What Swiss economists think about inflation, monetary policy and the franc

- KOF

- KOF Bulletin

- Economists Surveys

At present, the Swiss National Bank (SNB) is having to contend with above-average inflation, the economic recovery from the COVID-19 pandemic, and the considerable uncertainty arising from the war in Ukraine. In March, therefore, KOF and the Neue Zürcher Zeitung (NZZ) newspaper surveyed economists on their assessments of inflation and monetary policy in Switzerland.

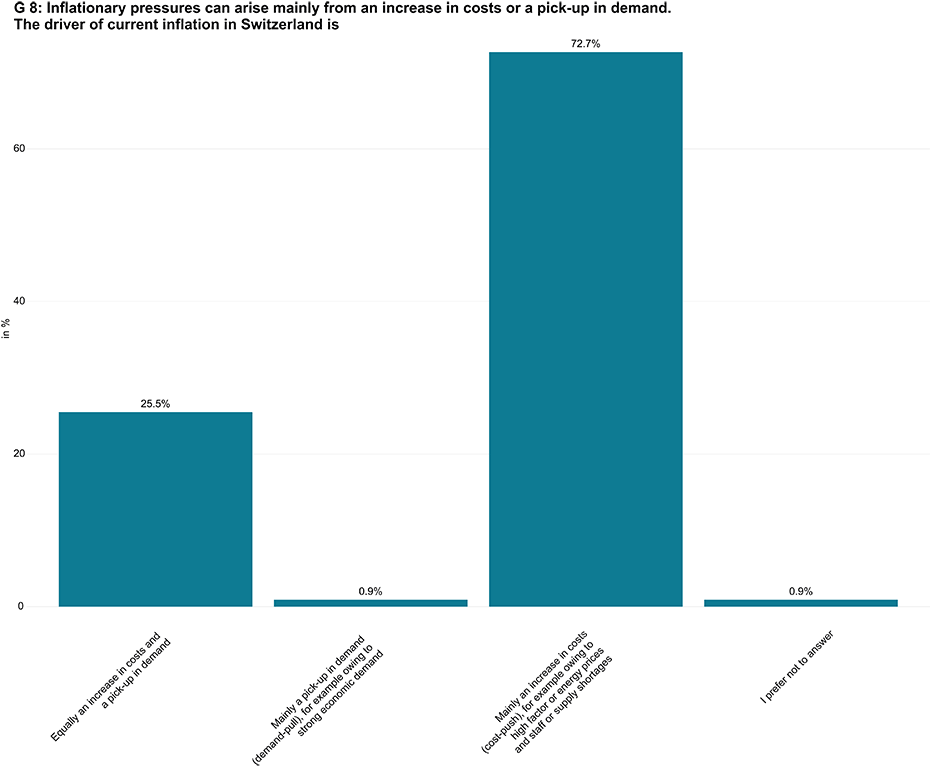

Year-on-year consumer prices in Switzerland rose in February and March 2022 at the fastest rate since the financial crisis of 2009. Rising at an annual rate of 2.2 per cent in February and 2.4 per cent in March, inflation is above the range of 0 per cent to 2 per cent that the SNB defines as price stability. The reason for the currently high inflation rates may be a cost-push – for example due to high factor or energy prices and staff or supply shortages. On the other hand, high inflation can be caused by an increase in demand (demand-pull) – for example due to catch-up effects resulting from the COVID-19 pandemic, the fiscal support provided during the pandemic or the expansionary monetary policy stance. Chart G 8 shows the responses given to the question about the main driver of current inflation in Switzerland. Only 1 per cent of survey respondents reckon that its main cause is the revival of demand. Almost three-quarters attribute the current price trends to higher costs. More than a quarter, on the other hand, are of the view that these price pressures are equally supply- and demand-driven.

