KOF Business Tendency Surveys: The Swiss economy is losing momentum

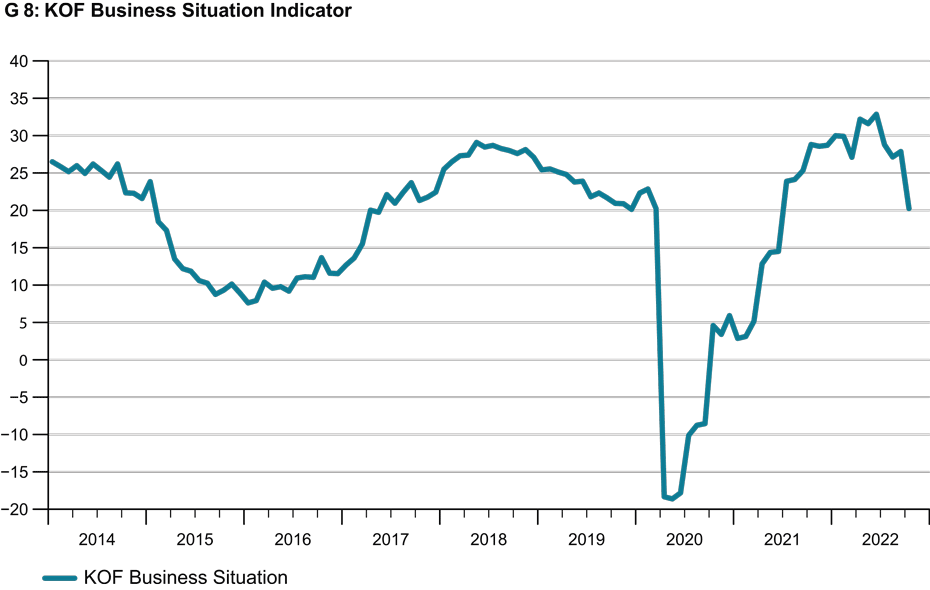

The KOF Business Situation Indicator for the Swiss private sector fell significantly in October (see chart G 8). Although business remains predominantly encouraging according to the KOF Business Tendency Surveys, the last time the indicator was lower than it is at present was in June 2021.

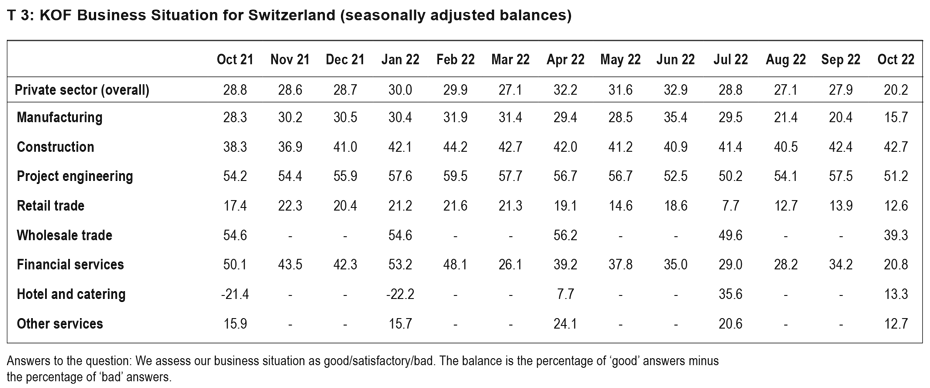

The stimulus resulting from the relaxation of the COVID-19 restrictions is running out. This is because business is slowing in the very sectors that benefited from it, namely hospitality and services. In virtually all other sectors surveyed, however, the Business Situation Indicator declined in October, falling in financial and insurance services, the wholesale trade, (again) in manufacturing, (slightly) in the retail sector and in project engineering. Only the construction industry performed fairly well (see table T 3).

Companies in Switzerland are planning to raise their prices even more frequently than before. The tendency to increase prices across almost all sectors is very strong over the medium term. Prices have recently risen even further, especially in the hospitality industry, among service providers and in manufacturing.

Easing shortages of intermediate products

Although shortages of materials and intermediate products continue to pose a problem for firms, there are some signs that the situation is easing. Wholesalers are expecting delivery times to increase less frequently than they did previously, and the manufacturing and construction industries are no longer complaining quite as often about shortages of materials and intermediate products. In the construction industry the lack of workers has actually been more significant than the shortage of materials for some months now.

