Inflation rates remain high

Inflation in Switzerland, the euro area and the US is at historic extremes; the upward trend in prices is gaining breadth.

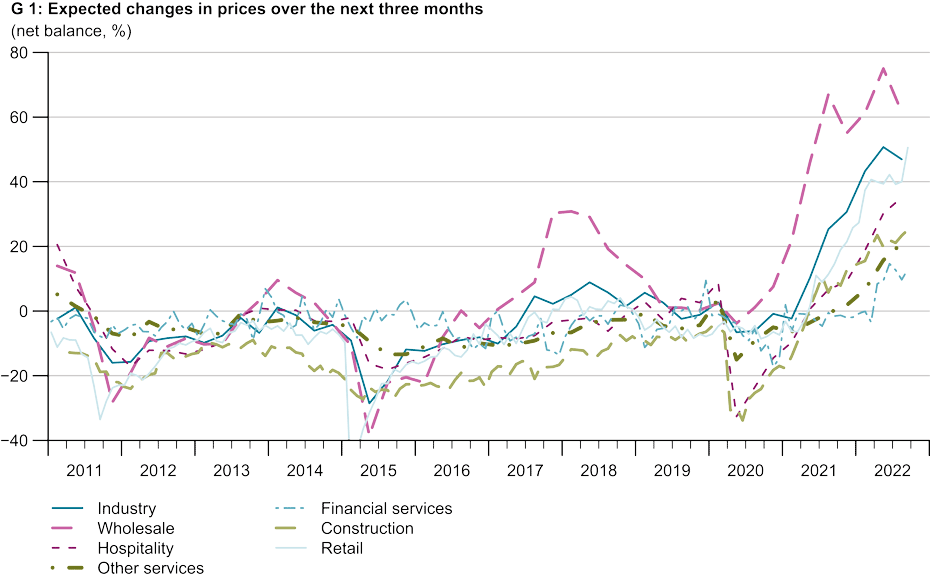

Inflation, as measured by the Swiss National Consumer Price Index (CPI), was 3.3 per cent in September after having been 3.5 per cent in August. In recent months it has hit its highest levels in almost thirty years. Its year-on-year increase is still mainly being driven by oil and gas, which are making housing and (air) travel considerably more expensive. Compared with September of last year the cost of heating oil alone has risen by 68 per cent and that of gas by 58 per cent. Overall, however, the upward trend in prices has also become more widespread; the recent increase in the prices of public services, for example, has been unusually strong. According to KOF’s Business Tendency Surveys, an unusually large number of firms are still planning to raise their prices over the next few months (see chart G 1). Switzerland is therefore following the international trend, although the general level of its price increases is still significantly lower. In the euro area, consumer prices rose by a historic 10 per cent in September (4.8 per cent core inflation), while the United States also reported an inflation rate of over 8 per cent in August (core inflation of 6.3 per cent). Chart G 2 shows that the local price rises in the consumer index are largely imported. Despite the large inflation differential, inflation of domestic goods is close to that of imported goods if energy is excluded. This is because the appreciation of the Swiss franc is dampening imported inflation.

Price pressures remain elevated

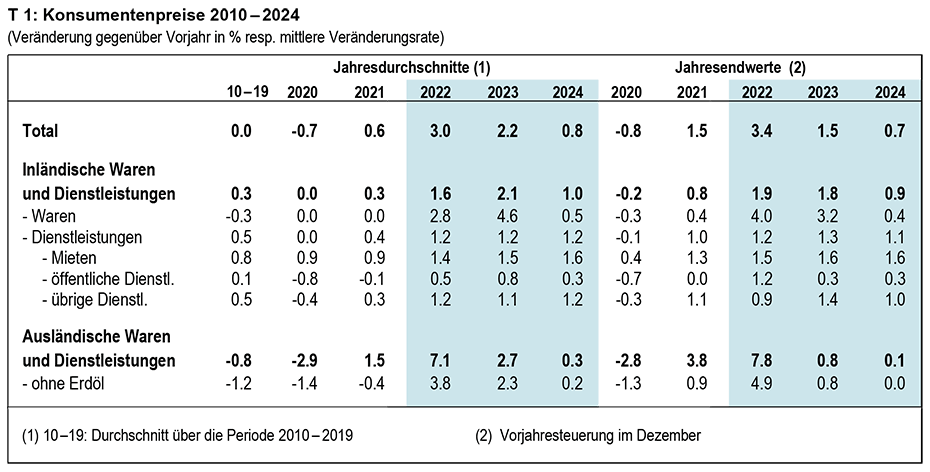

Given the stark flattening of economic growth, KOF does not expect the price of petroleum products to jump any further, which will bring about a decline in the corresponding inflation rates next year owing to the base effect. This will then be partially offset by the increase in electricity prices. Here, a new tariff for basic energy supplies will apply from next January, although this will be raised significantly by most suppliers owing to higher procurement costs. Average electricity prices for consumers will rise by 27 per cent. However, there is considerable regional heterogeneity. Overall, inflation rates within a range of 3 to 3.5 per cent can be expected over the coming months. Rising nominal wage growth will contribute to the upward pressure on prices, while the appreciation of the Swiss franc will curb imported inflation. In addition, the prices of goods affected by the COVID-19 pandemic and associated supply chain disruption and capacity shortages should continue to normalise over the forecasting period. Following the flattening of price rises and the expiry of base effects in energy prices, inflation in the second half of next year will return to within the range that the SNB defines as price stability. However, inflation in 2024 will remain significantly higher than the historical average owing to structural and second-round effects (see table T 1).

Risk of persistent inflation

The risks involved in the present price forecasts are considerable. The main reason for this is the uncertainty around energy supplies during the winter half-year, although KOF does not expect to see severe shortages in its baseline scenario. In addition, the COVID-19 pandemic continues to pose an upside risk, as associated disruption in international supply chains would drive up the prices of foreign goods. On the other hand, political developments abroad could cause key inflation drivers to disappear more quickly than forecast. Long-term inflation expectations currently remain stuck at just above 1 per cent. This is the basic prerequisite for preventing a wage-price spiral.

Contact

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland