COVID-19 pandemic, war in Ukraine and appreciation of the Swiss franc: impact on tourism in Switzerland

Much higher energy prices and the threat of recession abroad are depressing sentiment in the tourism industry. However, KOF expects to see growth in overnight stays thanks to the ongoing recovery from the pandemic and the strength of domestic tourism.

The appreciation of the Swiss franc since the start of the war in Ukraine (up by 5.5 per cent in real terms and by 8.5 per cent in nominal terms) and a looming recession in neighbouring European countries are creating uncertainty for the coming tourism seasons. A one-off analysis conducted by KOF shows that German and Dutch visitors in particular will be negatively impacted. Other trends – such as the continuing tendency on the part of Swiss guests to take more holidays at home, as well as robust demand from overseas markets – should ensure that the number of overnight stays in Switzerland stabilises over the coming years. The winter season is expected to see an increase of 2.4 million overnight stays (up 16 per cent) compared with last year. Although the effects of a recession in neighbouring countries will slow growth during the summer, the arrival of many Asian guests should ensure a modest rise of 0.7 per cent. KOF is forecasting a further increase in long-haul travellers and a higher share of domestic tourists over the long term compared with the pre-pandemic period.

Uncertainty around levels of tourism demand going forward

The COVID-19 pandemic, the war in Ukraine and the Swiss franc exchange rate are strong drivers of change and uncertainty in the tourism sector. As the pandemic subsided, for example, many people’s surplus savings were spent on holidays, causing a boom in domestic travellers within Switzerland. On the other hand, the economic environment remains the most important factor affecting the recovery of international tourism. Rising inflation and soaring energy prices are pushing up transport and accommodation costs, putting pressure on consumers’ purchasing power and savings. For these individuals the recent price increases are likely to cause a shift towards cheaper options such as holidaying in nearby countries or choosing more affordable transport options.

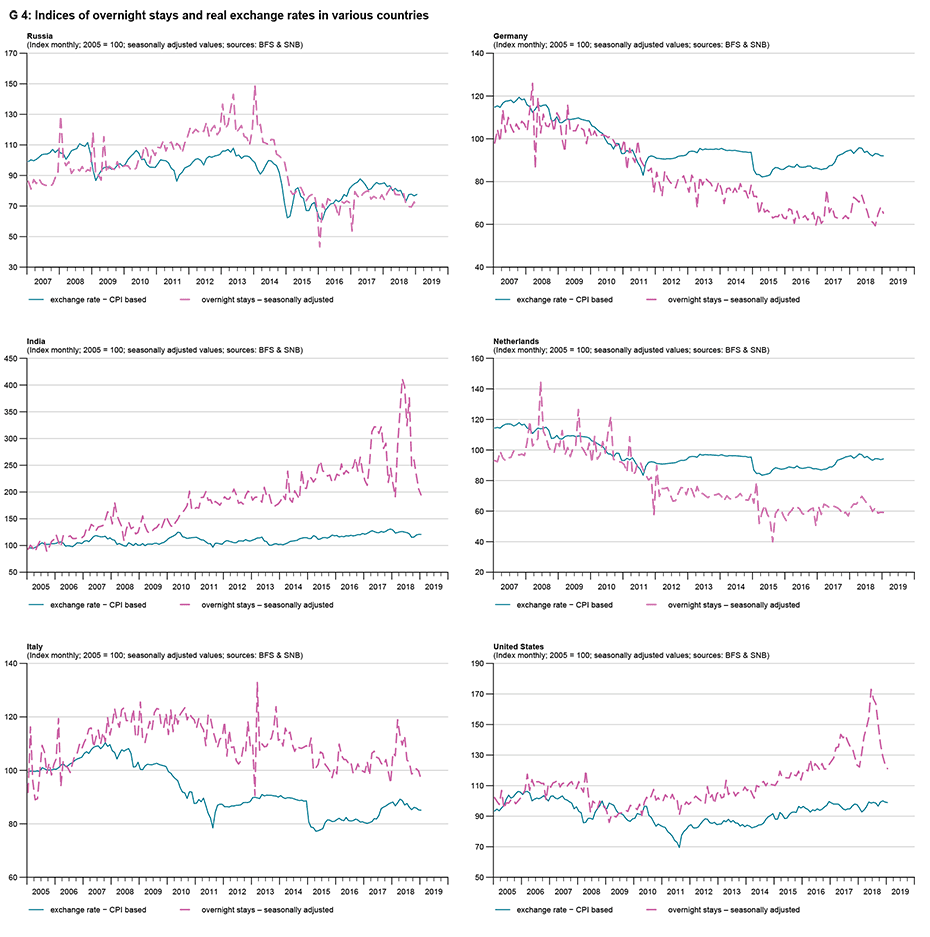

To what extent this trend applies to Switzerland remains unclear because, compared with other holiday regions in Europe, prices in Switzerland are higher and the relevant demographic is wealthier and probably less price-sensitive. However, there are differences between the various countries of origin. For example, chart “G 4: Indices of overnight stays and real exchange rates in various countries” shows that there is indeed a correlation between the number of tourists and the real exchange rate, as can be seen from the examples of Germany and the Netherlands. A less coherent picture emerges in the cases of the United States and India. To enable us to make statements about the future performance of various tourism regions as precisely as possible, statistical methods are used below to estimate real exchange-rate elasticities. In our case, exchange-rate elasticity shows how a movement in the Swiss franc exchange rate has a proportional effect on the number of overnight stays. If the exchange-rate elasticity is less than one, the movement in the exchange rate has less impact on the change in overnight stays.

How do different countries react to exchange-rate movements?

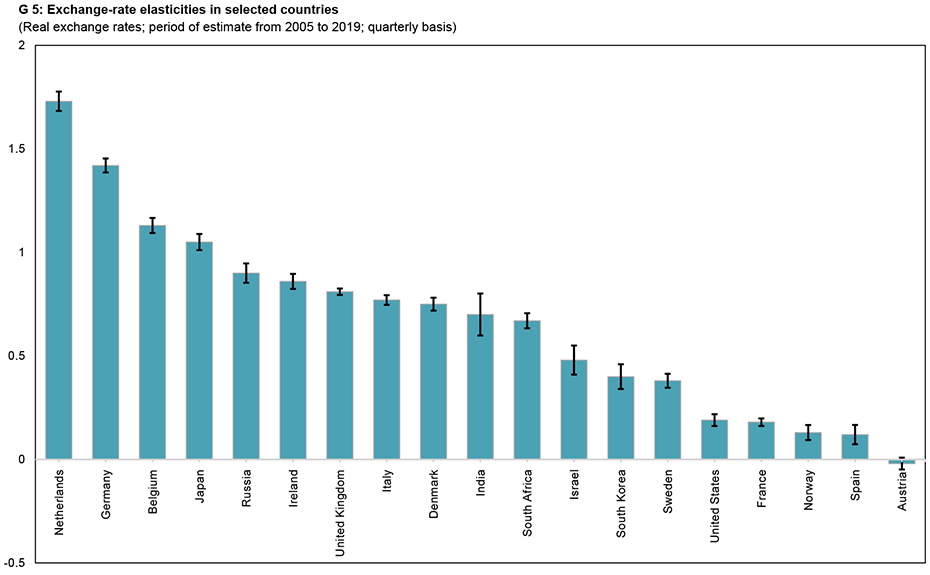

How are overnight stays in Switzerland affected by exchange-rate movements abroad? KOF uses the real exchange rate weighted by consumer prices in order to better and more accurately capture the effects of exchange-rate movements. All time series are seasonally adjusted and on a quarterly basis. To ensure that these effects are not overly influenced by exceptional events, the analysis only looks at data up to 2019, so the effects of the COVID-19 pandemic are not taken into account.

The reaction of tourists from other European countries tends to be more pronounced, which is probably due to substitution effects. This means that when the Swiss franc is strong, people from these nations tend to switch to other countries. It is plausible that they go to other Alpine countries with a similar tourism offer

This does not include the exchange-rate elasticities of Italy and Austria, which are relatively low. One possible reason for this low elasticity is that these countries already have a similar local tourism offer and many of them are increasingly becoming regular destinations

Overseas travellers from the US are less price-sensitive

Long-haul travellers from the United States and other countries react much less strongly. This is probably because many Americans combine a holiday in Europe with an additional stay in Switzerland, and a long-distance trip is often a one-off event that takes place regardless of any exchange-rate elasticities, or the exchange rate of the euro is more important than that of the Swiss franc when such travel is being planned.

Estimates of exchange-rate elasticities for almost all countries have fallen sharply compared with previous calculations (cf. Abrahamsen and Simmons-Süer, 2011). We can conclude from this that the relevant demographic has changed over the years. Those who have spent their holidays in Switzerland in recent years are unlikely to have been guided by prices. Price-sensitive guests have probably opted for other destinations and are holidaying in less expensive countries. The negative effects of any appreciation are therefore likely to be less pronounced than in the past.

German and Dutch tourists set to react more strongly to appreciation of Swiss franc

Forecasts of overnight stays, in which elasticities are particularly important for long-term trends, suggest that German and Dutch guests are likely to react particularly sensitively to the appreciation of the Swiss franc and that the long-term trend relating to these travellers will be revised downwards as a result. These regions are increasingly likely to look for cheaper alternatives in neighbouring countries during the summer months, thereby avoiding Switzerland. The assumption is that the euro exchange rate will remain at a higher level throughout the coming summer season. The decline in tourism during the winter is likely to be less pronounced owing to Switzerland’s lower price sensitivity because of its already higher costs.

On the other hand, markets such as India and the US, which have grown significantly in recent years, are proving to be extremely robust. In summary, it can be said that Switzerland is likely to experience less dramatic declines than neighbouring countries owing to its already higher prices. The real effect in Switzerland is smaller than the nominal effect.

Assumptions about medium- and long-term demand trends

The outlook for the medium- and long-term trends in tourism is now better than previously assumed. The recovery in the numbers of overnight stays from overseas markets (such as the US, India and Southeast Asia) has been faster than expected. In addition, domestic guests are continuing to stay in their home country to a greater extent.

However, looming recession in many key countries of origin is likely to reduce tourism spending. Consequently, the positive and negative effects on Switzerland as a tourism location are overlapping, thereby increasing the associated forecasting risks. Looking ahead, KOF is making the following assumptions about the relevant tourism regions:

Europe: KOF’s analysis of exchange-rate elasticities shows that guests from Germany and the Netherlands in particular will tend to stay away owing to the higher real exchange rate. Another negative signal is likely to come from the nominal parity of the Swiss franc and euro. Although this is only a nominal increase and does not take account of changes in the prices of tourism goods, it is a signal that is likely to deter some tourists. A brief look back to the past reminds us of a similar scenario following the financial crisis in 2009, when the numbers of tourists from Germany fell by almost 8 per cent the following year. However, the decline in overnight stays is expected to be much less dramatic. For one thing, the recession is likely to be much less severe and, for another, the relevant demographic is now different. In addition, the Swiss franc has appreciated much less in real terms than it did back then. At the time of the financial and euro crisis the relevant increase was 32 per cent between 2008 and 2011 (April to August). Only in the coming summer is the recession effect likely to predominate and slightly reduce the numbers of visitors from Europe. According to KOF’s forecast, economic output in Europe is therefore expected to decline in the first and second quarters of 2023.