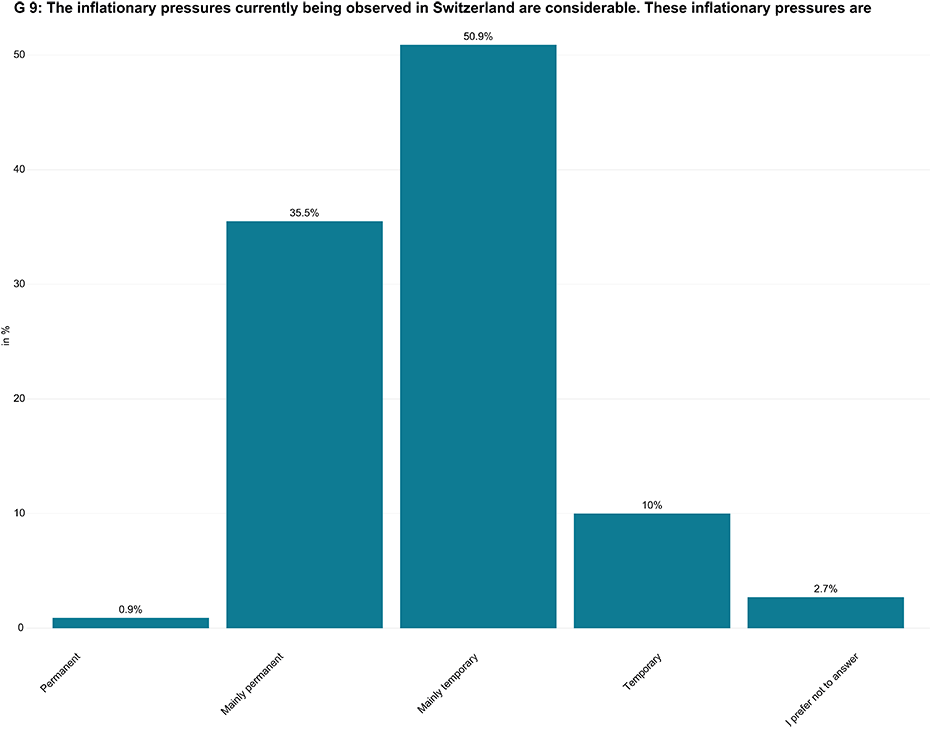

Given the currently rising inflation rates, the question is whether inflation will soon return to normal or whether it will remain high over the longer term. Sustained high inflation can arise, for example, if higher wages are demanded as a result of inflation, higher wage costs in turn push up prices and thus a wage-price spiral is set in motion. The results of the survey of economists reveal that the inflationary pressures currently being observed in Switzerland are seen as (mainly) temporary (see chart G 9). 61 per cent of survey respondents believe that the current price trends are (mainly) temporary, while 36 per cent see them as (mainly) permanent.

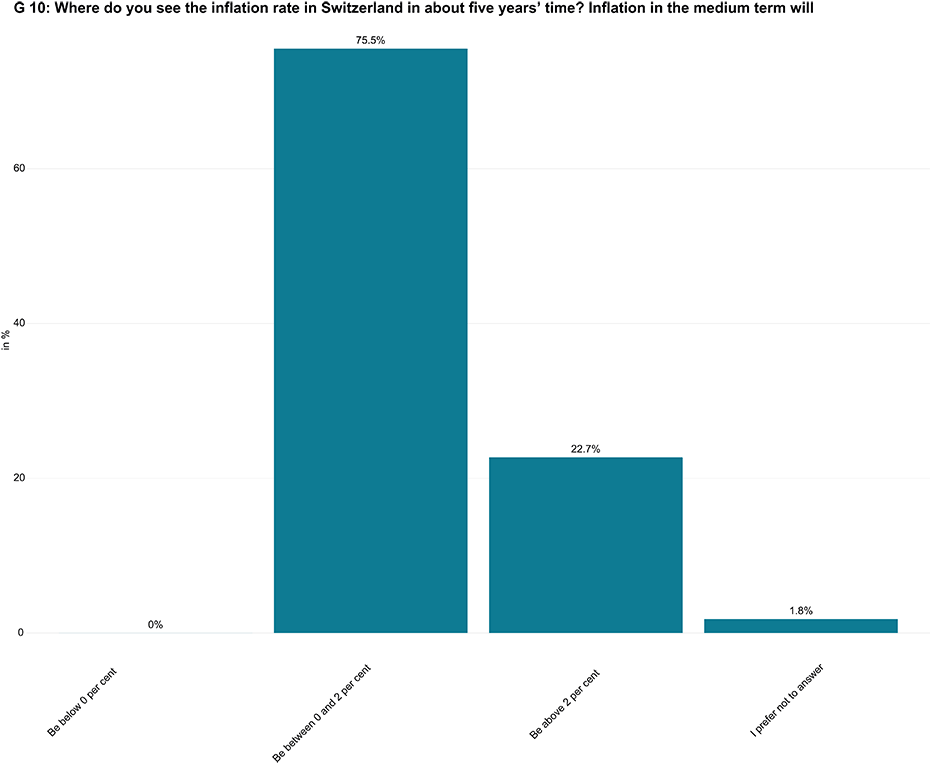

The survey of economists also asked about expectations regarding the rate of inflation in five years’ time (see chart G 10). 76 per cent of survey respondents expect inflation to be within the SNB’s target range of 0 per cent to 2 per cent in five years’ time. A clear majority thus expects inflation to remain within this target range over the long term. A year-on-year price increase of more than 2 per cent is expected by 23 per cent of respondents. Respondents do not see any deflationary price trends as a plausible option.

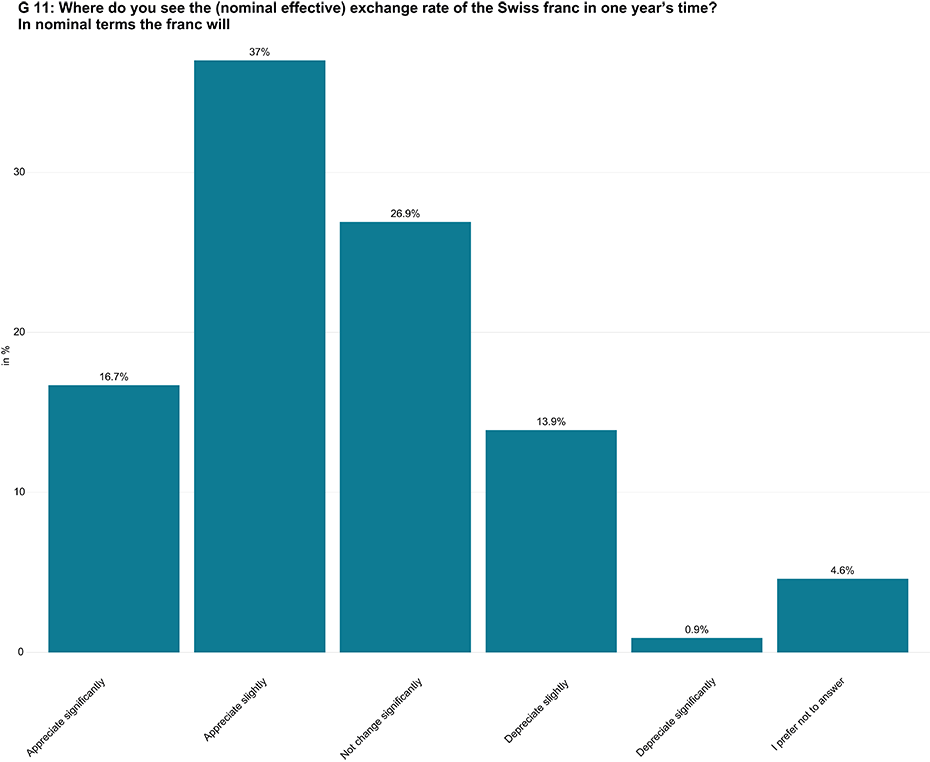

Half expect to see nominal appreciation of the Swiss franc

The nominal effective exchange-rate index of the Swiss franc has been on an upward trajectory for several years, meaning that the franc has appreciated in nominal terms against the currencies of its major trading partners. The Swiss franc appreciated further in March as a result of the macroeconomic uncertainty caused by the war in Ukraine and the currency’s role as a safe haven as well as Switzerland’s occasionally large inflation differential compared with other countries. More than half of survey respondents expect the Swiss franc to appreciate (slightly) over the coming twelve months (see chart G 11). In contrast, 27 per cent of economists expect to see no significant change in the nominal effective exchange-rate index, while 15 per cent expect the Swiss franc to depreciate (slightly).

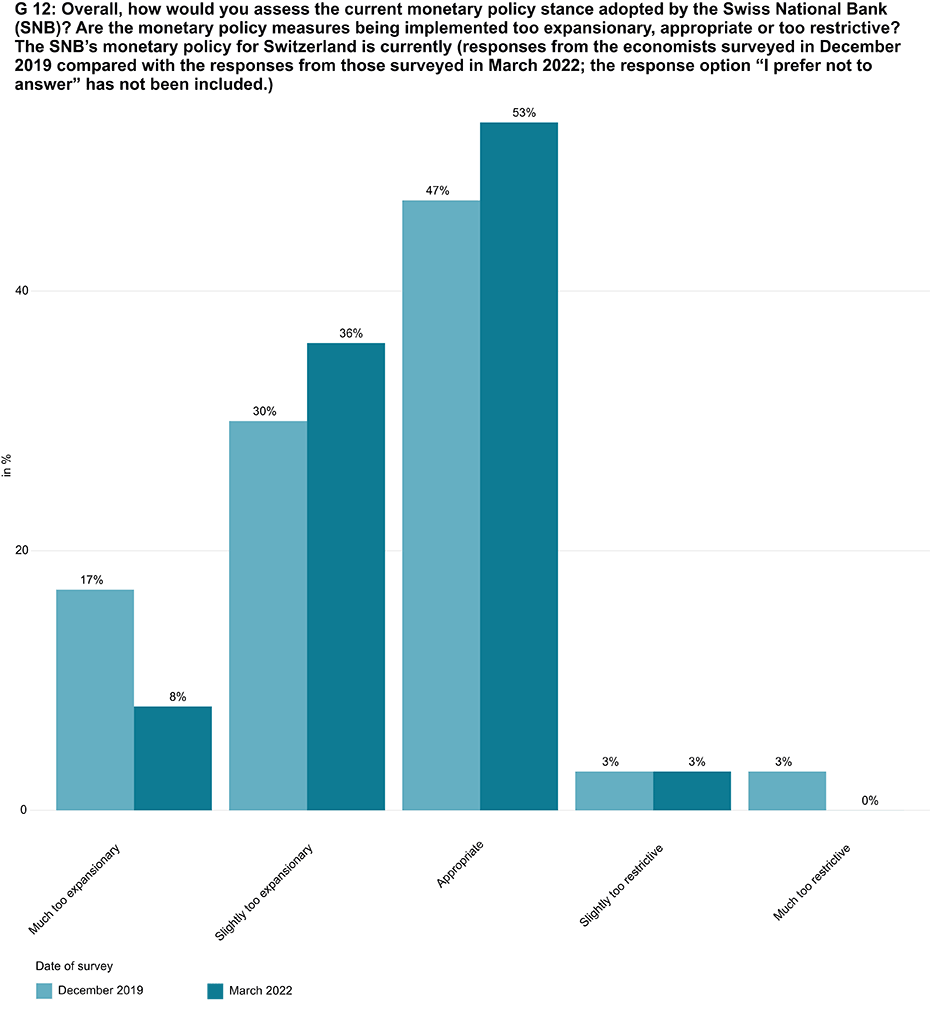

Most respondents view the SNB’s monetary policy as appropriate

Since the year-on-year inflation rates in February and March of this year were above the SNB’s target range, this raises the question of whether the current monetary policy is still justified or whether a more restrictive stance might be necessary to keep inflation in check. Any gradual normalisation of monetary policy would also create the scope for taking measures to ease the situation in future crises. However, tightening monetary policy in the current climate risks stalling the economic recovery from the COVID-19 pandemic. In addition, the economic outlook is more uncertain than usual owing to the war in Ukraine, and prices are not rising sharply across the board but only in the case of certain goods. The economists surveyed have differing views on the current direction of monetary policy. More than half of the economists who expressed an opinion view the monetary policy measures implemented in Switzerland as appropriate, while 44 per cent judge monetary policy to be (mainly) too expansionary (see chart G 12). The remaining 3 per cent think that the SNB is acting (mainly) too restrictively.

The same question on how to assess the SNB’s monetary policy was asked in a KOF-NZZ survey conducted back at the end of 2019. Chart G5 shows how the relevant percentage responses differ between the two surveys. On the whole, economists’ attitudes have not changed significantly. Two similarly large camps considered monetary policy to be either appropriate or (mainly) too expansionary, while only a few considered it to be (mainly) too restrictive. Compared with the 2019 survey, however, the latest results are slightly more concentrated around the middle response options. Whereas 17 per cent felt that the SNB’s monetary policy stance was clearly too expansionary in 2019, only 8 per cent did so in this year’s survey.

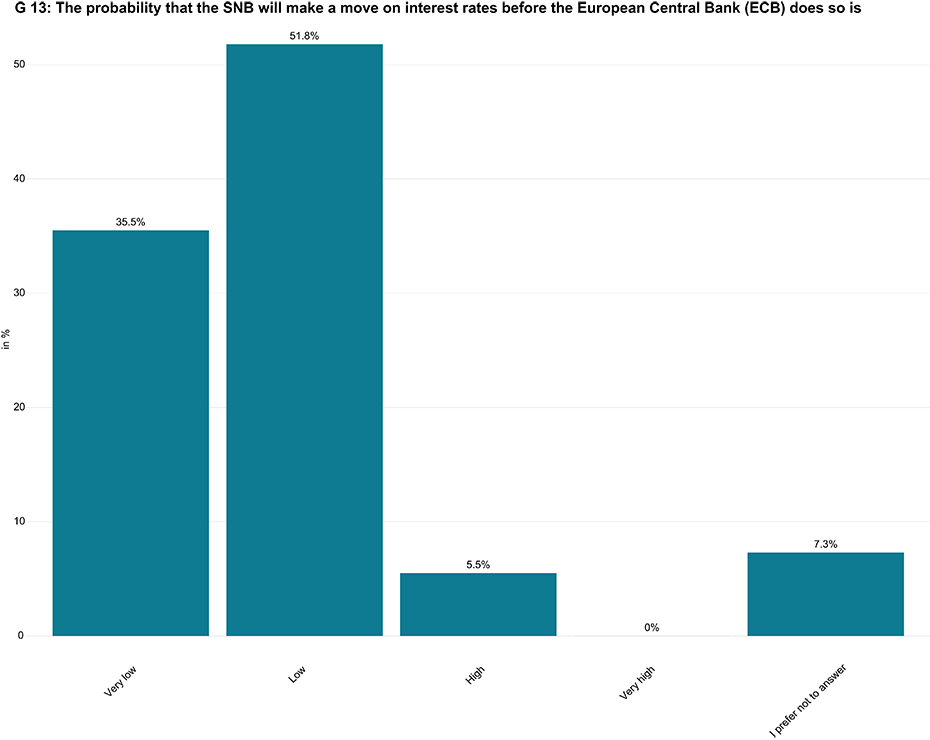

Discussion of any monetary policy normalisation also focuses on the question of how likely it is that the SNB will raise key interest rates before the European Central Bank (ECB) does so. Higher interest rates in Switzerland would make Swiss investments more attractive than European ones, which would put upward pressure on the Swiss franc against the euro. 87 per cent of the researchers surveyed believe it is (very) unlikely that the SNB will make any move on interest rates before the ECB does so (see chart G 13). Only 6 per cent of these experts see a scenario in which the SNB raises interest rates before the ECB as likely.

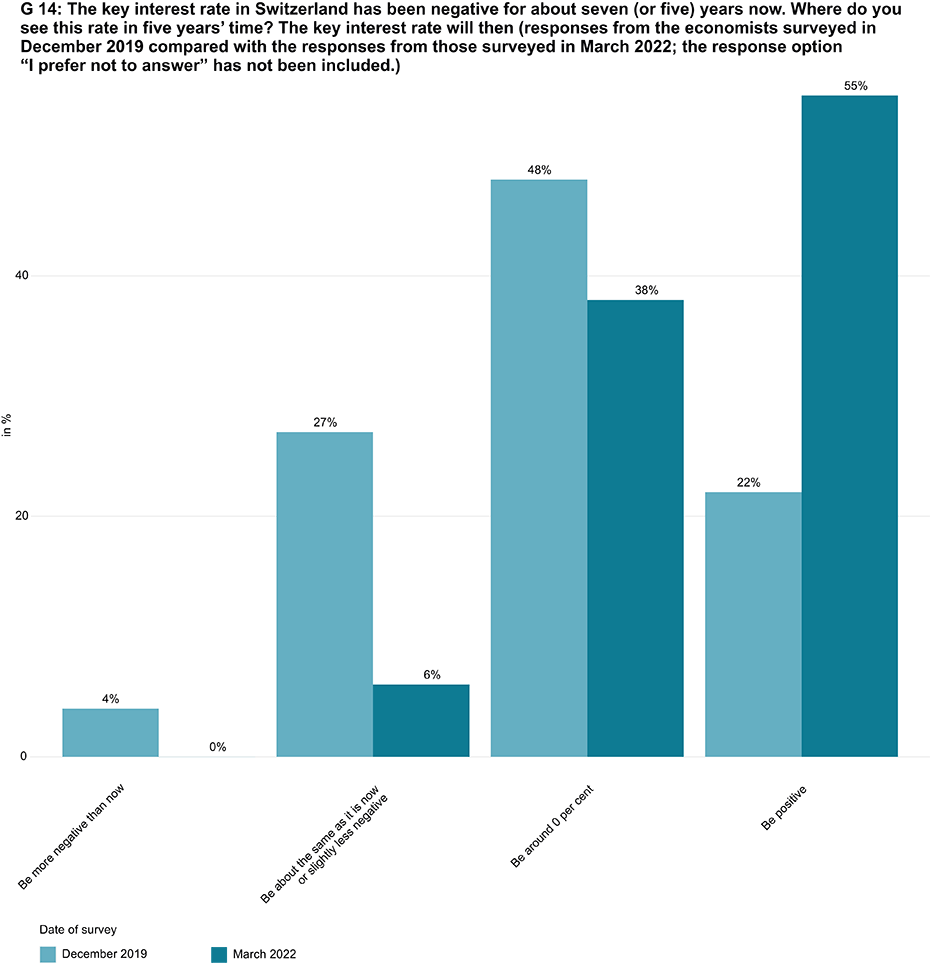

Negative interest rates expected to be raised within the next few years

The key interest rate in Switzerland has been in negative territory since January 2015. More than half of the economists surveyed expect this rate to be positive within the next five years (see chart G 14). Another 38 per cent expect this rate to be around 0 per cent. Only 6 per cent think that it will be about the same as it is now or slightly less negative. None of the economists surveyed expects to see further interest-rate cuts.

This attitude was non-existent at the end of 2019. In the survey conducted at that time, a minority expected to see a reversal of interest-rate policy in the near future, with 22 per cent of survey respondents expecting to see a positive interest rate within five years, 48 per cent expecting a rate of around 0 per cent, 27 per cent expecting the rate to remain virtually unchanged and 4 per cent expecting to see a more negative rate. This variation can probably be explained by the fact that inflation rates are currently significantly higher than they were three years ago and that an interest-rate move by the ECB is now more likely in the near future.

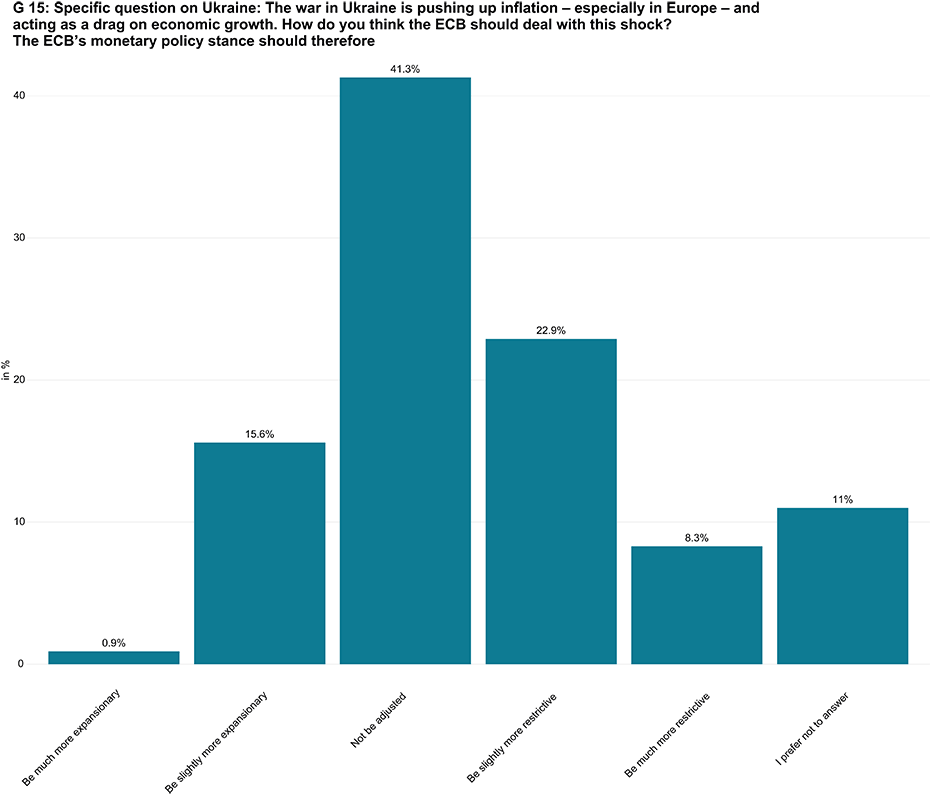

No consensus on how to adjust the ECB’s stance in response to the war in Ukraine

The ECB is also in a difficult situation at the moment. While the sharp rise in consumer prices would tend to demand a more restrictive monetary policy, the economic risks have grown significantly owing to the war in Ukraine. Russia’s invasion caused the KOF-NZZ survey to be supplemented to include a question relating to the changes arising from the war. The ECB’s monetary-policy decision taken in March 2022 was that interest rates would remain on hold for the time being. The economists surveyed were asked whether the ECB should adjust its monetary-policy stance in response to the war in Ukraine, and they disagree on this point. While 31 per cent of survey respondents would favour a (slightly) more restrictive monetary policy because of the war, 17 per cent see a (slightly) more expansionary stance as more conducive (see chart G 15). The remaining 41 per cent would not recommend making any adjustments to monetary policy compared with the hypothetical scenario without any war.

Contacts

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland

KOF FB Konjunkturumfragen

Leonhardstrasse 21

8092

Zürich

Switzerland

Director of KOF Swiss Economic Institute

Professur f. Wirtschaftsforschung

Leonhardstrasse 21

8092

Zürich

Switzerland

The KOF-NZZ survey of economists covers topics relevant to economic policy in Switzerland and provides a means of making the views of academic research economists visible to the public. KOF’s media partner in the preparation and interpretation of this survey of economists is Switzerland’s Neue Zürcher Zeitung (NZZ) newspaper. In March, KOF and the NZZ conducted a survey on inflation and monetary policy in Switzerland. 785 economists were contacted and responses were received from 110 economists at 17 institutions.