Eurozone Economy has Slowed Down

- KOF Bulletin

- World Economy

The pace of the Eurozone economy has slackened. Given a rather moderate 0.3 per cent increase in production over the previous quarter, gross domestic product (GDP) expanded more slowly in the second quarter 2016 than in the preceding quarter. In France and Italy, aggregate production even stagnated.

Following a 0.6 per cent increase in the first quarter 2016, production growth slowed down to a mere 0.3 per cent in the second quarter. However, with non-recurring effects distorting dynamics upwards in the first quarter, this downturn did not come as a surprise. The mild winter, for instance, boosted construction activities in Germany, while ticket sales for the European Football Cup drove private consumption in France. These non-recurring effects resulted in a counter-movement in the second quarter. Private consumer spending in France, for instance, merely stagnated. While the smaller import volume made a positive contribution to the growth of external trade, the low inventory build-up had a dampening effect on production. Following significant gains in the past few quarters, investment in construction and in plant and machinery once again declined.

In Italy, the persistent banking crisis and insecurity regarding the outcome of November’s referendum on extensive constitutional reforms are likely to have had a negative impact on consumption and investment demand. In Germany, growth dynamics slowed down from 0.7 per cent in the first quarter to 0.4 per cent in the second quarter. However, this second-quarter percentage is still higher than the overall Eurozone figure. The expansion was predominantly due to external trade and consumption, while construction regressed due to weather-related pre-emptive effects in the first quarter.

Further growth impetus was provided by the Netherlands and Spain. Greece also reported an increase in production. Both Spain and Greece are buoyed up by booming tourism industries, benefiting to some degree from political insecurity in other holiday destinations, such as Egypt or Turkey.

To everyone’s surprise, Ireland reported a 26 per cent increase in GDP after a revision of its 2015 national accounts. This result is most likely due to so-called ‘tax inversions’, i.e. the relocation of registered head offices by large multinationals. In consequence, productive capital rose by 40 per cent, especially thanks to intellectual property rights, and net exports doubled due to licensing income and merchanting. Although Ireland’s share in the Eurozone’s total economic output is of minor importance, the effect of this revision on total Eurozone GDP and its annual growth rate will be quite noticeable at around 0.4 percentage points.

Price and labour market recovery varies

Consumer price trends also present a heterogeneous picture. While the year-on-year change in the Belgian consumer price index amounted to two per cent (due to a rise in VAT on electricity from six per cent to 21 per cent in September 2015, the rise is distorted upwards), inflation in Germany and France stood at 0.4 per cent. Italy and Spain continued to display deflationary tendencies at -0.2 per cent and -0.9 per cent respectively. Overall inflation in the Eurozone in July 2016 was 0.2 per cent, while core inflation, excluding energy and unprocessed foodstuffs, amounted to 0.8 per cent. Once the base effects of earlier drops in commodity prices expire in the coming months, inflation is set to rise again on a more substantial basis.

The last few quarters’ upswing in the Eurozone has resulted in a decline in unemployment, albeit at very different levels (see G 1, in comparison with other EU countries and Switzerland). The total unemployment rate in the Eurozone stood at 10.1 per cent in June, following 11 per cent in the preceding year. In Spain, unemployment dropped below the 20 per cent mark for the first time in six years while, at 4.2 per cent, the German rate was back to pre-reunification levels. The Italian labour market reforms adopted at the beginning of 2015 seem to be bearing fruit: Compared to the previous year, unemployment declined by 0.6 percentage points to 11.6 per cent (most recent figure), while youth unemployment even decreased by 4.5 percentage points to 36.5%. In France, where unemployment recently dropped below 10 per cent, hasty labour market reforms were pushed through in July despite vehement protests by trade unions and employees. The easing of dismissal protection laws and flexible working hour regulations are to provide the labour market with greater dynamics.

Insecurity regarding the state of the Italian banking sector

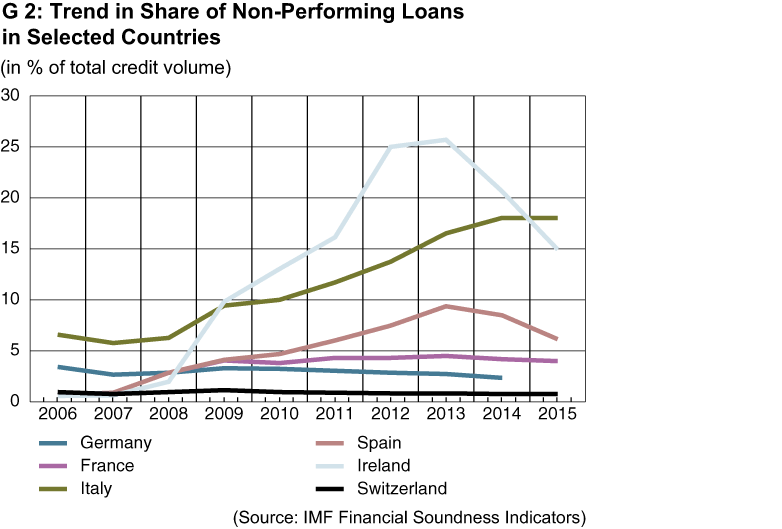

Italy’s banks weathered the 2009 financial crisis relatively well. They had neither invested excessively in speculative foreign ventures, nor were they subject to unwanted developments in the real estate sector due to insufficient lending diversification. Nevertheless, due to the weakness of the subsequent economic trend in Italy and the delay of structural reforms, around 18 per cent of loans are now rated ‘non-performing’. According to the definition of the International Monetary Fund (IMF), loans are placed in this category when principal or interest payments have been outstanding for more than 90 days. Italian banks thus have the largest share of non-performing loans in the entire Eurozone after Greece and Cyprus, whose banks have been drip-fed by international money sources for some time now (see G 2 for comparison with other Eurozone countries and Switzerland).

Public recapitalisation of non-performing banks is, however, in contravention of new EU guidelines which favour burden-sharing by shareholders and subordinated creditors. Nevertheless, the securitisation of non-performing loans, which has been initiated by the Italian government, and the injection of private funds to bolster the equity of failing institutions should defuse the situation for the foreseeable future.

Contact

KOF Konjunkturforschungsstelle

Leonhardstrasse 21

8092

Zürich

Switzerland