Long-haul travellers: In contrast to European guests (down 3 per cent), the numbers of long-haul travellers are still significantly below their pre-crisis levels (down 34 per cent). The positive recovery effects continue to predominate among these guests. Above all, regions in Asia remain far below their pre-crisis levels, with overnight stays by tourists from Japan, Korea and China showing the greatest reductions. It was not until October 2022 that the Japanese government lifted warnings against non-essential foreign travel due to COVID-19. The return of Asian tourists should stimulate growth next summer. Strong long-term trends are coming primarily from India, where a significant and growing affluent segment of the population travels to Switzerland. The outlook for China – an important tourist destination – remains gloomy and it is difficult to estimate when guest numbers will pick up again. The numbers of long-haul travellers are unlikely to return to their normal pre-crisis levels until Chinese visitors return to Switzerland.

Domestic tourism: Domestic guests continue to sustain the high levels of overnight stays in Switzerland. Since the outbreak of the pandemic, overnight stays by domestic guests have increased enormously owing to the unavailability of foreign travel. This trend continued last year and this summer and is expected to continue further, albeit to a lesser extent. Long-distance travel by Swiss tourists is forecast to bounce back as a result of better long-term planning. However, the relevant proportion should not be too high as rising air fares and domestic tourism offers will dampen this growth.

Return to pre-crisis levels during the winter season

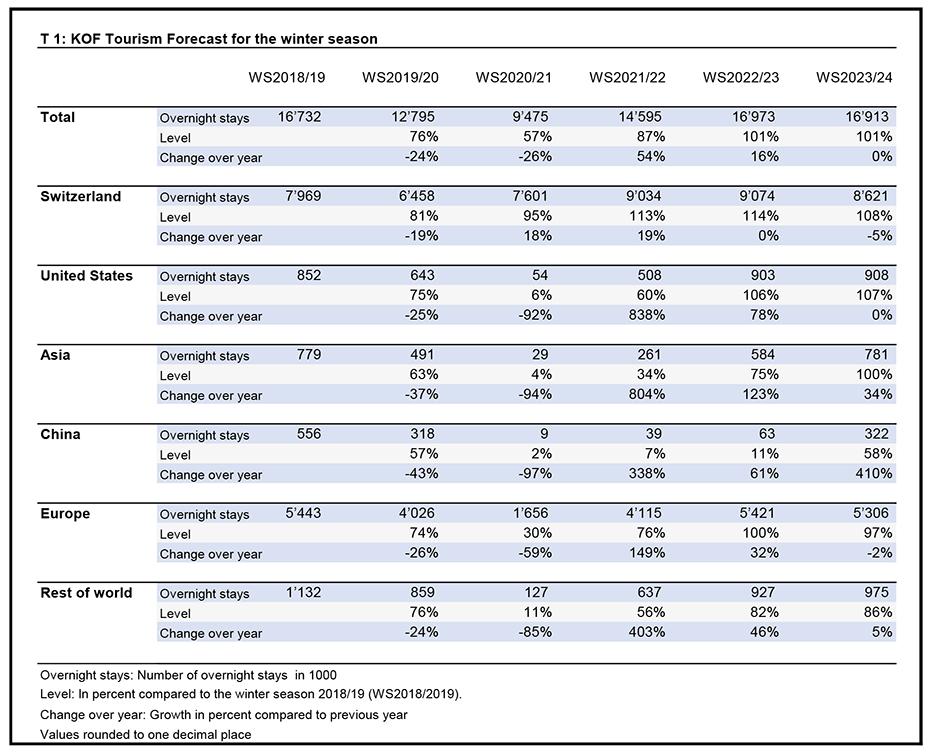

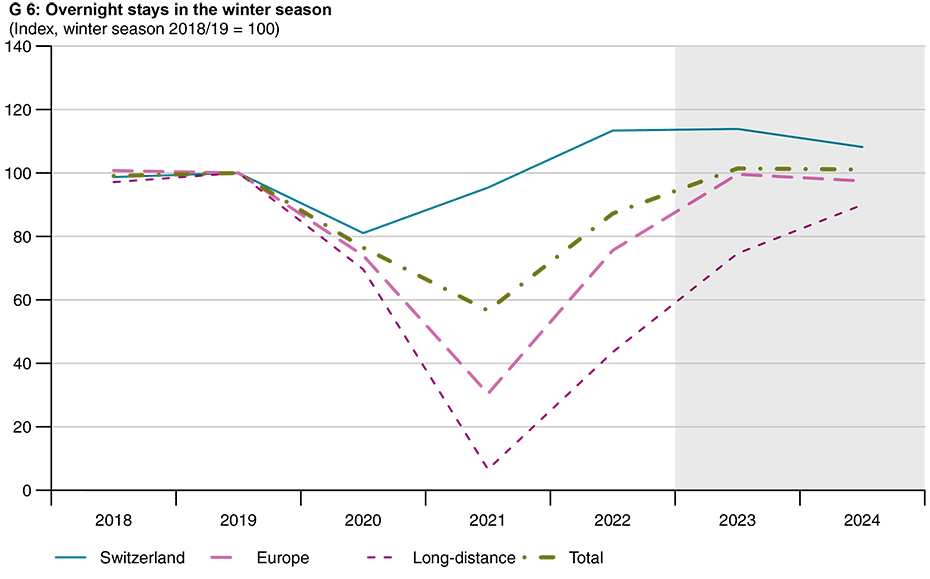

KOF is forecasting almost 2.4 million more overnight stays (up 16 per cent) for the 2022/2023 winter season than in the previous winter season (T 1). This represents a return to pre-pandemic levels (G 6). The first few months of the winter season – especially November and December – should be better than last year, when a wave of COVID infections meant that there were fewer guests at that time. Last winter, for example, the outbreak of a new coronavirus variant caused a sharp drop in European visitors. Such a decline is unlikely this winter unless the pandemic situation worsens. The growth forecast for the winter season is a result of the previous very strong summer months, which were already above their pre-crisis levels (119 per cent for France and 116 per cent for Switzerland in August). These strong summer months show that the desire to travel is still very high following the pandemic. This coming winter – probably the first skiing season without too many restrictions – should benefit from this urge to travel. Because the impact of energy prices and a weaker economy is slowing this trend, growth of only slightly more than 1 per cent in overnight stays can be expected compared with the penultimate winter season. Any worsening of energy prices or a reduction in supply due to labour shortages continue to pose a downside risk.

The 2023/2024 winter season is expected to reach a similar level. The unusually high numbers of domestic guests are expected to decline again slightly, while the return of Asian markets should stabilise growth. The declines in visitors from Europe due to the economic downturn should be smaller in winter as winter tourism is more robust because there are fewer alternatives available to skiing tourists.

The numbers of long-haul travellers will remain below their pre-pandemic levels over the forecasting period. Parts of the Asian market are still recovering slowly. Japanese guests, for example, have only been able to take very basic trips abroad since October 2022. Chinese visitors are seeing growth, albeit only very modest increases (reaching about 10 per cent of their pre-pandemic levels). Russian tourists will remain largely absent throughout the forecasting period. In the past they have been particularly strong during the travel months of January and February.

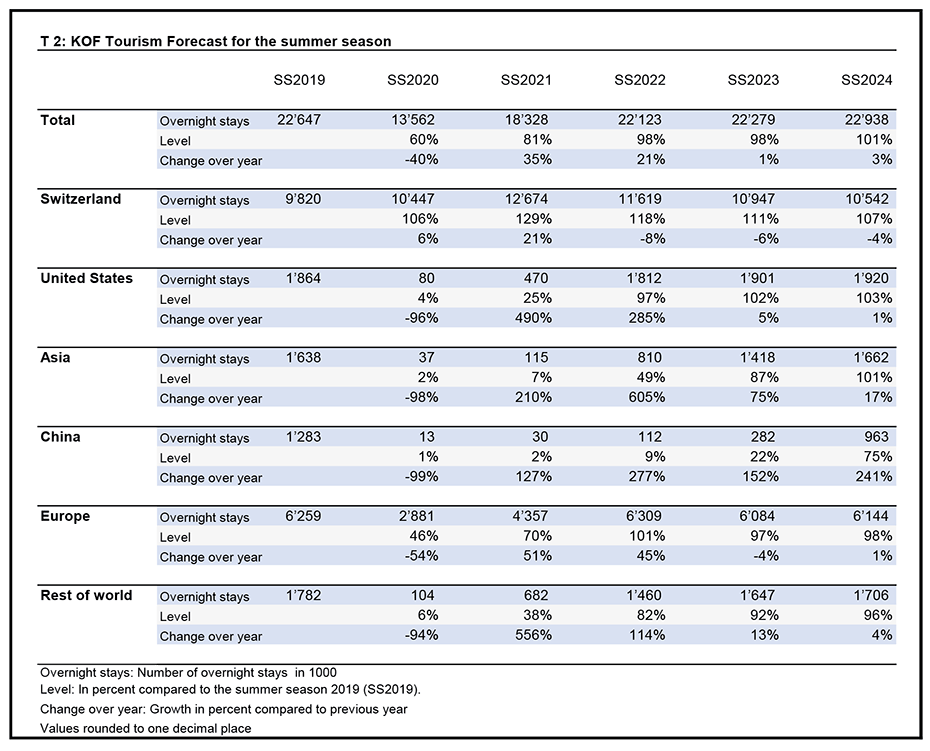

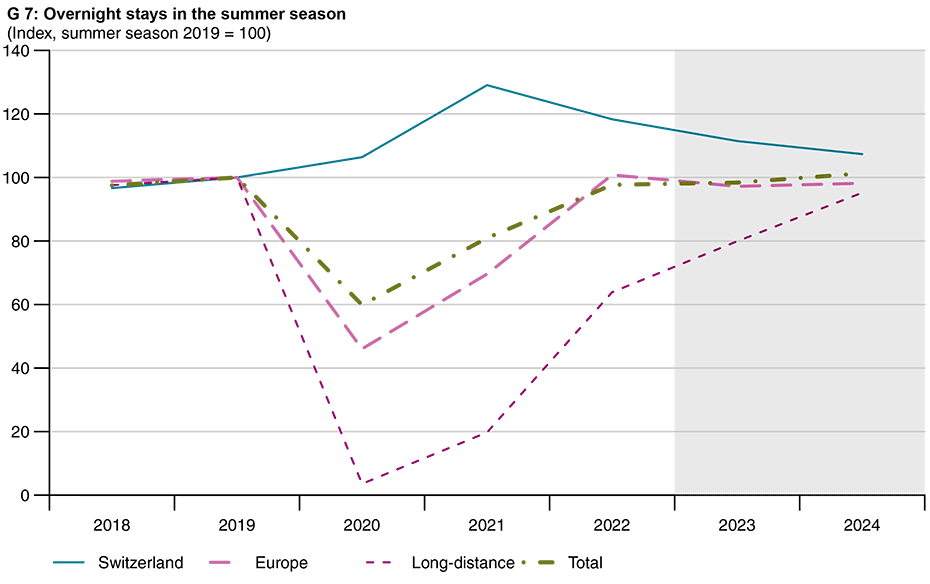

Summer marked by the return of Asian travellers

KOF is forecasting 0.16 million more overnight stays (up 0.7 per cent) for the 2023 summer season than during this year’s summer season (T 2). This almost represents a return to pre-pandemic levels (G 7). The economic slowdown in other European countries is then likely to make itself felt. The tourism potential in Europe should flatline over the medium term, assuming that the real exchange rate remains constant. The trend in 2024 is likely to depend mainly on the arrival of Chinese visitors and whether their numbers fully recover. For the purposes of this forecast it is assumed that the levels of Chinese tourists will not return to anything like normal until the summer of 2024. One positive scenario might be if China opens up soon, which could accelerate growth in summer 2023, although this is considered less likely.

Contact

KOF FB Konjunktur

Leonhardstrasse 21

8092

Zürich

Switzerland