Business activity in the manufacturing sector is slowing

The Business Situation Indicator for the manufacturing sector continues to weaken, falling at a faster pace in October and for the fourth month in a row. In addition, uncertainty about future levels of business has increased markedly. Both export-led and domestically focused firms reckon that their current business situation is less encouraging than it was before. The Swiss franc exchange rate is probably also having an impact, and firms’ competitive position in foreign markets has come under pressure. Since companies fear a slowdown in demand more often over the next three months, they are more cautious about purchasing intermediate products. Despite encountering difficulties with procurement, firms are now well-stocked with intermediate products. The problem of shortages of materials and input products is becoming less significant. Nevertheless, almost half of the businesses surveyed are still complaining about production constraints caused by shortages of materials and input products. Sales prices are likely to continue to rise significantly, with prices projected to climb sharply overall. Nevertheless, companies will not be able to sustain their current levels of earnings.

Order books in the building-related sectors are fairly full

The levels of business activity in the building-related sectors of construction and project engineering varied in October. The situation in construction remained as encouraging as it had been in the previous month, while there was a slight deterioration in the project engineering sector. Although the earnings situation in project engineering is not progressing as well as had been hoped, more projects are now being processed than previously. Project engineering firms’ order books are fairly full and they are looking to increase their staffing levels. They plan to boost their future earnings by raising their prices even further. Order books in the construction industry, too, are increasingly filling up. However, production levels have not followed suit, and capacity utilisation has declined slightly. The shortage of materials continues to be a problem, but its intensity is clearly decreasing. In contrast, staff shortages are becoming more significant as a constraining factor and are even more important than the shortage of materials.

Business in the retail sector remains more or less stable

Retailers rated their business situation in October as being almost as encouraging as in the previous month but much less buoyant than at the beginning of the year. Their level of business activity is now only average. Overall, however, goods sales are no longer performing quite as poorly as in previous months. Although retailers are still planning widespread price rises, this tendency did not increase any further in October. Companies hope that sales will not suffer despite these price rises. Regardless of the price increases already implemented, earnings have come under fairly strong pressure. Business activity in the wholesale trade continues to slow. Although the situation here remains buoyant, it is no longer as exceptionally positive as it was at the beginning of the year. There are now far fewer people talking about further increases in delivery times for the wholesale trade in producer goods, while the problem for the wholesale trade in consumer goods appears to have at least peaked for the time being. The upward pressure on prices is decreasing in the wholesale trade in producer goods, while it continues to increase in the wholesale trade in consumer goods.

Business activity in the hospitality industry is faltering

Business in the hospitality sector has slowed significantly for the first time since the beginning of 2021. This is due to the food-service sector, where the business situation is less encouraging than it was in the previous quarter. In the accommodation sub-sector, on the other hand, business activity is holding up. There are also striking differences between the various tourism zones. Business in the major towns and cities is improving in both the food-service and accommodation sub-sectors. In contrast, both sub-sectors are faltering in the mountain and lake regions. Overall, accommodation providers have managed to more or less maintain their occupancy rates owing to an increase in foreign guests. Looking ahead to the coming months, these businesses are hoping to receive larger numbers of bookings from foreign visitors. There is very little potential for increasing the numbers of domestic visitors. Price rises are being planned more frequently than before in both the accommodation and food-service sub-sectors.

Business activity in financial services is slowing significantly

The Business Situation Indicator for the financial and insurance services sector slumped again in October after rallying in the previous month. Although the business situation here continues to be viewed positively on balance by these institutions, the last time the indicator was lower than it is at present was in April 2020. Although the business outlook for the coming six months is slightly more upbeat than it was last month, it does not indicate a strong recovery. Once again there is less scope for earnings growth than there was previously, and uncertainty about future levels of business is increasing. Banks’ income from fee and commission business and from proprietary trading tends to be under pressure anyway, and their fee and commission business is likely to weaken further. Their hopes are increasingly resting on their interest-earning business. The volume of assets under management is clearly decreasing. At least these institutions are now more confident about the level of demand for lending to corporate clients than they were in the previous quarter.

Costs are putting pressure on earnings in other services

Business activity in other services slowed for the second month in a row. The Business Situation Indicator’s pre-pandemic levels are thus increasingly becoming unattainable. Nevertheless, capacity utilisation is still encouraging and almost as high as it was at the beginning of the summer. Capacity utilisation in the transport, information and communication sub-sectors has been dampened. In contrast, capacity utilisation in business-related and personal services remains above its average for 2018 to 2019. Consequently, staff shortages have become more entrenched. However, it has not been possible to improve earnings any further. Firms are therefore once again more likely to try to impose price increases. The greater tendency towards price rises applies throughout the sectors of transport, information and communication as well as in business-related and personal services.

The results of the KOF Business Tendency Surveys for October 2022 include the responses of around 4,500 firms from manufacturing, construction and the major service sectors. This equates to a response rate of around 58 per cent.

The detailed results of the KOF business surveys (including tables and graphs) can be found on our website.

Contact

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland