producer prices in the manufacturing sector (see chart G 4). However, these rises in producer prices have slowed down or even declined in recent months. The reason for this is, firstly, that supply chain problems have partly eased and congestion at the ports has largely dissipated, causing freight rate prices to fall. And, secondly, commodity prices – especially those for oil and gas – are now lower than they were at the beginning of the year. This is partially due to the expansion of supplies through the development of new oil and gas suppliers, the successful replenishment of liquefied natural gas (LNG) storage facilities and the completion of new LNG terminals. Demand has also been reduced by government energy-saving initiatives, consumers switching to other energy sources, greater energy efficiency, and lower demand due to the relatively mild temperatures in November and the global economic slowdown. In addition, the oil, gas and electricity price caps imposed by European governments are likely to limit further increases in energy prices.

Inflation set to remain elevated for some time

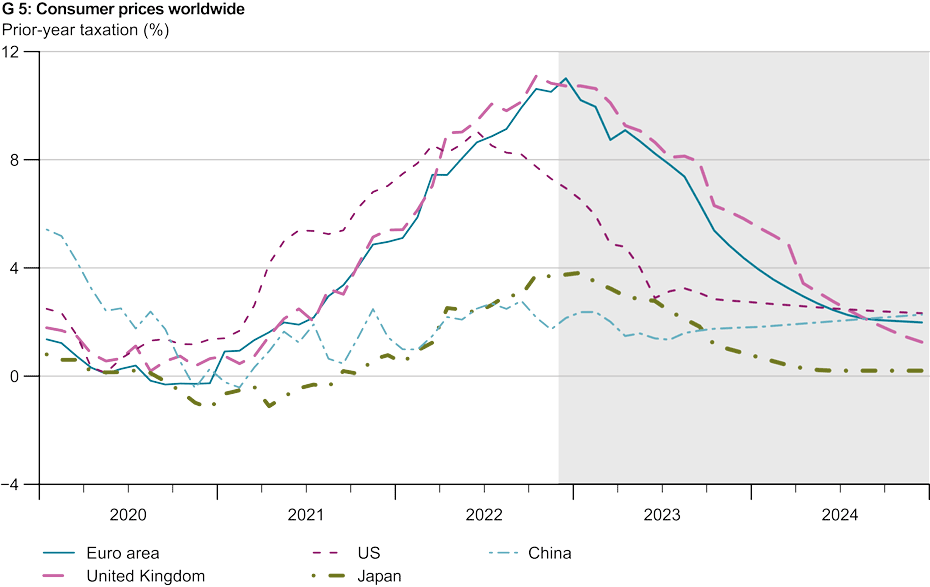

The high energy prices have continued to fuel consumer prices in recent months, both directly and indirectly, in the form of higher prices of food, services and industrial goods. The energy price component of consumer prices should decline over the coming months owing to the fall in commodity prices and the energy price caps imposed by many European governments. However, inflation has been increasingly broad-based in recent months. Labour markets remain tight, and skill shortages together with high wage demands will keep core inflation rising for the time being before companies eventually reduce their demand for labour as a result of the decline in demand. In addition, various financial support measures introduced by European governments – such as inflation compensation payments, heating cost subsidies, tax breaks and other one-off payments – are likely to support consumption in the short term but also to drive inflation. This should cause inflation to remain elevated for some time. Nevertheless, inflation is likely to peak gradually even in the euro area (see chart G 5). The United States already reached this turning point back in June. Inflation has been falling since then. KOF expects inflation to decline over the forecasting period but to remain higher than central banks’ inflation targets for a while longer.

Economic downturn postponed until winter

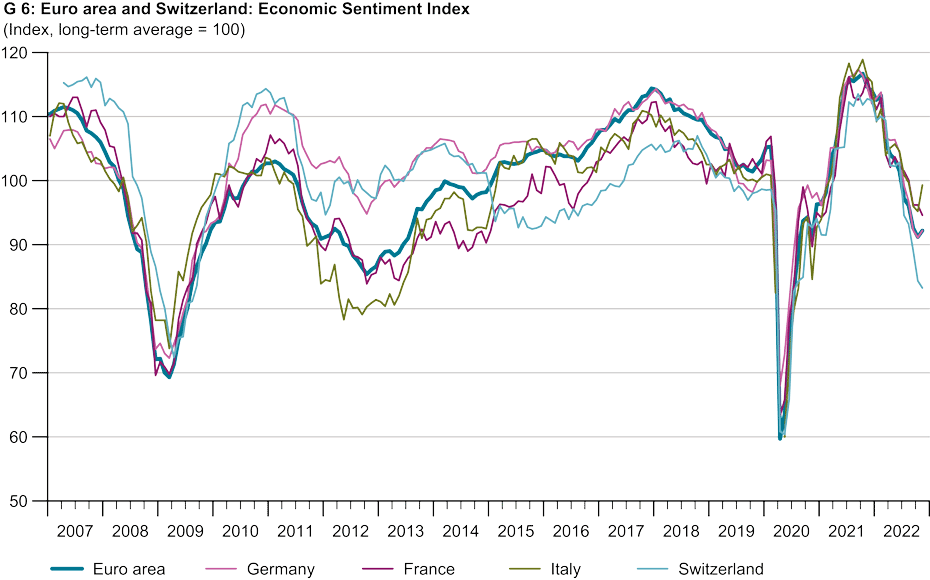

Although the real economy performed well in the third quarter of 2022, this is not expected to continue in the fourth quarter. The positive trend in the third quarter was largely driven by one-off effects. Private consumption in Europe was still strong despite high inflation, which is likely due to COVID-related catch-up effects. Savings accumulated during the pandemic continued to be reduced, thus further supporting consumption. In the US, the third quarter was boosted by high military spending and energy exports, while private consumption remained stable and the weakness of investment continued. The Chinese economy rebounded sharply in the third quarter as a result of its recovery from the summer lockdown measures. However, its performance going forward is likely to become increasingly gloomy from the coming quarter onwards. Key leading indicators such as the Economic Sentiment Index (ESI) for all countries had fallen so sharply by the end of the autumn that, even if these indicators recover, Europe’s economic downturn is likely to be broadly based across almost all countries over the winter (see chart G 6).

Even though the ESI has calmed down somewhat recently and the uncertainty about energy supplies has decreased over the winter, persistently high inflation and high energy costs are likely to continue to weigh on demand in Europe. On the production side, energy-intensive sectors and manufacturing industry in particular are suffering in the current climate. Firms’ backlog of orders is likely to be gradually processed, while new orders are increasingly declining. The UK is also still struggling with the consequences of Brexit, resulting in greater labour shortages, higher goods prices and continued weak investment and trade with the EU. In the US, too, persistently high inflation is denting purchasing power, which is weakening private consumption, while rising interest rates are dampening investment. The outlook for the Chinese economy has darkened as a result of its burgeoning property crisis, weak global demand, and domestic tensions owing to the renewed rise in COVID-19 infections and protests against the government’s zero-COVID policy. A decline in aggregate output in many advanced economies by mid-2023 remains highly likely. Forecasting world GDP weighted by Swiss exports, KOF expects to see growth rates of 2.9 per cent this year, 0.5 per cent for 2023 and 1.9 per cent for 2024, which are very similar to its autumn forecast (2.6 per cent for 2022, 0.6 per cent for 2023 and 1.9 per cent for 2024).

Many risks in both directions

KOF’s forecast is subject to the assumption that the war in Ukraine will continue and the sanctions against Russia will remain in place during the forecasting period. Furthermore, KOF presumes that Russia will continue to halt gas supplies to the EU and that the production restrictions in place at French nuclear power plants will only be partially overcome during the winter. Its forecast is based on the assumption that European governments will continue to provide financial support and that power shortages can be avoided this winter and next winter by saving energy and developing new sources. Finally, KOF does not expect any new far-reaching COVID 19-related restrictions to be introduced.

There are various downside risks to the forecast. For example, government financial support measures and higher wage increases could fuel private consumption in the short term and trigger second-round effects that drive inflation. This would necessitate tighter monetary policy, which is likely to cause a more severe economic downturn. High levels of government debt, especially in Europe, could force governments to adopt austerity measures that prolong the crisis or weaken the subsequent recovery. Renewed COVID-19 outbreaks in China might lead to widespread lockdowns and once again exacerbate supply chain problems. Such lockdowns, political tensions and the country’s property crisis could trigger a more severe downturn there. Geopolitical tensions might intensify. The war in Ukraine could bring about greater bloc formation and weaken globalisation. Any escalation of the conflict between China and Taiwan might seriously affect global semiconductor production and further exacerbate East-West divides.

In contrast, it is possible that existing supply chain problems will ease sooner than expected, the expansion of, and transition to, new energy sources in Europe will progress more quickly and energy prices will decline faster. Consumption might provide further support to the economy through a greater reduction in savings, and lower interest-rate rises would dampen investment less than expected. Geopolitical tensions could ease unexpectedly, while a successful vaccination campaign in China could boost the country’s economy. Downside risks have become less significant compared with the most recent forecast.

KOF’s latest economic forecast for Switzerland is available external pagehere.

Contacts

KOF FB Konjunktur

Leonhardstrasse 21

8092

Zürich

Switzerland

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland

KOF FB Konjunktur

Leonhardstrasse 21

8092

Zürich

Switzerland