Corporate bankruptcies exceeding pre-crisis levels for the first time

- KOF

- Swiss Economy

- KOF Bulletin

The number of company bankruptcies in Switzerland continued to rise in March and, after a two-year low, has exceeded the pre-crisis levels of 2019 for the first time. Although this increase is broadly based across sectors and regions, a wave of bankruptcies remains unlikely. The boom in new business start-ups has flatlined recently.

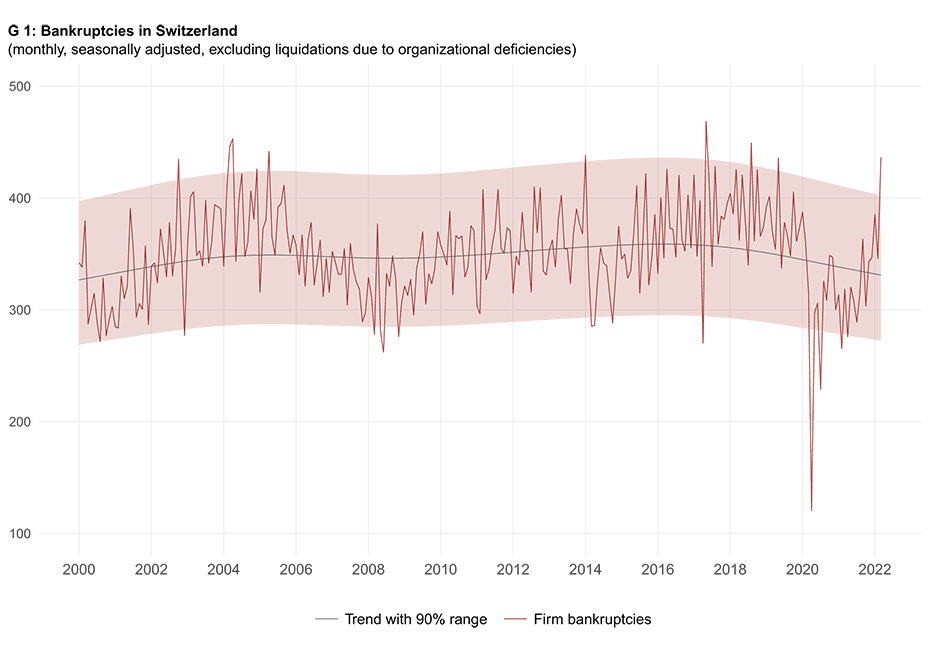

KOF examines the numbers of company bankruptcies over time by scrutinising the commercial register figures collected and processed by Dun & Bradstreet Schweiz AG. The data show that the number of monthly company bankruptcies plummeted at the beginning of the COVID-19 pandemic. Such bankruptcies (excluding liquidations by the bankruptcy authorities) in 2020 were, on average, around 19 per cent lower than they had been in 2019, and even in 2021 they were still 17 per cent lower (see chart G 1). The number of bankruptcies has recently recovered significantly and by March 2022 even exceeded its pre-crisis level. This trend raises the question of whether a wave of bankruptcies has accumulated over the past two years.

Government support measures keeping firms afloat

To answer this question, it is useful to look more closely at the causes of the low bankruptcy figures recorded during the coronavirus pandemic.

(1) Legal measures: The immediate reasons for the massive slump in bankruptcies in spring 2020 were the legal standstill ordered by the Swiss Federal Council (19 March to 4 April 2020), the subsequent debt-collection holidays (until 19 April) and the suspended obligation to report over-indebtedness (until the end of October 2020).

(2) Loans: To ensure liquidity, around 138,000 firms received bridging loans totalling CHF 16.9 billion until July 2020 under the Swiss government’s COVID-19 lending programme.

(3) Direct aid: To cover staff costs, around CHF 20 billion was paid out to struggling companies in the form of short-time working compensation and financial support for self-employed individuals. 35,000 particularly hard-hit firms have received direct payments amounting to almost CHF 5 billion to cover their fixed costs under the cantonal hardship assistance fund available since 2021.

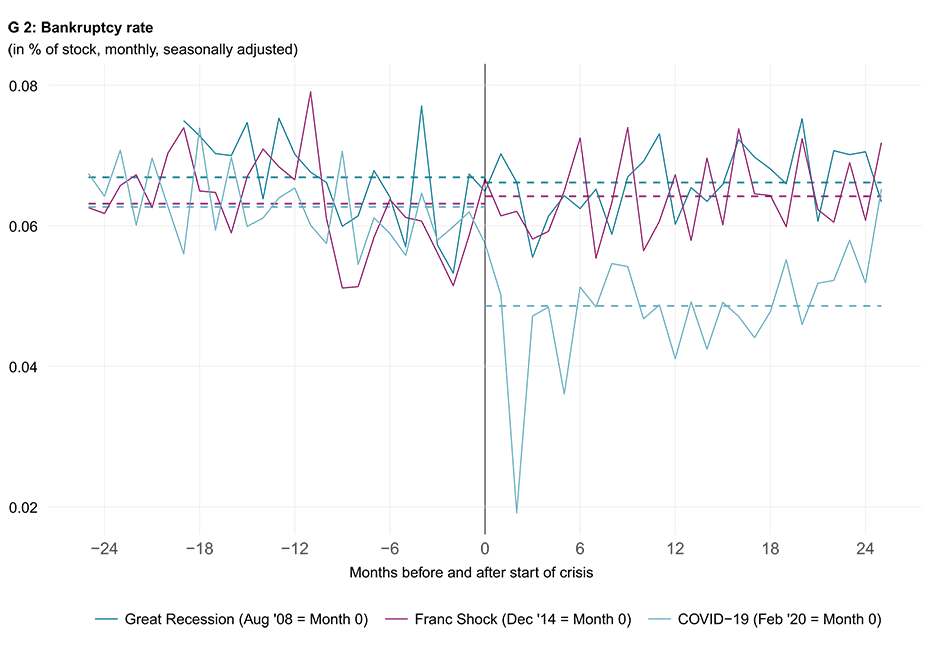

The exceptional financial support measures taken have also ensured that the numbers of bankruptcies occurring over time during the COVID-19 pandemic have differed from those seen during previous crises. The Great Recession of 2008 and the Swiss franc shock of 2015 were not followed by any immediate movements in the bankruptcy rate (see chart G 2). As many such measures have now expired, the bankruptcy rate has risen sharply again.

Financial support measures expiring

Many financial support measures, such as simplified short-time working compensation and the hardship assistance fund, are likely to expire soon. This should prevent unproductive firms from being kept alive by government funding – the so-called ‘zombie company problem’. However, this raises the question of whether we will now see more pent-up and deferred bankruptcies. To answer this question, it helps to differentiate between the causes of the low bankruptcy rates:

(1) Legal measures: These measures have long since expired, so catch-up effects are hardly to be expected.

(2) Loans: Almost 30 per cent of the total loan volume has already been repaid – well before the repayment deadline of eight years. Although the greater indebtedness of companies could lead to defaults in some cases, the rapid normalisation of the economy should have alleviated this problem.

(3) Direct aid: Direct payments have enabled large sections of the economy to ride out any pandemic-related cyclical disruption. If we now assume that the economy returns to normal structurally, company bankruptcies should return to their ‘normal’ pre-crisis level. New debt, which is mainly found on the Swiss government’s balance sheet, should be reduced over a lengthy period of time through structural budget surpluses and additional SNB distributions. Consequently, no additional financial burden is expected to be imposed on businesses.

The two-year phase of low numbers of bankruptcies is thus likely to be associated with only minor catch-up effects. Nevertheless, above-average levels of company bankruptcies can probably be expected over the coming period. The pandemic has permanently changed many consumer preferences and required supply chains in some sectors to be adjusted. This is likely to have triggered or accelerated structural changes in many sectors of the economy – especially in hospitality, transport, retailing and other contact-intensive service industries.

Sharp increase in individual sectors

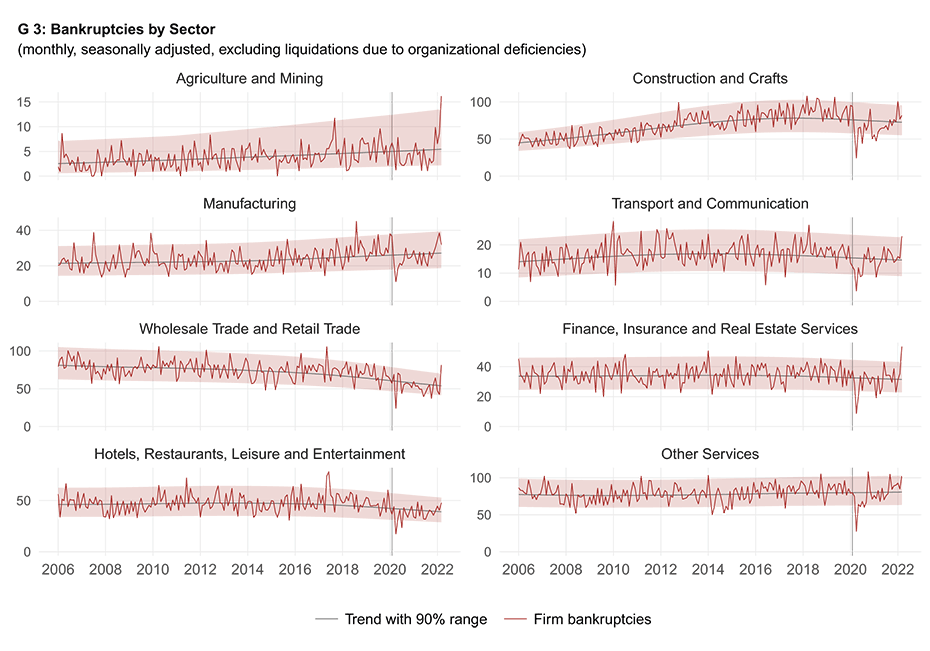

Company bankruptcies in some sectors – such as wholesaling and retailing (see chart G 3) – have recently risen beyond the normal volatility range. Although a trend increase in insolvencies is to be expected, these figures should be interpreted with caution on a sectoral view. A temporary surge in bankruptcies occurs sporadically owing to volatile base data and need not indicate a rising wave of bankruptcies in individual sectors.

Wave of start-ups flatlining

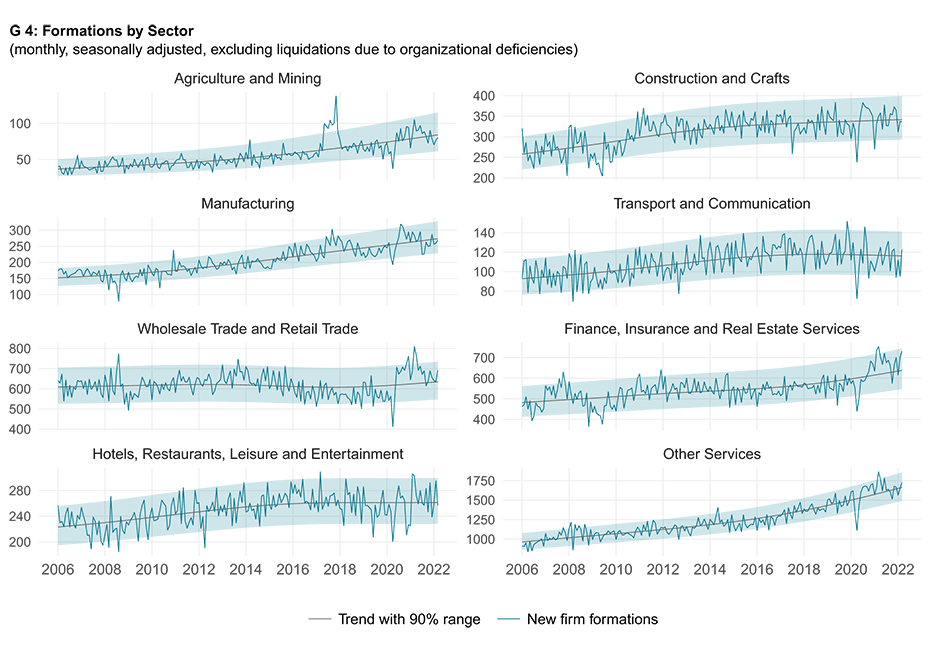

Pandemic-related structural change has already been evident in the form of heightened start-up activity in some sectors since the summer of 2020. Accelerated digitalisation has triggered a genuine start-up boom (see chart G 4) especially in the wholesale, retail, finance, insurance and real-estate sectors. However, the number of start-ups has recently flatlined – probably partly because of the ongoing normalisation of the pandemic and the economy. A comparison with the financial crisis of 2008 again shows the unusual economic nature of the COVID-19 pandemic. At that time, start-up activity in the sectors affected – such as financial services and construction – declined significantly.

Limited disruption despite geopolitical upheaval

The numbers of corporate bankruptcies in many industries going forward are likely to depend on how much consumer preferences have changed and consolidated. Whether business tourism picks up or online meetings remain a part of the post-COVID world, for example, is likely to be crucial for the hospitality industry in urban areas. The war in Ukraine seems to have only slightly impaired companies’ business so far (with the exception of financial and insurance service providers). Any escalation of this situation would, of course, affect the economic recovery.

Contacts

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland